In this article, Chloé ANIFRANI (ESSEC Business School, Global Bachelor in Business Administration (GBBA), 2019-2024) shares her professional experience as Asset Management Development Assistant for Amplegest.

About the company

Amplegest was established in 2007 and operates across three main business segments: Private Wealth Management, Family Office, and Asset Management.

Private Wealth Management

Wealth Engineering: A team of wealth engineers provides personalized advice to clients, addressing evolving issues related to wealth, taxation, and family matters over time.

Discretionary Portfolio Management: The firm offers the market expertise of its fund managers, developed through extensive experience in banks or asset management firms. Amplegest actively seeks new investment opportunities across all asset classes and geographical regions, employing a short and collaborative decision-making process for responsiveness.

Profiled Portfolio Management: The firm offers specific profiled portfolios to retail investors, who manage their own clients’ portfolios.

Family Office

Amplegest serves high-net-worth individuals in France and internationally through a dedicated department, Canopée FO, offering fully customized services.

Asset Management

Amplegest’s Asset Management division offers three expertise:

- Equity: with 5 funds, the firm covers many thematics (such as technological innovation, pricing power), capitalizations (large, mid and small caps) and regions (global, US and Eurozone),

- Diversified portfolios: with its Latitude range, the firm offers diversified funds with precise return objectives and risk allocation, with an offer for each profile of investor,

- Fixed Income: the firm distributes Octo AM’s funds, a company specialized in bonds funds, with a Value management style.

Key Facts and Figures

- Assets under Management (AuM): 3bn€

- A large product range of more than 13 funds

- Diverse clientele: institutional, retail, funds selectors…

- All activities of Amplegest are approved by the AMF (Autorité des Marchés Financiers).

Logo of the company.

![]()

Source: Amplegest.

My internship

My internship was in the sales department of Amplegest Asset Management. With a team of five sellers, I learned about the different distribution channels of funds in a B2B model (the team I was in did not work with final clients). The focus of the team is on institutional and retail clients. In 2023, we mainly worked on distributing Octo AM’s bonds funds, which have met a great success following the interest rates’ raises. The firm’s fixed income’s AuM went from €350m in 2022 to €800m in 2023.

My missions

Over the course of six months, I supported the team with customer relationship management and enhancing our understanding of the firm’s competitive landscape.

One of my primary responsibilities involved diligently preparing for client appointments. This entailed creating comprehensive briefs on Amplegest funds and conducting in-depth analyses of their competitive environments. Whether addressing global competition or specific funds selected by clients, my aim was to highlight the differentiating aspects of our offerings.

In addition to client-focused tasks, I took charge of producing documents containing technical information about the funds, ensuring compliance with our customers’ regulatory requirements such as “étude de transparisation”, KYC, and Due Diligence. Monthly, I managed the dispatching of these documents, tailoring the frequency to the individual needs of each client.

Collaborating closely with both the Asset Management and Marketing teams, I actively contributed to the planning and execution of numerous B2B events. This encompassed the coordination of trade fairs such as Patrimonia, organizing large-scale professional lunches and presentations, facilitating webinars, and orchestrating engaging professional afterwork events.

Furthermore, I dedicated efforts to augment the firm’s understanding of its funds’ positions in the market. Collaborating with dedicated tools designed to gather real-time information on competitors’ performance and track records, I systematically compared these metrics against our own. This included the creation of specific peer groups tailored to each fund, providing valuable insights into their relative standing within the market.

Required skills and knowledge

In Asset Management firms, the role of Sales Assistants requires a multifaceted skill set that encompasses technical expertise and strong interpersonal skills. B2B clients expect sales professionals to possess an in-depth understanding of the market and its dynamics, coupled with the ability to articulate a fund’s management process, recent market movements, and current values with the same proficiency as a portfolio manager.

Upon assuming the role, I prioritized enhancing my knowledge of current events, particularly those related to the stock market and global financial trends. Each day commenced with a thorough review of newsletters, and I highly recommend daily publications by Bloomberg for comprehensive insights. This proactive approach allowed me to respond swiftly when clients sought information about the prevailing market conditions and how they correlated with Amplegest’s product offerings.

A good knowledge of the regulatory environment of Asset Management firms is also essential. The rules that govern this profession are numerous and constantly updated. This means that a great interest for current events (suits and convictions in other firms, general recommendations…) will be beneficial, as well as a good understanding of the guidelines provided by the Compliance department.

A proficiency in Excel is paramount, serving as a vital tool for data analysis, reporting, and decision-making within the asset management landscape. Additionally, financial analysis skills are crucial for interpreting complex financial data and providing comprehensive insights to clients.

In terms of soft skills, effective communication is fundamental—both verbal and written—enabling the clear and concise articulation of complex financial concepts. Strong client relationship management skills are essential for building and maintaining long-term partnerships, understanding client needs, and providing excellent customer service.

Adaptability is key in navigating evolving market conditions, client preferences, and organizational changes. Problem-solving skills come into play in identifying challenges and proposing effective solutions to address client inquiries and concerns.

Negotiation skills are valuable in securing mutually beneficial agreements with clients, while team collaboration is essential for working effectively with colleagues across different departments, fostering a cooperative and supportive work environment. Effective organization and multitasking are necessary for managing multiple tasks and projects simultaneously, while analytical thinking is crucial for making data-driven decisions and providing valuable insights to clients.

Furthermore, networking skills contribute to building a professional network within the industry, attending relevant events, and staying informed about industry trends. Finally, strong time management ensures efficient task prioritization, meeting deadlines, and delivering results in a fast-paced environment. Together, these skills collectively contribute to the effectiveness of an Asset Management Sales Assistant in navigating the complexities of the financial industry and delivering value to clients and the organization.

What I learned

In terms of knowledge, I learned a lot about the organization of an Asset Management firm, and its funds. In this internship, I gained practical knowledge of the regulatory landscape governing the financial sector. I also learned about fund organization and shares, exploring the nuances of fund structures, issuance of shares, and compliance with legal frameworks. Moreover, I developed a perspective on the distinctions between the back, middle, and front office specific functions within an asset management firm. This exposure allowed me to appreciate the integral roles each department plays in the overall operational efficiency and success of the organization.

In this role, I was also able to use skills developed in previous internships. Time management was one of them, which, as explained earlier, revealed itself to be a crucial component to a good experience in this field. Indeed, some requests from clients and coworkers needed to be tended to in a matter of minutes or may make the firm lose millions (a bit extreme, but sometimes realistic). Therefore, my other missions needed to be done as soon as possible, to allow time for the more pressing ones. I learned to organize my work to optimize my efficiency on this matter.

In terms of technical skills, I learned funds analysis, with the ability to evaluate their performance, risk profiles and underlying strategies thanks it their allocation and communications. This involved a systematic examination of the firm’s competitive market and its key players and trends.

Thanks to this in-depth benchmark, a sales team is able to prepare clients’ briefs, but also to offer new strategies and product offerings to their managers, identifying market opportunities and specific needs for the clients.

This experience has not only enhanced my analytical capabilities but also deepened my understanding of the intricate dynamics within the financial markets.

As a Sales Assistant, I also developed my VBA skills, and learned the power of this tool, especially used in finance firms. Excel VBA helped me to automate and streamline numerous tasks related to data analysis, reporting, and client communication, thereby significantly enhancing my efficiency and productivity. By developing proficiency in Excel VBA, I could create customized macros and scripts tailored to the specific needs of our team, automating repetitive processes and allowing me to focus more on strategic aspects of sales and client relationship management.

Overall, this experience not only broadened my knowledge and skills base but also equipped me with practical insights crucial for navigating the complex and highly regulated landscape of asset management.

Financial concepts related my internship

Fixed income

As explained earlier, 2023 was the year of fixed income. Because of this, understanding the inner workings of a bond funds was essential, as those funds are more complex than equity funds.

In order to give the clients the information they required and work adequately with the provided documents, this knowledge was a real necessity.

Diversified Asset Allocation

In preparing briefings for clients and partners, I often had to summarize the recent movements made on the firm’s diversified funds. Those funds invest in ETFs, bonds, monetary funds structured products in order achieve their expected annual return and respect their risk budget. Therefore, this type of product is, once again, more complex than equity funds, and require a deep understanding of active asset allocation and market movements.

Return on Investment

In order to have more insight on Amplegest’s clients’ satisfaction, I had to compute their total RoI, taking into account every movement they made over the course of their investment in the firm (subscription/redemption), in different funds at different times and with different net asset value of the shares they bought. This required a good understanding of Return on Investment.

Why should I be interested in this post?

As ESSEC students, we often think of working in Asset Management firms as working as a portfolio manager. However, there are many other functions in this field, and sales is one of them. If you are looking to expend your knowledge on the field and your potential future job inquiries, this post will teach you more about a very exciting position!

Related posts on the SimTrade blog

▶ All posts about Professional experiences

▶ Louis DETALLE A quick interview with an Asset Manager at Vontobel

▶ Akshit GUPTA Asset management firms

Useful resources

Asset management markets in Europe size & share analysis – growth trends & forecast

About the author

The article was written in February 2024 by Chloé ANIFRANI (ESSEC Business School, Global Bachelor in Business Administration (GBBA), 2019-2024).

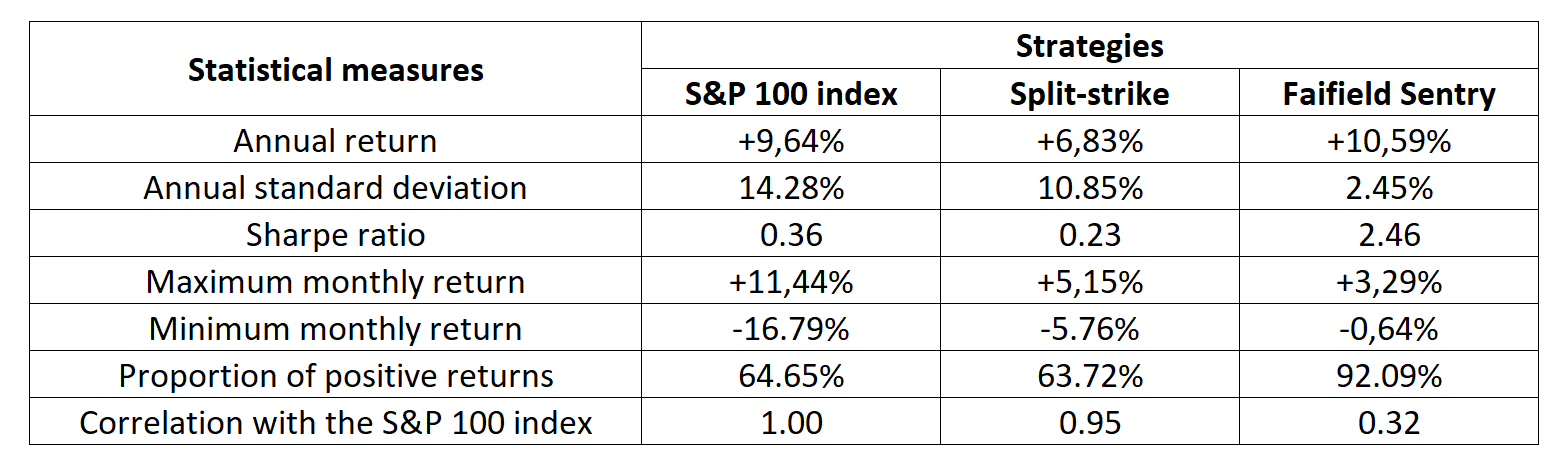

Source: Madoff

Source: Madoff Source: Bernard and Boyle (2009)

Source: Bernard and Boyle (2009)