The WHO’s news on the HPV vaccine caused the stock prices of Zhifei Bio and Wantai Bio to plunge

In this article, Pai LI (ESSEC Business School, Global BBA, 2021-2023) shares her insights on the event “The WHO’s news on the HPV vaccine caused the stock prices to plunge”.

The Brief Introduction of the event

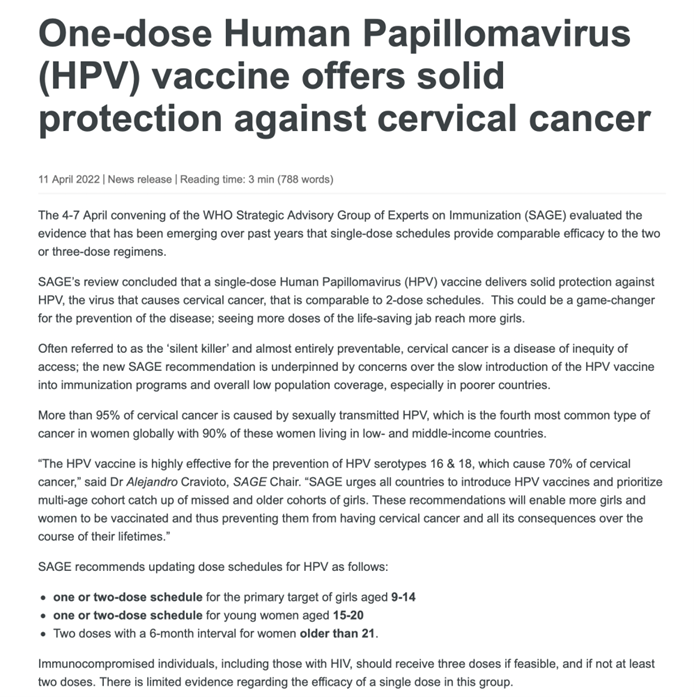

On 2022 April 11, the World Health Organization (WHO) announced on its official website that the WHO convened a meeting of the Strategic Expert Group on Immunization (SAGE) from April 4 to 7 to vaccinate one dose of human papillomavirus (HPV) vaccine. The expert group considered that only 1 dose of HPV vaccine can produce the same immune effect as 2-3 doses, and can effectively prevent cervical cancer caused by HPV infection.

As soon as the news came out, the stock prices of HPV vaccine concept stocks Zhifei Bio and Wantai Bio plunged. As of the close, Zhifei Bio fell 14.19%, and Wantai Bio once fell by the limit, and as of the close, it fell 9.46% and approached the limit.

Stock chart of Zhifei Bio and Wantai Bio

Source: Bloomberg.

Explanation of the Market reaction to the Event

The World Health Organization (WHO) website released information saying that from April 4 to April 7, the WHO Strategic Advisory Group of Experts on Immunization (SAGE) held a meeting, referring to the single dose of the HPV vaccine provides reliable protection, comparable to a 2- or 3-dose regimen.

Regarding the impact of the reduction in the number of HPV vaccination doses, at noon on April 14, After the stock market opened on the afternoon of April 14, the decline in the share price of related companies narrowed. As of the close, Zhifei Biological fell 14.19% to 116 yuan per share, with a market value of 185.6 billion yuan; Watson Bio fell 3.08% to 49.11 yuan / stock market value of 78.65 billion yuan; Wantai Bio fell 9.46% to 257.59 yuan / share , with a market value of 156.37 billion yuan.

The stocks of biology may be affected by the decline of three HPV vaccine companies. On April 14, many stocks in the A-share biological vaccine sector fell. For example, CanSino closed down 3.99%, and Kangtai Bio closed down 1.2%.

WHO press release

Source: WHO.

It is important to note that SAGE stated in the minutes of the meeting that it reviewed new evidence on the efficacy of single doses of HPV, and recommended that women aged 9-14 receive 1 or 2 doses, with a single dose providing comparable and high levels of protection. From a public health perspective, is more effective, less resource intensive and easier to implement. Likewise, 1 or 2 doses are also suitable for women between the ages of 15 and 20.

The current HPV vaccine policy in the world is 2 doses for girls aged 9-14 years, 3 doses for girls aged 15 years and above, and 3 doses for immunocompromised people of any age, including people with HIV.

Notably, SAGE emphasizes that more evidence is needed on whether reduced doses provide protection in immunocompromised groups.

The minutes also mentioned that WHO will conduct stakeholder consultations on these important policy changes before revising the position paper on HPV vaccination.

Predictions for the future

Regarding the recommendations of this WHO meeting on HPV vaccine, I believe that this meeting is only providing a recommendation and not implementing it, and that the current vaccination schedule is still dominated by 2-3 doses. In addition, WHO’s recommendations are mainly based on concerns about the slow introduction of HPV vaccine into immunization programs and low overall population coverage, especially in poorer countries, and the core is to address the huge gap between HPV vaccine supply and demand.

Even if the vaccination procedure is changed from three injections to two injections in the future, the improvement of industry penetration rate and accessibility is believed to effectively fill the market, which is expected to bring strong demand for HPV vaccination in relevant third world countries, and the export of Chinese domestic HPV vaccines is expected to accelerate. At the same time, for Merck’s nine-valent HPV vaccine, it is still in a stage of insufficient production capacity. Whether it is a two-shot or three-shot vaccination program, it is still in a stage of short supply. In conclusion, there is no need to worry too much about the impact on the performance of HPV-related companies.

About the author

The article was written in May 2022 by Pai LI (ESSEC Business School, Global BBA, 2021-2023).