In this article, Nithisha CHALLA (ESSEC Business School, Grande Ecole Program – Master in Management, 2021-2023) presents the FTSE 100 index and details its characteristics.

The FTSE 100 index

The Financial Times and the London Stock Exchange established the FTSE 100 index in 1984. It is now run by FTSE Group, a partnership between the Financial Times and the London Stock Exchange. The index, which is regarded as the standard index for the UK equity market, includes the 100 largest companies by market capitalization that are listed on the London Stock Exchange.

Larger companies have a greater influence on the index’s movements than smaller ones because the index is market capitalization-weighted. HSBC, Royal Dutch Shell, BP, and Unilever are a few of the biggest companies that make up the FTSE 100 as of 2021. The FTSE 100 is a key metric for gauging the state of the UK economy because it serves as a benchmark for funds and investment portfolios with UK roots. Recent occurrences like Brexit, the COVID-19 pandemic, and adjustments to the global economy have all had an effect on the index.

The sectoral composition of the FTSE 100 is one of its distinctive features. The financial and resource sectors account for a significant portion of the index’s total market capitalization, which heavily favors these industries.

How is the FTSE 100 index represented in trading platforms and financial websites? The ticker symbol used in the financial industry for the FTSE 100 index is “UKX”.

Table 1 below gives the Top 10 stocks in the FTSE 100 index in terms of market capitalization as of January 31, 2023.

Table 1. Top 10 stocks in the FTSE 100 index.

Source: computation by the author (data: Yahoo! Finance financial website).

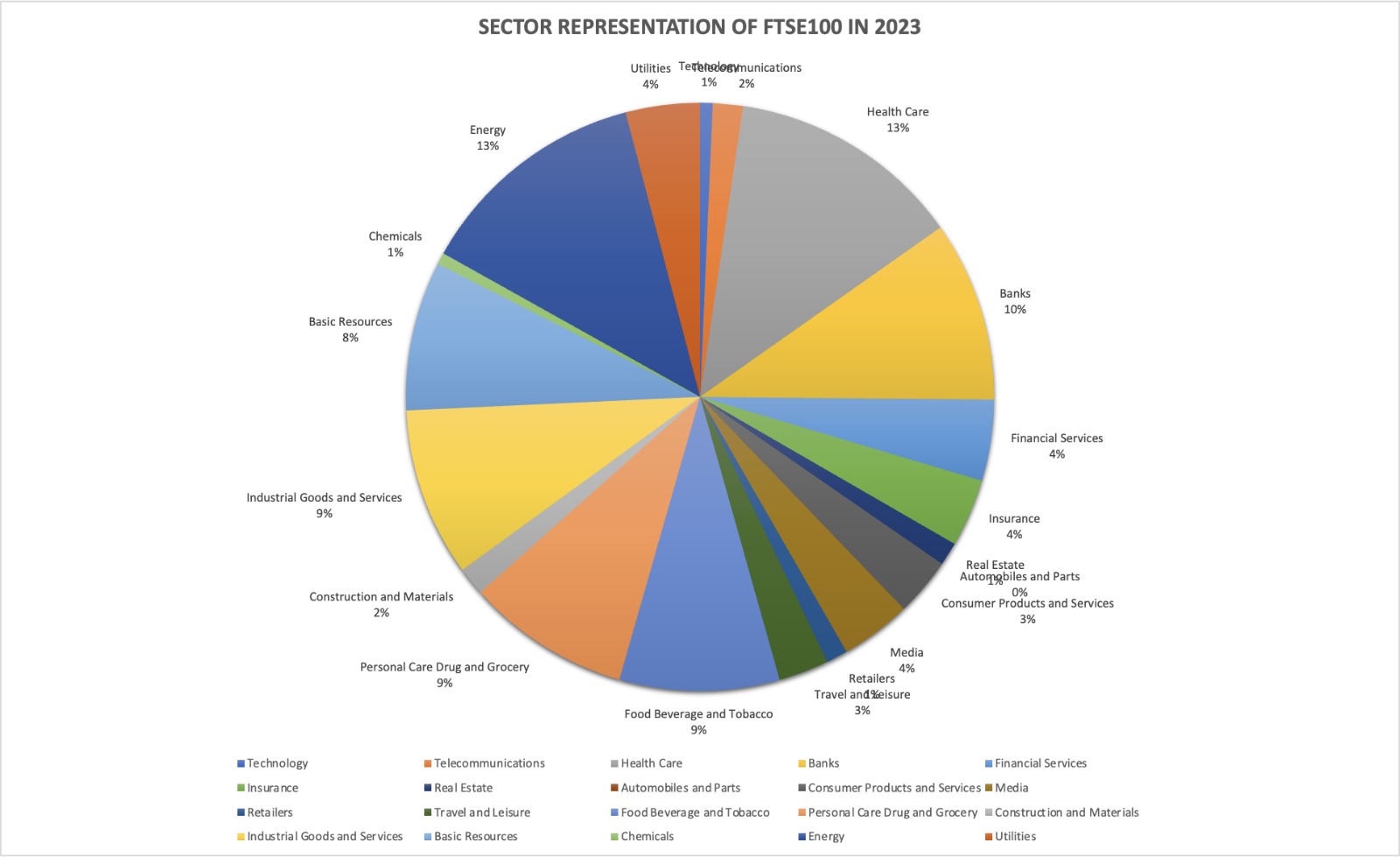

Table 2 below gives the sector representation of the FTSE 100 index in terms of number of stocks and market capitalization as of January 31, 2023.

Table 2. Sector representation in the FTSE 100 index.

Source: computation by the author (data: Yahoo! Finance financial website).

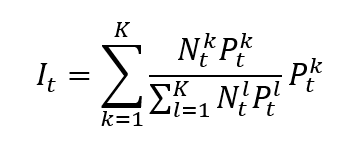

Calculation of the FTSE 100 index value

The FTSE 100 is a market capitalization-weighted index, which means that each company’s weight in the index is determined by its market capitalization, i.e., the total value of all its outstanding shares. The index, which is regarded as the standard index for the UK equity market, includes the 100 largest companies by market capitalization that are listed on the London Stock Exchange.

The formula to compute the FTSE 100 index is given by

Where I is the index value, k a given asset, K the number of assets in the index, Pk the market price of asset k, Nk the number of issued shares for asset k, and t the time of calculation of the index.

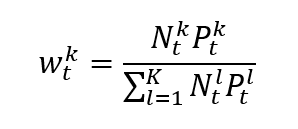

In a market capitalization-weighted index, the weight of asset k is given by formula can be rewritten as

Which clearly shows that the weight of each asset in the index is its market capitalization of the asset divided by the sum of the market capitalizations of all assets.

Note that the divisor, whose calculation is based on the number of shares, is typically adjusted for events such as stock splits and dividends. The divisor is used to ensure that the value of the index remains consistent over time despite changes in the number of outstanding shares.

Use of the FTSE 100 index in asset management

The performance of large-cap companies listed on the London Stock Exchange is frequently measured against the FTSE 100. Investors can gain insight into the overall health of the UK economy and spot potential opportunities or risks in particular industries or regions by examining the sector weightings and geographic exposure of the index. It serves as a benchmark for asset managers to compare the performance of their equity portfolios to the overall market performance.

Benchmark for equity funds

One of the most popular metrics for assessing the performance of the UK stock market is the FTSE 100. It includes businesses from a wide range of sectors, including consumer goods, healthcare, energy, and finance. As a result, it is frequently used by investors and fund managers to monitor the UK economy’s performance and evaluate the country’s investment opportunities.

Financial products around the FTSE 100 index

There are several financial products that track the performance of the FTSE 100 index, allowing investors to gain exposure to the Japanese stock market.

- ETFs are investment funds traded on stock exchanges, designed to track the performance of an index. There are several ETFs that track the FTSE 100 index, such as the iShares Core FTSE 100 ETF and the Vanguard FTSE 100 UCITS ETF.

- index funds are also designed to track the performance of an index. index funds based on the FTSE 100 index include the HSBC FTSE 100 Index Fund and the Legal & General UK 100 Index Fund.

- Futures and options contracts based on the FTSE 100 index provide investors with the ability to speculate on the future performance of the index. For example, the London International Financial Futures and Options Exchange (LIFFE) offers futures contracts based on the FTSE 100 index.

- Certificates are investment products that allow investors to gain exposure to the FTSE 100 index. Société Générale offers a range of certificates linked to the FTSE 100 index, such as the FTSE 100 Tracker Certificate.

Historical data for the FTSE 100 index

How to get the data?

The FTSE 100 index is the most common index used in finance, and historical data for the FTSE 100 index can be easily downloaded from the internet.

For example, you can download data for the FTSE 100 index from January 3, 1984 on Yahoo! Finance (the Yahoo! code for FTSE 100 index is ^FTSE).

Source: Yahoo! Finance.

You can also download the same data from a Bloomberg terminal.

R program

The R program below written by Shengyu ZHENG allows you to download the data from Yahoo! Finance website and to compute summary statistics and risk measures about the FTSE 100 index.

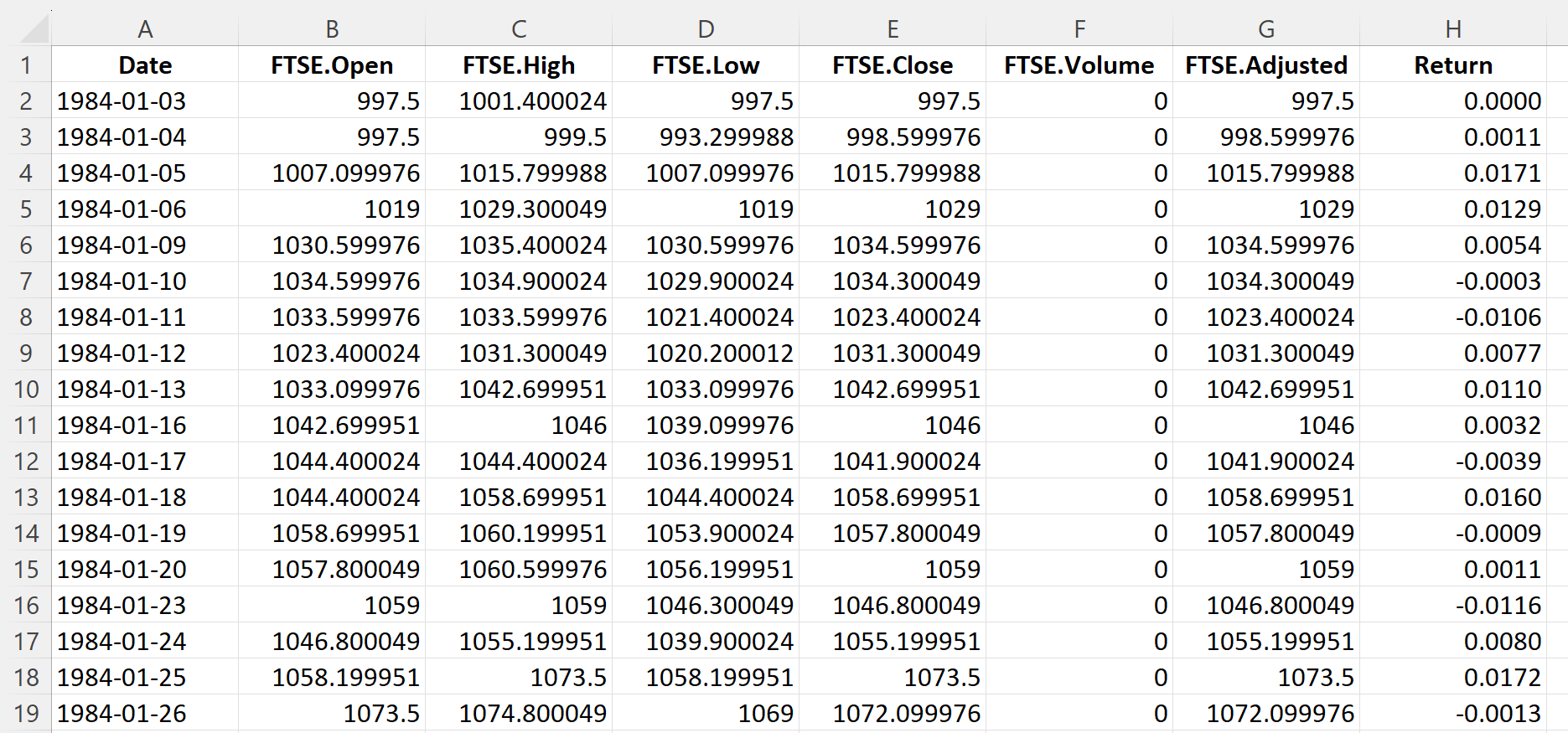

Data file

The R program that you can download above allows you to download the data for the FTSE 100 index from the Yahoo! Finance website. The database starts on January 3, 1984. It also computes the returns (logarithmic returns) from closing prices.

Table 3 below represents the top of the data file for the FTSE 100 index downloaded from the Yahoo! Finance website with the R program.

Table 3. Top of the data file for the FTSE 100 index.

Source: computation by the author (data: Yahoo! Finance website).

Evolution of the FTSE 100 index

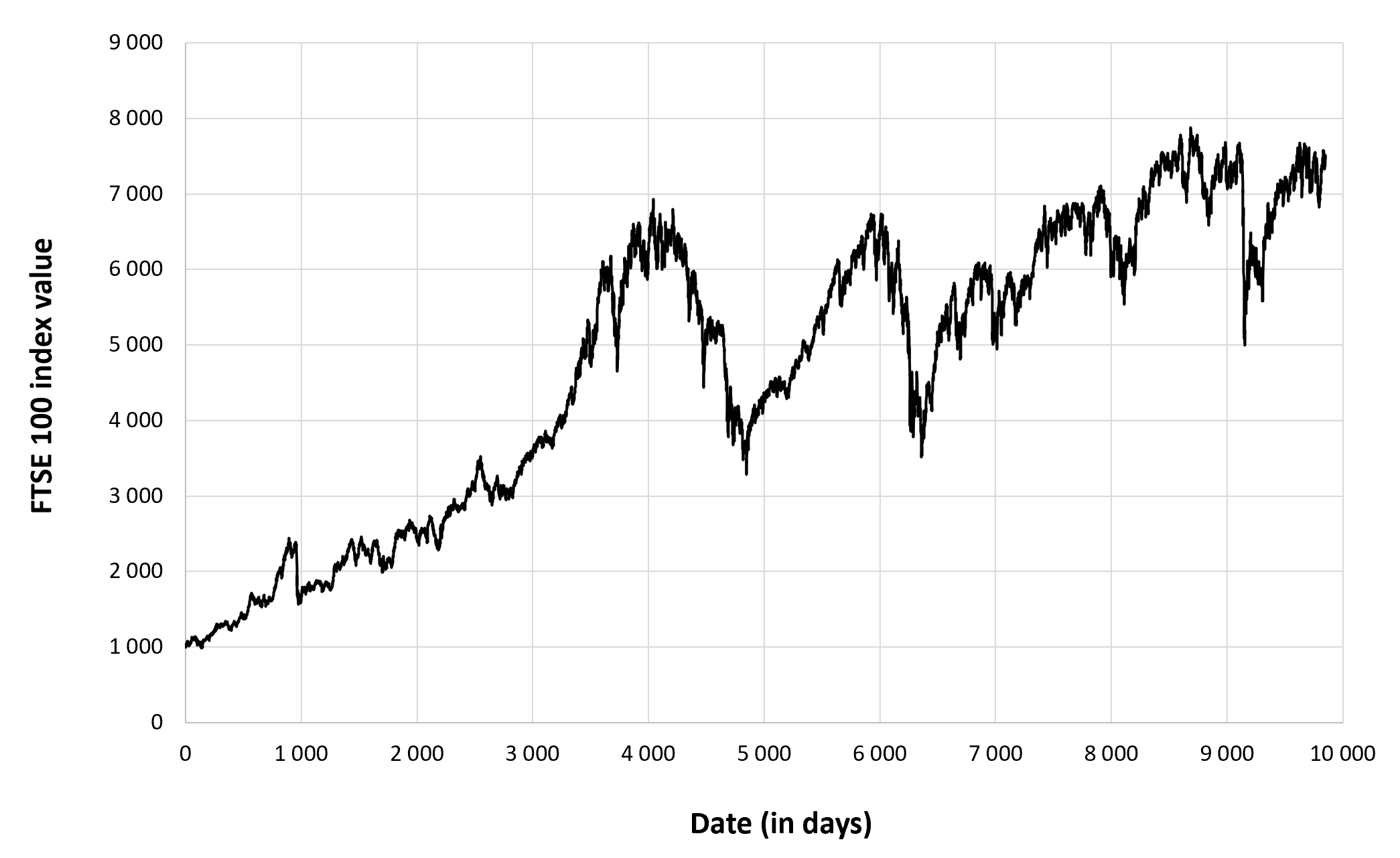

Figure 1 below gives the evolution of the FTSE 100 index from January 3, 1984 to December 30, 2022 on a daily basis.

Figure 1. Evolution of the FTSE 100 index.

Source: computation by the author (data: Yahoo! Finance website).

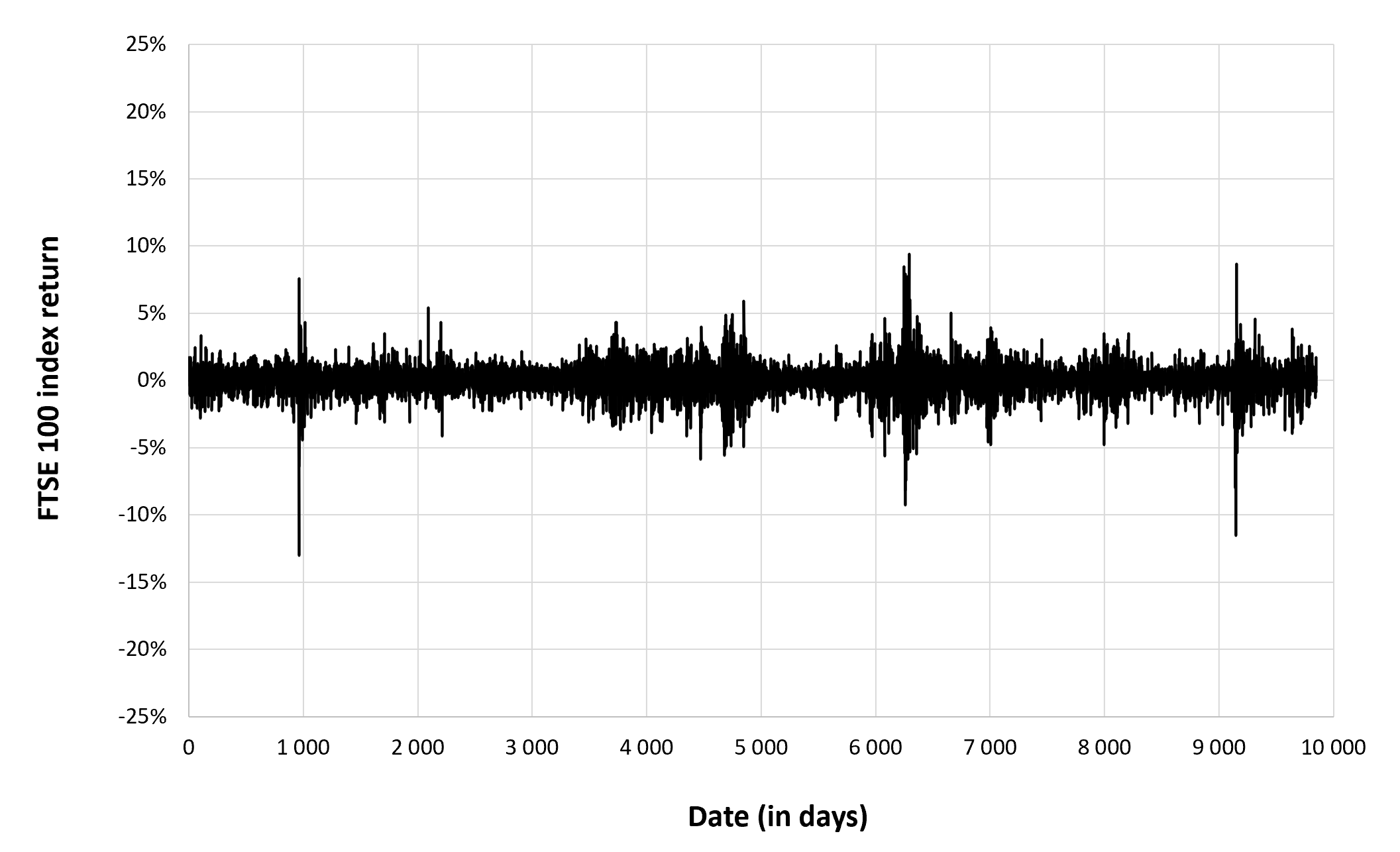

Figure 2 below gives the evolution of the FTSE 100 index returns from January 3, 1984 to December 30, 2022 on a daily basis.

Figure 2. Evolution of the FTSE 100 index returns.

Source: computation by the author (data: Yahoo! Finance website).

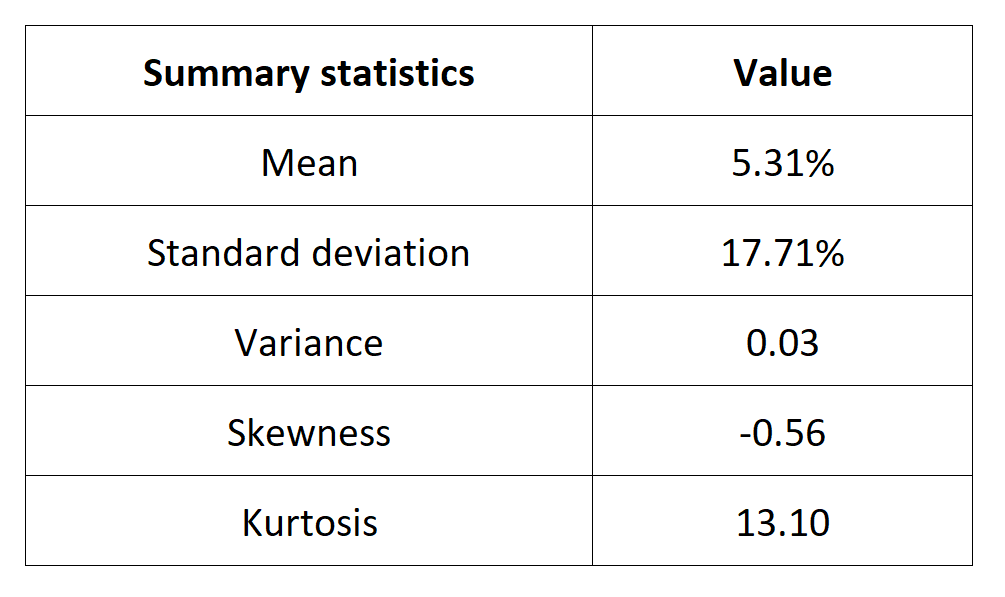

Summary statistics for the FTSE 100 index

The R program that you can download above also allows you to compute summary statistics about the returns of the FTSE 100 index.

Table 4 below presents the following summary statistics estimated for the FTSE 100 index:

- The mean

- The standard deviation (the squared root of the variance)

- The skewness

- The kurtosis.

The mean, the standard deviation / variance, the skewness, and the kurtosis refer to the first, second, third and fourth moments of statistical distribution of returns respectively.

Table 4. Summary statistics for the FTSE 100 index.

Source: computation by the author (data: Yahoo! Finance website).

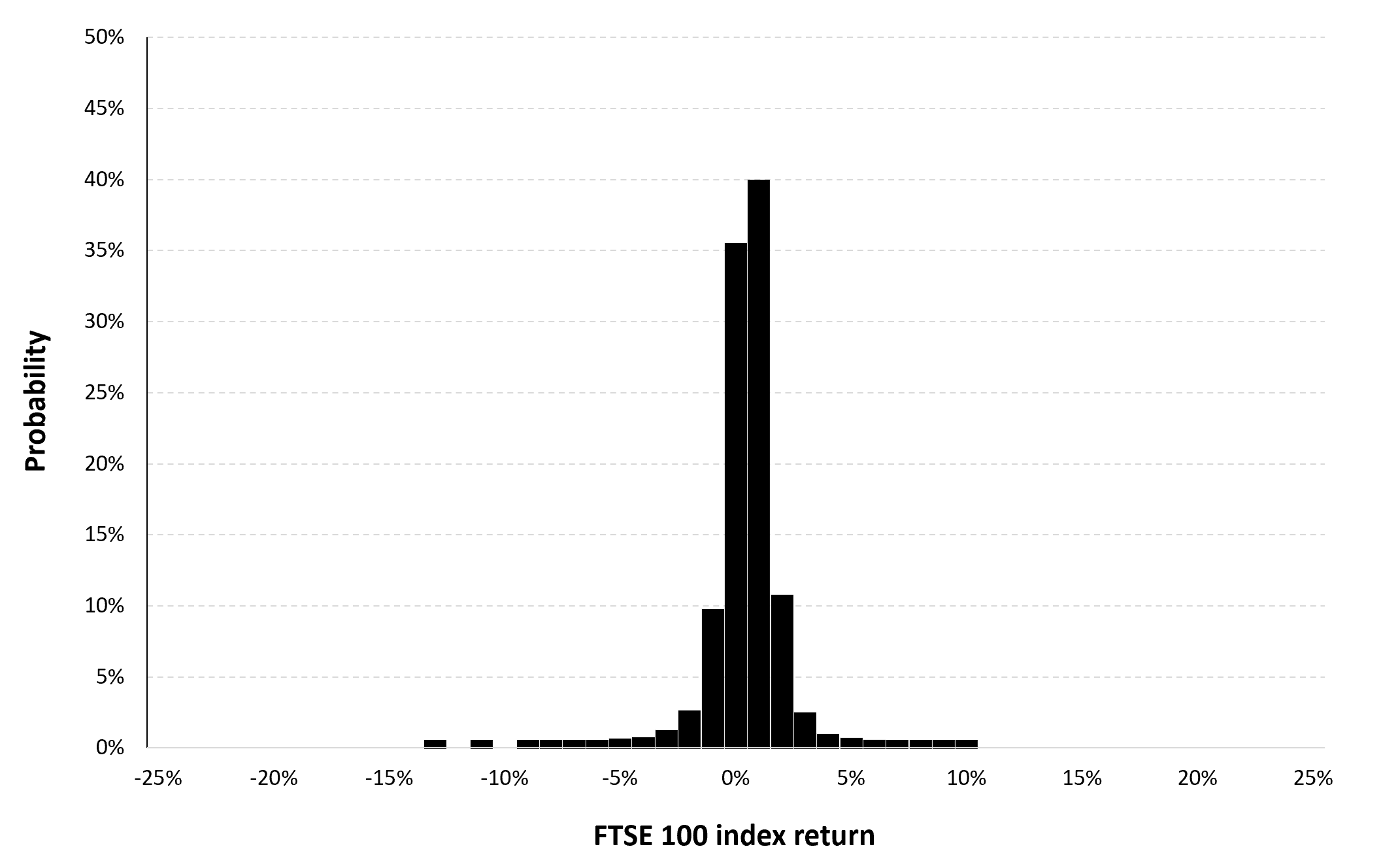

Statistical distribution of the FTSE 100 index returns

Historical distribution

Figure 3 represents the historical distribution of the FTSE 100 index daily returns for the period from January 3, 1984 to December 30, 2022.

Figure 3. Historical distribution of the FTSE 100 index returns.

Source: computation by the author (data: Yahoo! Finance website).

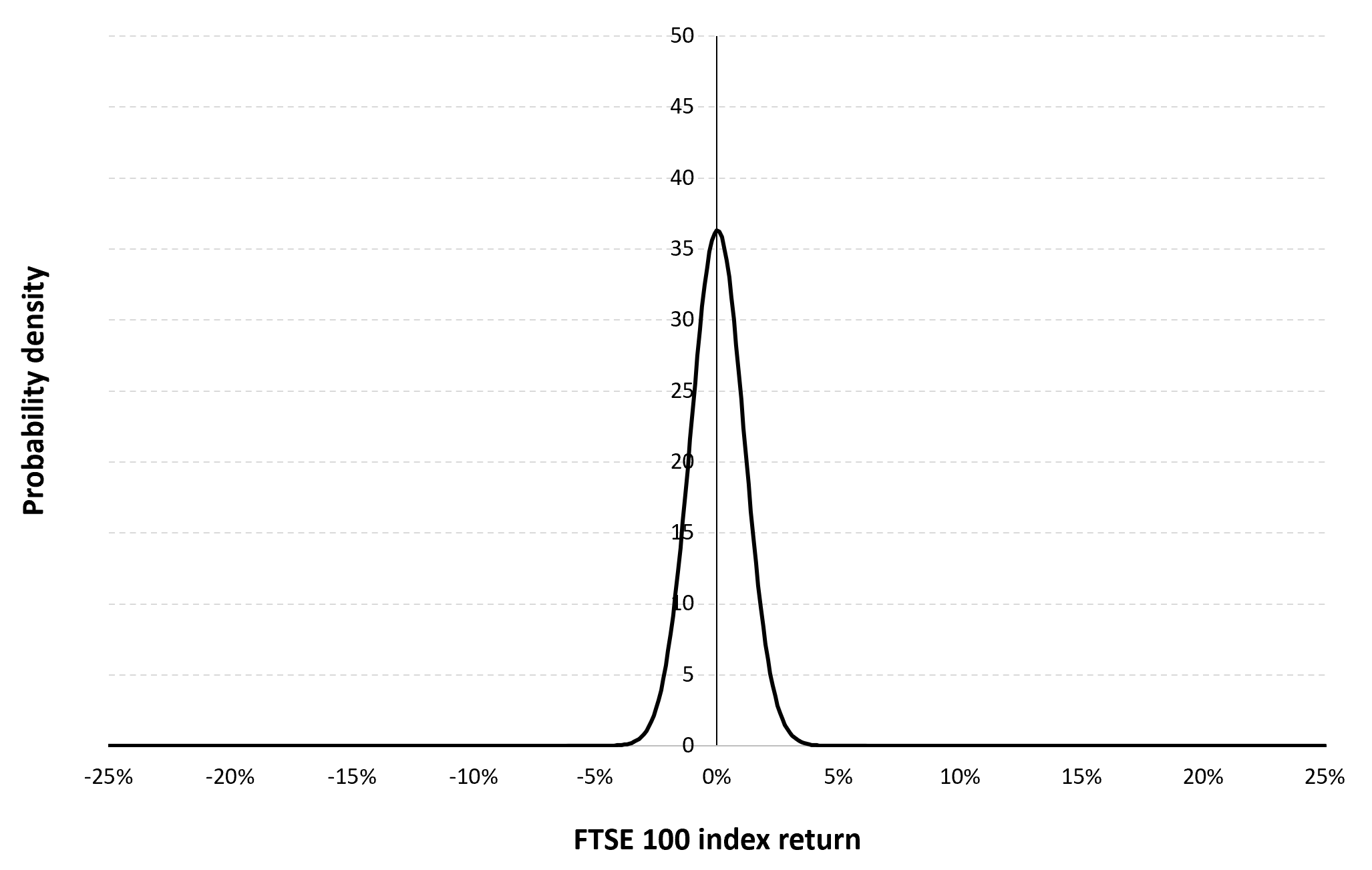

Gaussian distribution

The Gaussian distribution (also called the normal distribution) is a parametric distribution with two parameters: the mean and the standard deviation of returns. We estimated these two parameters over the period from January 3, 1984 to December 30, 2022. The mean of daily returns is equal to 0.02% and the standard deviation of daily returns is equal to 1.37% (or equivalently 3.94% for the annual mean and 28.02% for the annual standard deviation as shown in Table 3 above).

Figure 4 below represents the Gaussian distribution of the FTSE 100 index daily returns with parameters estimated over the period from January 3, 1984 to December 30, 2022.

Figure 4. Gaussian distribution of the FTSE 100 index returns.

Source: computation by the author (data: Yahoo! Finance website).

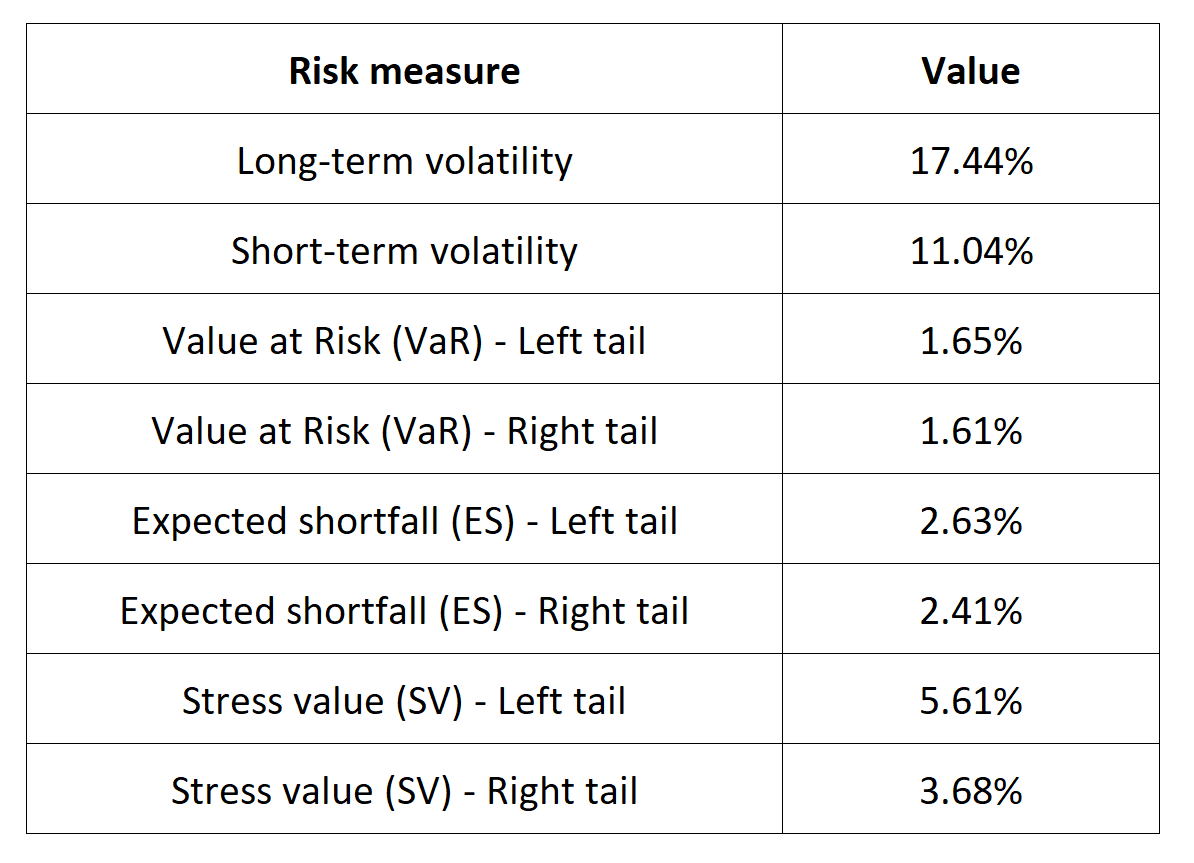

Risk measures of the FTSE 100 index returns

The R program that you can download above also allows you to compute risk measures about the returns of the FTSE 100 index.

Table 5 below presents the following risk measures estimated for the FTSE 100 index:

- The long-term volatility (the unconditional standard deviation estimated over the entire period)

- The short-term volatility (the standard deviation estimated over the last three months)

- The Value at Risk (VaR) for the left tail (the 5% quantile of the historical distribution)

- The Value at Risk (VaR) for the right tail (the 95% quantile of the historical distribution)

- The Expected Shortfall (ES) for the left tail (the average loss over the 5% quantile of the historical distribution)

- The Expected Shortfall (ES) for the right tail (the average loss over the 95% quantile of the historical distribution)

- The Stress Value (SV) for the left tail (the 1% quantile of the tail distribution estimated with a Generalized Pareto distribution)

- The Stress Value (SV) for the right tail (the 99% quantile of the tail distribution estimated with a Generalized Pareto distribution)

Table 5. Risk measures for the FTSE 100 index.

Source: computation by the author (data: Yahoo! Finance website).

The volatility is a global measure of risk as it considers all the returns. The Value at Risk (VaR), Expected Shortfall (ES) and Stress Value (SV) are local measures of risk as they focus on the tails of the distribution. The study of the left tail is relevant for an investor holding a long position in the FTSE 100 index while the study of the right tail is relevant for an investor holding a short position in the FTSE 100 index.

Why should I be interested in this post?

For a number of reasons, management students (as future managers and individual investors) should learn about the FTSE 100 index. The FTSE 100 index is a key benchmark for the Japanese equity market, which is one of the world’s largest market. Understanding how the index is constructed, how it performs, and the companies that make up the index is important for anyone studying finance or business in Japan or interested in investing in Japanese equities.

Individual investors can assess the performance of their own investments in the Japanese equity market with the FTSE 100 index. Last but not least, a lot of asset management firms base their mutual funds and exchange-traded funds (ETFs) on the FTSE 100 index which can considered as interesting assets to diversify a portfolio. Learning about these products and their portfolio and risk management applications can be valuable for management students.

Related posts on the SimTrade blog

About financial indexes

▶ Nithisha CHALLA Financial indexes

▶ Nithisha CHALLA Calculation of financial indexes

▶ Nithisha CHALLA The business of financial indexes

▶ Nithisha CHALLA Float

Other financial indexes

▶ Nithisha CHALLA The S&P 500 index

▶ Nithisha CHALLA The CSI 300 index

▶ Nithisha CHALLA The Nikkei 225 index

▶ Nithisha CHALLA The DAX 30 index

About portfolio management

▶ Youssef LOURAOUI Portfolio

▶ Jayati WALIA Returns

About statistics

▶ Shengyu ZHENG Moments de la distribution

▶ Shengyu ZHENG Mesures de risques

Useful resources

Academic research about risk

Longin F. (2000) From VaR to stress testing: the extreme value approach Journal of Banking and Finance, N°24, pp 1097-1130.

Longin F. (2016) Extreme events in finance: a handbook of extreme value theory and its applications Wiley Editions.

Business

Axi What is the FTSE 100 index and how to trade it?

CMC markets An introduction to the FTSE 100

Nerd Wallet What is the FTSE 100?

Data

Yahoo Finance FTSE 100 index

About the author

The article was written in April 2023 by Nithisha CHALLA (ESSEC Business School, Grande Ecole Program – Master in Management, 2021-2023).