In this article, Saral BINDAL (Indian Institute of Technology Kharagpur, Metallurgical and Materials Engineering, 2024-2028 & Research assistant at ESSEC Business School) explains how option prices can be used to build an implied risk-neutral distribution.

Introduction

Derivative markets provide a rich source of information for market expectations. For example, a futures price is the market’s expectation of the future value of an asset. More interestingly, we can derive the moments of the statistical distribution of future asset values from the market prices of options, like the variance (second moment), the skewness (third moment) and the kurtosis (fourth moment). More generally, we can extract the ex-ante risk-neutral probability distribution of future asset prices at a given date from option market prices with the corresponding maturity date.

Physical vs Risk-Neutral Probability Measures

A real-world probability measure represents the statistical distribution of asset returns typically estimated using historical data. These measures incorporate risk premia, market frictions, and investor behaviour, and are primarily used for statistical inference and risk modelling.

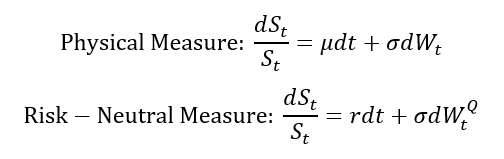

In contrast, risk-neutral probability measure is a mathematical pricing measure used in no-arbitrage valuation of financial derivatives. Under this framework, asset prices are evaluated as discounted expected payoffs under an equivalent martingale measure. In this setting, the expected return of any risky asset is adjusted to the risk-free rate within the pricing measure, simplifying valuation by transforming uncertain future payoffs into present values computed via expectation (Hull, 2018; Shreve, 2004).

Historical vs Risk-Neutral Distributions

Historical Distributions are constructed from observed past returns under the physical measure (P-measure). They empirically capture the true statistical behaviour of asset prices, including fat tails, skewness, and volatility clustering driven by real market shocks and investor behaviour. These distributions exhibit higher variance and kurtosis, making them particularly valuable for stress testing, Value-at-Risk estimation, and portfolio risk management where realistic loss scenarios matter.

Risk-Neutral Distributions are derived from option market prices rather than historical data, under the implied measure by no-arbitrage pricing (Q-measure). They reflect market-implied expectations of future payoffs discounted at the risk-free rate resulting in smoother, less skewed densities. While highly effective for pricing derivatives and contingent claims, they tend to underestimate tail risk and do not directly represent the actual probabilities investors assign to future market outcomes.

Risk-neutral distribution: the Black–Scholes–Merton framework

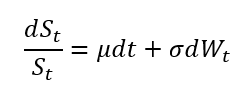

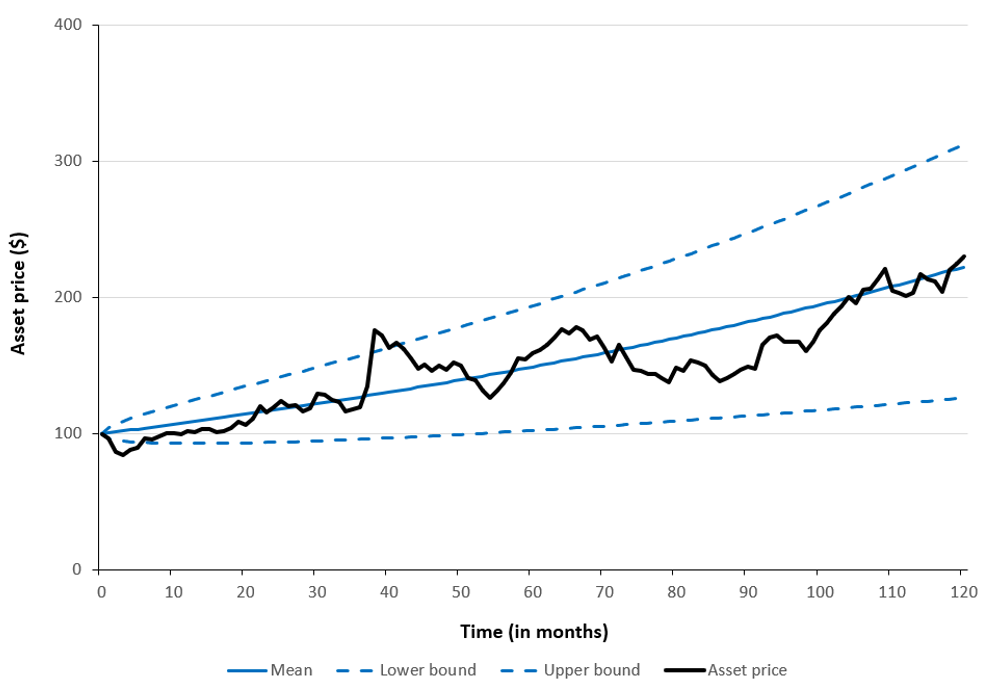

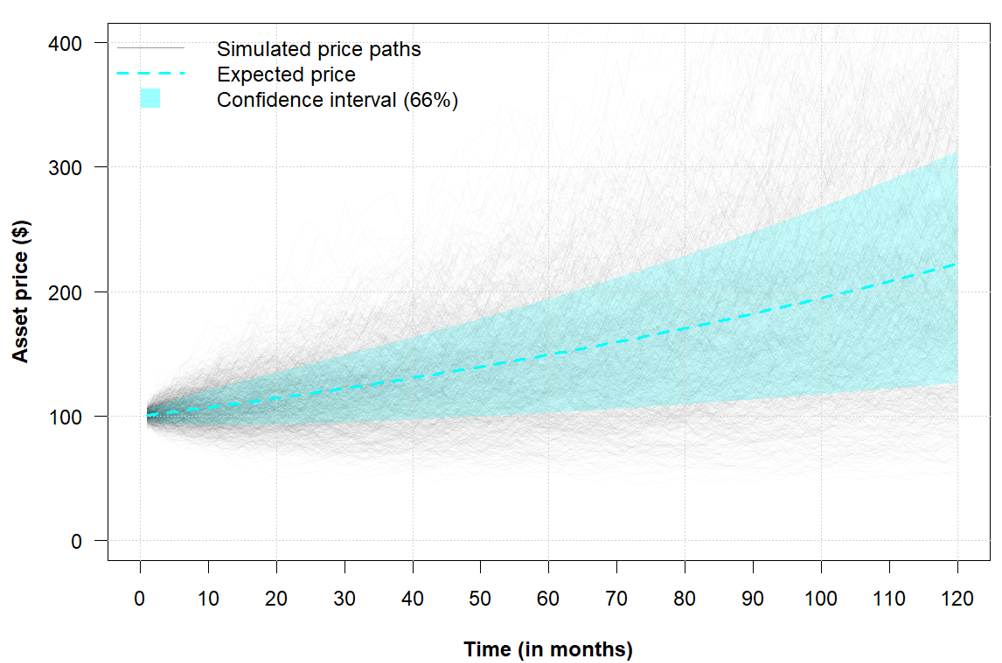

Having distinguished between the physical and risk-neutral probability measures, it is useful to examine the risk-neutral distribution implied by the Black–Scholes–Merton (BSM) model, which is a standard model in quantitative finance. The BSM framework assumes that the underlying asset follows a geometric Brownian motion and provides a simple illustration of how the transition from the physical measure to the risk-neutral measure alters the distribution of future asset prices.

Under the BSM, the standard assumption is that the underlying asset follows a geometric Brownian motion given by the following expressions:

where:

- St = asset price at time t t

- μ = drift (growth rate of the asset price)

- r = risk-free rate

- σ = volatility (standard deviation)

- dWt/dWtQ = infinitesimal increment of wiener process (N(0,dt)) under respective measures

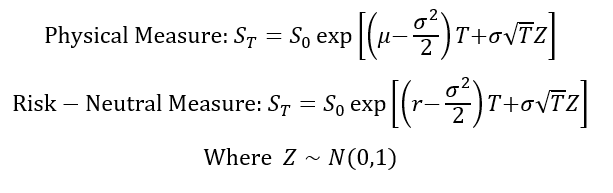

Solving these stochastic differential equations over the interval [0, T] yields the terminal asset price:

Taking logarithms shows that the terminal log-price is normally distributed:

Thus, under the Black–Scholes–Merton framework, the risk-neutral distribution of the terminal asset price is lognormal (as the physical distribution). Relative to the corresponding physical distribution, the volatility remains unchanged, while the drift parameter μ is replaced by the risk-free rate r. This is an important result as the risk-free rate r is known and easily observable while the drift parameter μ has to be estimated and is not directly observable.

Butterfly spread

To extract a continuous risk-neutral probability distribution from the market, we must first understand how to isolate the market’s view on a specific future asset price. The primary tool for this is a classic option trading strategy: the butterfly spread.

A butterfly spread is an options trading strategy designed to achieve limited profit with strictly bounded risk, typically in market environments where relatively small price movements are anticipated. The strategy may be implemented using either call or put options and can be established in either a long or short configuration. For example, a long call butterfly is constructed by purchasing one call option at a lower strike price, selling two call options at an intermediate strike price, and purchasing one call option at a higher strike price. Depending on the relative spacing between the strike prices, a butterfly spread may be either symmetric or asymmetric.

Cost of a Symmetric Butterfly Spread

To understand how option market prices encode the market’s expectations regarding the future distribution of the underlying asset price, we consider a symmetric butterfly. A symmetric butterfly spread is constructed using three European call options with a common maturity T and distinct strike prices. The strategy involves purchasing one call option with strike K – ΔK at a premium of C(K-ΔK,T), selling two call options with strike K at a premium of C(K,T) each, and purchasing one call option with strike K + ΔK at a premium of C(K+ΔK,T).

The price of the resulting butterfly spread is therefore given by

The net cost of the butterfly spread is obtained by summing the premia paid for the two long call positions and subtracting the premiums received from the two short call positions.

Payoff of a Symmetric Butterfly Spread

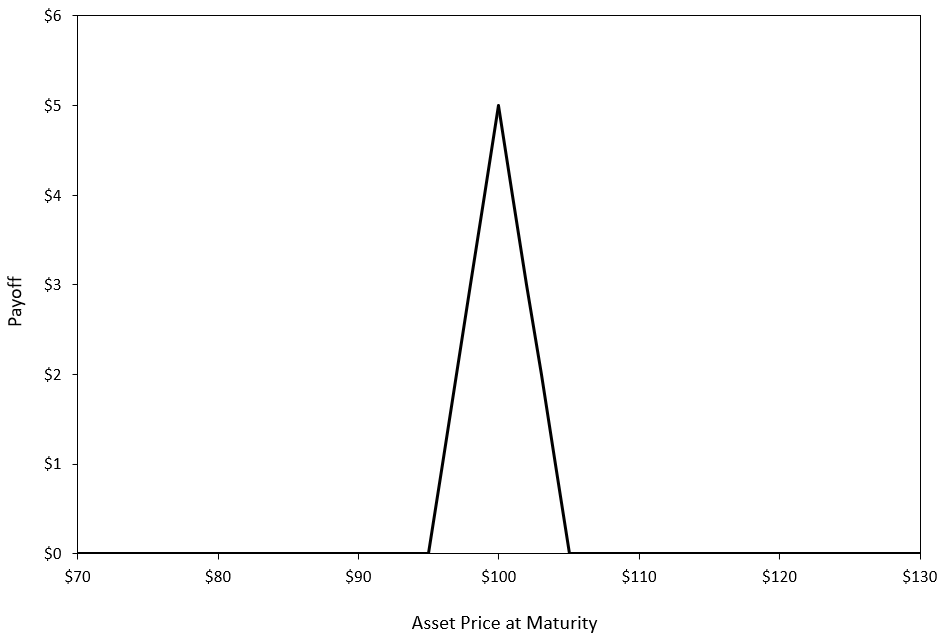

The payoff of a symmetric butterfly spread is centred around the strike (K) and can be expressed as

Figure 1 illustrates the payoff profile of a symmetric butterfly spread centred at the strike K = 100 with strike spacing ΔK = 5. The payoff reaches its maximum when the terminal asset price ST equals the strike K and declines to zero as ST moves beyond the adjacent strikes K – ΔK and K + ΔK.

Figure 1. Symmetric Butterfly Spread Payoff at Maturity

Source: computation by the author.

As a result, the butterfly spread effectively isolates a narrow range of terminal asset prices, making it a useful instrument for extracting information about the market-implied probability distribution of the underlying asset price at maturity.

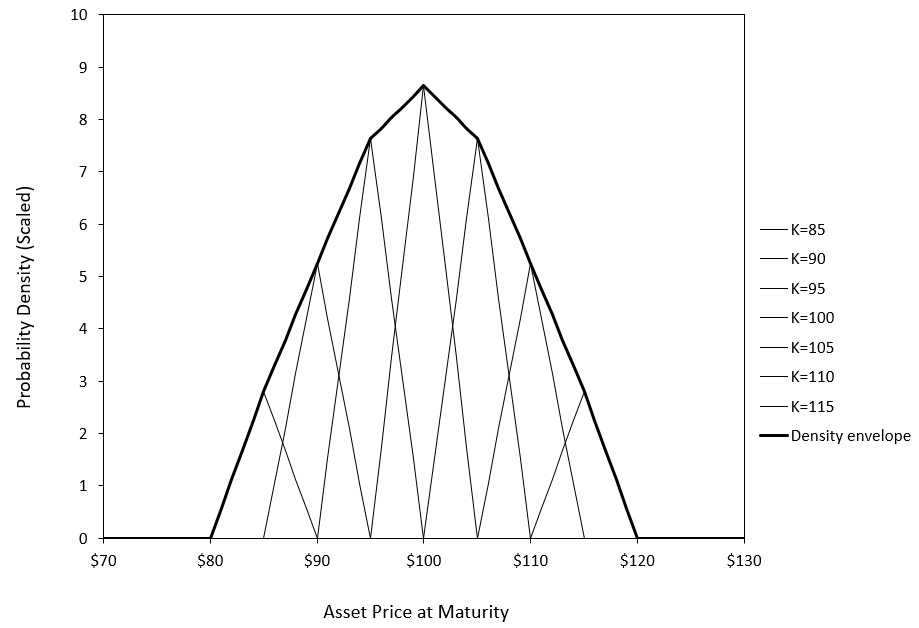

Stacked Butterfly Spreads

A stack of butterfly spreads refers to a collection of butterfly spreads constructed across a range of strike prices, such that the central strike of each butterfly is equally spaced from the next. The spacing between successive central strikes is equal to the strike spacing ΔK used in the construction of each individual butterfly spread, as discussed above.

Figure 2 illustrates that a collection of butterfly spreads across strikes at a fixed maturity converges to the market-implied probability density of the underlying asset. Each butterfly corresponds to a discrete approximation of the second derivative of option prices with respect to strike, and aggregating these across strikes recovers the risk-neutral density.

We construct seven butterfly spreads centered at strikes K = 85 to K = 115 in increments of 5, with strike spacing ΔK = 5. The weights are specified using a Gaussian distribution with mean μ = 100 and standard deviation σ = 10, reflecting an assumed market belief about the concentration of terminal prices. The payoff profile is scaled by a factor of 200 to improve visual readability, and it is normalized by ΔK2 to remain consistent with the second-order finite-difference interpretation of butterfly spreads as detailed below.

Figure 2. Approximating the Risk-Neutral Density Using Butterfly Spreads

Source: computation by the author.

As the strike spacing ΔK is reduced, additional butterfly spreads can be constructed between existing butterfly spreads. Consequently, the stacked payoff profile becomes increasingly smooth and, in the limit, approaches a continuous representation of the implied probability distribution.

To better understand this limiting behaviour, it is useful to examine the properties of an individual butterfly spread. As the strike spacing ΔK decreases, the payoff of the butterfly spread becomes increasingly concentrated around its central strike. In the limit as ΔK → 0, the butterfly spread approaches an infinitesimally narrow peak centred at K.

Consequently, the value of the butterfly spread decreases as its payoff becomes increasingly concentrated around its central strike. To obtain a meaningful limiting quantity, the butterfly value must therefore be normalized by (ΔK)2. This normalization is motivated by a well-known result from calculus, central finite-difference approximation of the second derivative.

Comparing the two expressions above, reveals that the normalized butterfly value is precisely the finite-difference approximation of the second derivative of the call pricing function with respect to strike.

This observation forms the foundation of the Breeden-Litzenberger (1978) result, which establishes that the second derivative of the call pricing function with respect to strike is directly related to the market-implied risk-neutral probability density embedded in option prices, as demonstrated in the derivation below.

You can download the Excel file provided below to generate and visualize the payoff profiles of the butterfly spread and stacked butterfly spread at maturity, as discussed above.

Option implied risk-neutral distribution

This section develops the analytical derivation of the risk-neutral distribution using the seminal Breeden-Litzenberger (1978) result. By exploiting the cross-sectional structure of option prices across strikes, we recover the market-implied risk-neutral density embedded in option market prices.

Analytical derivation

Under the risk-neutral measure, the value of a European call option is given by the present value of its expected payoff at maturity. For a strike price K, continuously compounded risk-free rate r, and time to maturity T, the call pricing function C(K,T) can be expressed as

To obtain a continuous representation of the call price, the expected payoff can be expressed as an integral over the probability density function of the terminal asset price, f(ST).

Note: The integral starts at K because the payoff is zero when St≤K.

Taking the first derivative with respect to K, we get

To obtain the risk-neutral probability density function, as shown by Breeden and Litzenberger (1978), we take an additional derivative with respect to the strike

Rearranging the above formula, we get the risk-neutral distribution

Applying the second-order central difference approximation heuristically developed in the previous section using butterfly spreads, we obtain the following expression:

This expression shows that the risk-neutral probability density can be recovered directly from the second derivative of the call pricing function with respect to strike. In practice, however, option prices are observed only at a finite set of discrete strike prices, requiring numerical methods to approximate the derivatives and extract the implied risk-neutral distribution.

Numerical methods for extracting the risk-neutral distribution

Methods for extracting the risk-neutral distribution can be broadly classified into non-parametric (data-driven with minimal distributional assumptions), semi-parametric (partial structural assumptions, typically imposed on intermediate quantities such as implied volatility), and parametric or structural (explicit assumptions on the distribution or asset price dynamics) approaches. These methodologies differ in the degree of modelling assumptions imposed on the option pricing function and the terminal asset price distribution, leading to different trade-offs between flexibility, numerical stability, and economic interpretability.

Non-parametric methods

Non-parametric methods aim to recover the risk-neutral distribution directly from observed option prices without imposing any specific parametric structure on either the terminal asset price distribution or the stochastic process governing the evolution of the underlying asset price. Consequently, these methods are highly flexible, but they tend to be sensitive to market microstructure noise, sparse strike coverage, and interpolation error in option quotes.

Risk-neutral histograms: the most direct implementation of the Breeden–Litzenberger result constructs a discrete approximation of the implied risk-neutral density using finite differences across traded strikes (Breeden and Litzenberger, 1978; Neuhaus, 1995). Adjacent butterfly spreads may therefore be interpreted as local estimates of state-contingent probabilities.

Because option contracts are quoted only at discrete strike intervals, the recovered distribution resembles a histogram rather than a smooth continuous density, making the approach highly sensitive to strike spacing and pricing noise.

Kernel regression methods: to mitigate the instability of histogram-based estimates, subsequent research introduced non-parametric smoothing techniques that estimate a continuous option pricing function directly from observed market prices. A prominent example is the kernel regression framework of Aït-Sahalia and Lo (1998).

By reducing the influence of local pricing noise, kernel-based methods generally produce smoother and more stable estimates of the implied risk-neutral density.

Spline-based methods: another widely used class of non-parametric methods employs spline interpolation techniques to construct smooth and arbitrage-consistent call pricing functions across strikes (Bates, 1991). Once a sufficiently smooth pricing function has been obtained, the implied risk-neutral density can be recovered through numerical differentiation.

Spline-based approaches offer substantial flexibility but remain sensitive to data quality and sparse observations in the tails of the distribution.

Semi-parametric approaches

Semi-parametric approaches occupy a middle ground between purely data-driven and fully parametric methodologies. Rather than modelling the risk-neutral density directly, these methods impose structure on intermediate quantities, most commonly the implied volatility smile.

Implied volatility smile methods: in practice, many market participants smooth the implied volatility smile rather than the option prices directly. Observed option prices are first converted into implied volatilities, after which a smooth volatility smile is fitted across strikes using parametric specifications or spline-based interpolation techniques (Shimko, 1993).

The smoothed volatility smile is subsequently mapped back into option prices, allowing the implied risk-neutral density to be recovered through numerical differentiation. These methods generally exhibit greater numerical stability, although tail estimation remains sensitive to extrapolation assumptions in illiquid regions of the smile.

Parametric and structural approaches

Parametric and structural methodologies recover the implied risk-neutral distribution by imposing explicit assumptions on either the terminal distribution of asset prices or the stochastic process governing their evolution.

Parametric density models: a prominent class of methods assumes that the terminal risk-neutral distribution follows a particular parametric specification. One widely used approach models the distribution as a mixture of lognormal densities calibrated to observed option prices (Bahra, 1997; Melick and Thomas, 1997).

Parametric methods are computationally efficient and often yield economically interpretable measures of skewness, kurtosis, and tail risk. Their flexibility, however, is inherently constrained by the assumed functional form.

Dynamic option pricing models: rather than specifying the terminal distribution directly, structural approaches derive the implied density from an assumed stochastic process governing the evolution of the underlying asset price. Examples include stochastic volatility and jump-diffusion frameworks calibrated to observed option prices (Bates, 1995; Malz, 1995).

Within these models, the risk-neutral density emerges endogenously from the dynamics of the underlying asset under the risk-neutral measure. While theoretically appealing, such models are computationally intensive and sensitive to model misspecification.

Application

Implementing the Breeden and Litzenberger (1978) result in practice requires a continuum of European option prices written on the same underlying asset, all sharing a common maturity and spanning a continuous range of strike prices from zero to infinity. Under such idealized conditions, the risk-neutral density can be recovered directly from the cross-section of option prices (at a given maturity date).

In practice, however, listed option markets provide only a sparse and discrete grid of strike prices, typically concentrated around the at-the-money (ATM) region. The absence of a complete continuum of option strikes, particularly in the deep in-the-money and far out-of-the-money regions, necessitates the use of interpolation across observed strikes and extrapolation into the tails in order to recover a smooth and arbitrage-free implied risk-neutral distribution.

Required data

Constructing a risk-neutral distribution requires option chain data (a set of calls and/or puts) for a single maturity, along with the underlying asset price, the prevailing risk-free rate, dividend assumptions, at the exact observation time of the market data.

Such data can be obtained from both free and commercial data providers. One of the most accessible sources is Yahoo! Finance; however, freely available option data is often subject to inconsistencies such as wide bid–ask spreads, stale quotes, and incomplete cross-sectional coverage of strikes, all of which can materially distort empirical estimation of the risk-neutral distribution (RND).

For our application, we employ simulated option data to illustrate the derivation of the implied risk-neutral distribution from an option chain within a controlled and internally consistent setting. This ensures that the resulting distribution remains aligned with the theoretical framework developed above.

Extraction of the implied risk-neutral density

From the collected option chain data, we first apply a series of standard filtering procedures designed to remove illiquid and economically inconsistent observations. In empirical applications, this typically includes liquidity screens, moneyness and maturity filters, implied-volatility sanity checks, and no-arbitrage constraints to mitigate errors arising from stale quotes, asynchronous observations, and market microstructure noise. Since the dataset employed here is simulated and internally consistent by construction, these preprocessing steps can be largely omitted.

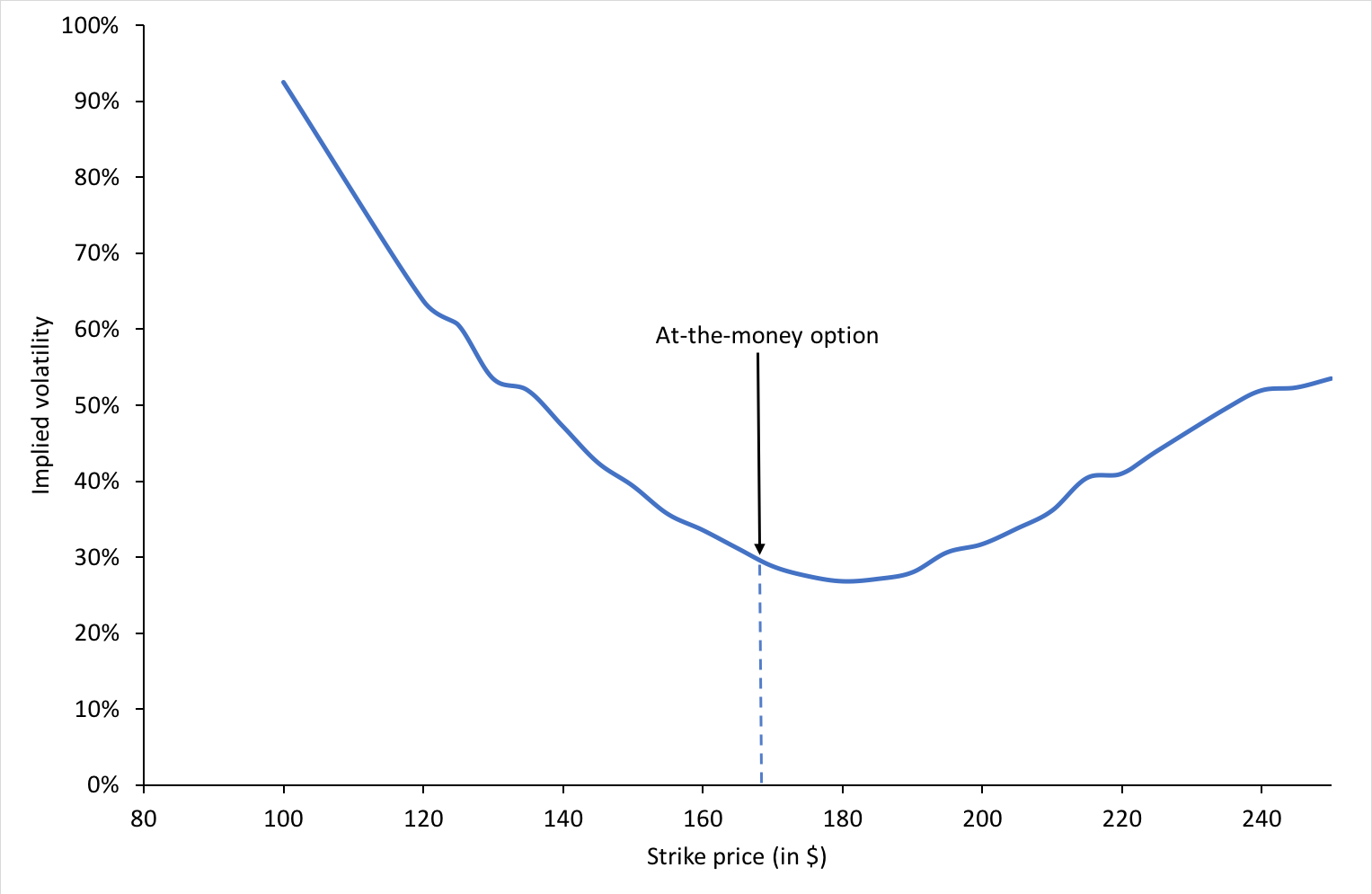

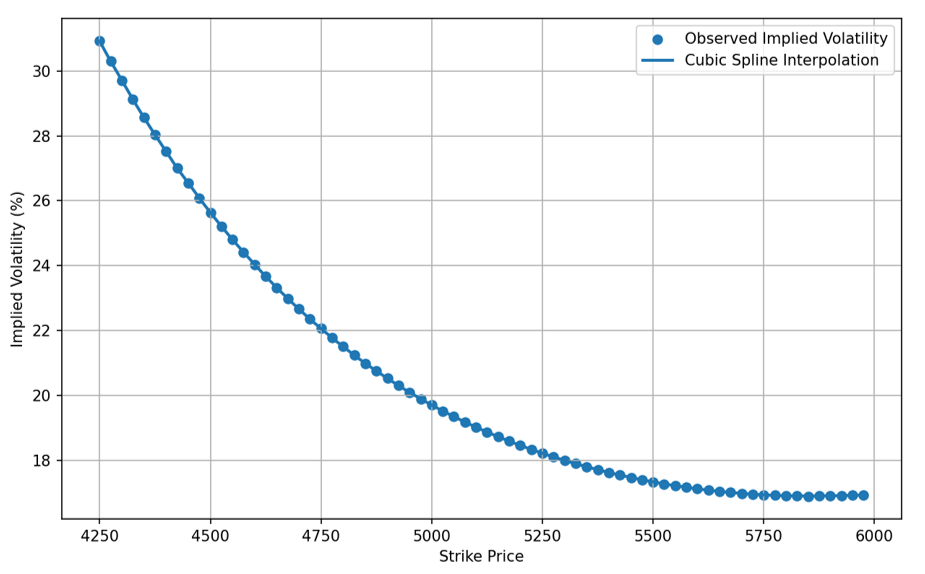

Figure 3 below presents the implied volatility smile obtained from the simulated European call option chain after numerical inversion of the Black–Scholes–Merton pricing model. The smile is interpolated using a natural cubic spline over a dense strike grid spanning the filtered strike range of 4,000 to 6,000, under the assumptions of an underlying spot price of $5,300, a continuously compounded risk-free interest rate of 5.2%, and a remaining time-to-maturity of 30 days. The resulting smooth volatility curve serves as the key intermediate input for constructing a continuous and differentiable call pricing function required for subsequent risk-neutral density extraction.

Figure 3. Implied Volatility Smile

Source: computation by the author (with python)

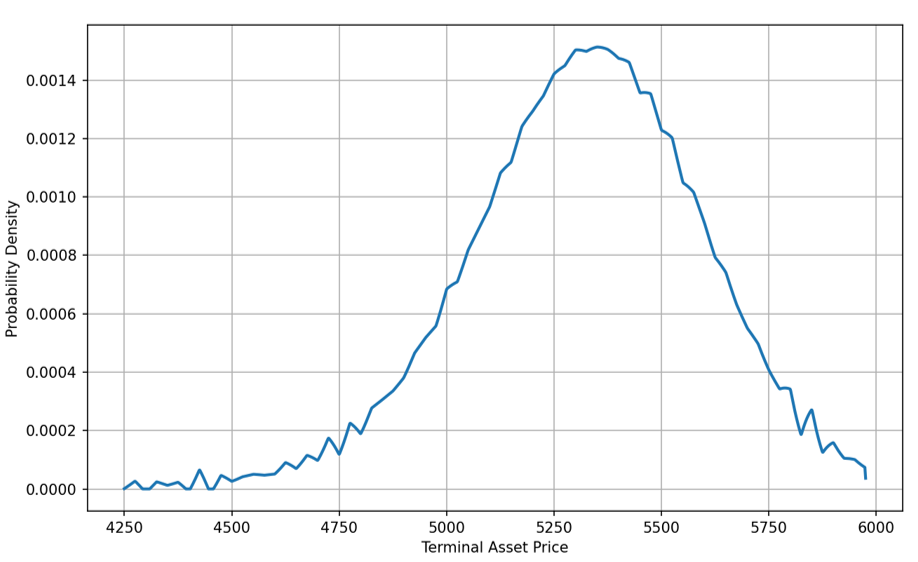

The interpolated implied volatility smile is subsequently utilized to reprice European call options across a finely discretized strike grid, thereby constructing a smooth numerical approximation of the cross-sectional call price surface. The option implied risk neutral density is then recovered by applying the Breeden Litzenberger operator, corresponding to the second partial derivative of discounted call prices with respect to strike, to the smoothed pricing function. Figure 4 illustrates the resulting risk neutral density extracted from the simulated European call option chain under an underlying spot level of $5,300, a continuously compounded risk-free interest rate of 5.2%, and a remaining time to maturity of 30 days.

Figure 4. Implied Risk-Neutral Distribution

Source: computation by the author (with python)

You can download the Python code provided below for generating simulated call option chain data and the option-implied risk-neutral distribution, as discussed above.

Alternatively, you can download the R code below with the same functionality as in the Python file.

Empirical issues

A primary limitation in empirical recovery of the risk-neutral distribution is the discrete nature of listed option strikes. The Breeden–Litzenberger framework assumes a continuum over strike space, whereas traded options are observed only on a sparse and uneven grid concentrated around the at-the-money region.

A second limitation arises from the unobservability of the distribution tails. Deep in-the-money and far out-of-the-money options are often illiquid or not quoted, implying that tail behaviour of the risk-neutral density must be inferred through extrapolation rather than direct market observation.

A separate issue is asynchronous option quotes. Since option prices across strikes are not necessarily recorded simultaneously, the resulting cross-section may embed timing mismatches, introducing bias in the reconstructed pricing function. This is typically addressed using end-of-day settlement data or synchronized snapshots.

In addition, different levels of market liquidity (due to different levels of bid ask spreads for example) across strikes introduces noise and heterogeneity in observed quotes. Illiquid contracts may exhibit stale or unreliable prices, which can distort the implied volatility surface even after basic filtering.

Finally, the reconstruction procedure does not explicitly impose no-arbitrage conditions or global smoothness constraints across strikes. As a result, when option prices are interpolated to form a continuous surface, the fitted call price function may exhibit local violations of convexity in strike space (e.g., small regions where butterfly spreads imply negative prices or non-monotonic curvature). Such violations are problematic because they imply the possibility of arbitrage and can lead to risk-neutral probability estimates that are not economically consistent.

Despite these limitations, the framework remains a useful reduced-form tool for extracting risk-neutral densities, provided appropriate smoothing and arbitrage constraints are imposed.

Real-life applications

Central Bank Monetary Policy Monitoring

Bahra (1997) and Kim (2009) suggest that policymakers extract ex-ante risk-neutral distributions (RNDs) from interest rate, equity, and currency options to assess market-implied expectations and uncertainty around policy decisions. Unlike futures prices, which only reflect the conditional mean, RNDs incorporate higher-order information such as skewness and kurtosis, allowing for a more complete assessment of perceived tail risks and macro-financial stress. For example, during the February 2007 equity sell-off, the European Central Bank (ECB, 2007) used option-implied probability distributions (“fan charts”) to assess whether the move reflected extreme tail risk and to track the evolution of market expectations after stabilization.

Value-at-Risk (VaR) Forecasting

Risk management units in investment banks use quantiles derived from implied RNDs to forecast extreme portfolio losses in a forward-looking manner. Compared to traditional historical simulation methods, RND-based approaches incorporate market-implied expectations and have been shown to provide improved performance relative to standard volatility-based models such as GARCH(1,1) (Chang, Chang, Huang, & Hsieh, 2011).

Systemic Risk and Stress Testing Indicator

Macroprudential regulators transform option-implied volatility surfaces into arbitrage-consistent risk-neutral distributions to quantify system-wide financial vulnerabilities. By aggregating tail-risk measures across equities, currencies, and interest rates, these distributions can be used to construct time-series indicators of systemic stress and cross-asset fragility (Malz, 2014).

Market Risk Aversion and Investor Sentiment Estimation

By combining option-implied risk-neutral distributions with empirical (physical) distributions, researchers can infer the market’s implicit risk preferences and aggregate degree of risk aversion (Bliss & Panigirtzoglou, 2004). This allows for the identification of time variation in investor sentiment and risk pricing across different investment horizons (Bliss & Panigirtzoglou, 2004; Gemmill & Saflekos, 2000).

Why should you be interested in this post?

The risk-neutral distribution is one of the few tools in finance that reveals how the market prices uncertainty based on the entire distribution of possible future states implied by option prices. It is widely used in practice to understand how the market is pricing downside risk, fat tails, and asymmetry that is directly used in volatility modelling, pricing, and risk management frameworks. From a practical perspective, it is one of the standard tools used to extract forward-looking information from option prices in both research and industry settings.

Related posts on the SimTrade blog

▶ Saral BINDAL Historical Volatility

▶ Saral BINDAL Implied Volatility and Option Prices

▶ Saral BINDAL Volatility curves: smiles and smirks

Useful resources

Academic research on option pricing

Black, F., & Scholes, M. (1973). The pricing of options and corporate liabilities. Journal of Political Economy, 81(3), 637-654.

Hull J.C. (2015) Options, Futures, and Other Derivatives, Eighth Edition, Global Edition, Chapter 14 – The Black-Scholes-Merton model, 299-320.

Merton, R.C. (1973). Theory of rational option pricing. The Bell Journal of Economics and Management Science, 4(1), 141-183.

Academic research on risk neutral distribution

Aït-Sahalia, Y., & Lo, A. W. (1998). Nonparametric estimation of state-price densities implicit in financial asset prices. The Journal of Finance, 53(2), 499-547.

Bahra, B. (1997). Implied risk-neutral probability density functions from option prices: Theory and application. Bank of England Working Paper Series, 66, 1-42.

Bates, D. S. (1991). The crash of ’87: Was it expected? The evidence from options markets. The Journal of Finance, 46(3), 1009-1044.

Bates, D. S. (1995). Testing option pricing models. NBER Working Paper Series, w5135, 1-53.

Bliss, R. R., & Panigirtzoglou, N. (2004). Option-implied risk aversion estimates. The Journal of Finance, 59(1), 407-446.

Breeden, D. T., & Litzenberger, R. H. (1978). Prices of state-contingent claims implicit in option prices. Journal of Business, 51(4), 621-651.

Chang, Y. C., Chang, C. L., Huang, H. T., & Hsieh, T. H. (2011). Value-at-Risk forecasting via option-implied risk-neutral density. Journal of Risk and Financial Management, 4(1), 56-83.

European Central Bank (ECB). (2007). Gauging stock market uncertainty using option-implied distributions. ECB Monthly Bulletin, April, Box 4, 31–32.

Figlewski, S. (2010). Estimating the implied risk neutral density for the U.S. market portfolio. In T. Bollerslev, J. R. Russell, & M. W. Watson (Eds.), Volatility and Time Series Econometrics: Essays in Honor of Robert F. Engle (pp. 43-69). Oxford University Press.

Gemmill, G., & Saflekos, A. (2000). How useful are market-implied probabilities for forecasting sharp changes in asset prices? An application to the UK general election. Market Expectations and the Implications for Monetary Policy, 203-223.

Kim, K. (2009). Monetary policy announcements and market expectations under different monetary policy regimes: An options-based approach. International Finance Discussion Papers (Federal Reserve Board), 977, 1-45.

Malz, A. M. (1996). Using option prices to estimate realignment probabilities in the European Monetary System: the case of sterling-mark. Journal of International Money and Finance, 15(5), 717-748.

Malz, A. M. (2014). A VaR-based systemic risk indicator. Federal Reserve Bank of New York Staff Reports, 668, 1-47.

Melick, W. R., & Thomas, C. P. (1997). Recovering an asset’s pdf from option prices: An application to crude oil during the Gulf crisis. Journal of Financial and Quantitative Analysis, 32(1), 91-115.

Neuhaus, H. (1995). The informational content of derivatives for monetary policy. Deutsche Bundesbank Discussion Paper Series 1: Economic Studies, 1995(03), 1-34.

Shimko, D. (1993). Bounds of probability. Risk, 6(4), 33-37.

Shreve, S. E. (2004). Stochastic calculus for finance II: Continuous-time models. Springer Science & Business Media.

About the author

The article was written in June 2026 by Saral BINDAL (Indian Institute of Technology Kharagpur, Metallurgical and Materials Engineering, 2024-2028 & Research assistant at ESSEC Business School).

▶ Discover all articles by Saral BINDAL