Why do some financial portfolios grow at an explosive rate, while others seem to stagnate? The answer often lies in a mathematical phenomenon that Albert Einstein allegedly called the “eighth wonder of the world”: compound interest.

In this article, Hadrien PUCHE (ESSEC Business School, Grande École Program, Master in Management, 2023-2027) explores the mechanics of compound interest, to help you better understand how to include this concept to your own financial strategy or investments.

About Einstein and this quote

Albert Einstein is universally recognized as the father of modern physics, famous for the theory of relativity. While his primary focus was the universe, he possessed a deep appreciation for the beauty of mathematical patterns. Although the exact origin of this specific quote is a matter of historical debate, it perfectly captures the scientific essence of wealth creation: compounding is essentially the “physics” of capital.

To Einstein, compound interest was the ultimate proof that small, consistent actions can lead to massive, universal results over time.

Analysis of the quote

The core of Einstein’s idea is that understanding compound interest is a prerequisite for investing. If you view money linearly, you see a €1,000 investment as just a fixed sum, that can earn you a couple euros every month. If you view it through the lens of compounding, you see it as a seed, with a potential to grow into a couple thousand euros over many years.

This results in the following dichotomy in terms of financial literacy:

- “He who understands it, earns it”: the investor who knows and understand compound interest reinvest his investment earnings, and create a self-sustaining loop where investments grow exponentially.

- “He who doesn’t, pays it”: the individual who does not understand compound interest starts taking high-interest liabilities, such as credit card debt, and does not realize that he his the one paying for someone else’s exponential returns, as compound interest due on the debt create a bleeding process that can quickly lead to insolvency.

However, while Einstein’s quote presents compounding as a binary choice (either you understand it or not), modern financial economics introduces a vital optimization constraint: the Life-Cycle Hypothesis.

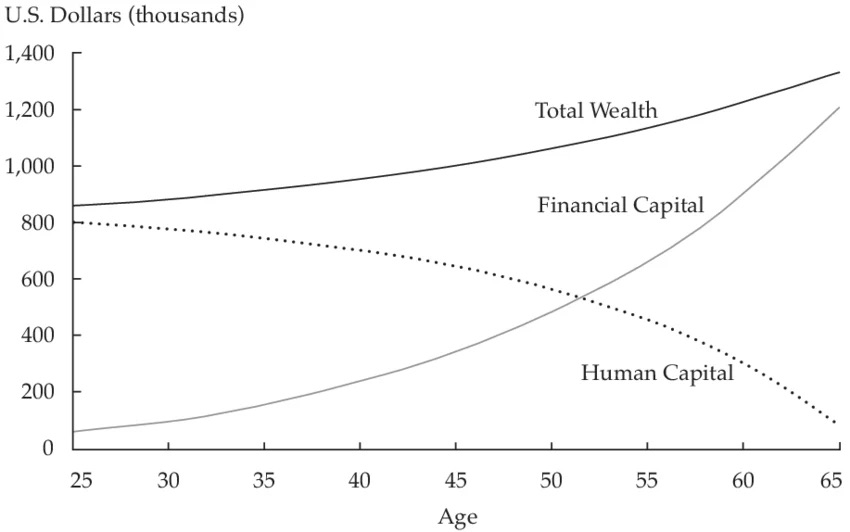

- Early in your life, you may not have a lot of financial assets, but you do have a great “human capital” (your future earning potential).

- As you age, your human capital converts into financial capital, as your future earning potential converts into actual earnings and financial capital.

As a result, you have to consider your total net worth as the sum of both types of capital :

Total wealth = human capital +financial capital

The key idea is that when you are young, you have a massive human capital that acts as a safety net, so you can afford to invest into high-risk high-reward assets, that will benedit the most from compounding. On the other hand, when you are older, following Einstein’s quote blindly would be a mistake : as you get closer to retirement, you should lower the risk of your financial capital, because you no longer have a human capital to replace it.

Samuelson (1969) and Merton (1969) proved mathematically that to maximize the compounding effect over time, an investor’s risk tolerance and portfolio composition must shift across the stages of life.

Ultimately, compound interest remains a neutral mathematical force; its structural impact on your life depends entirely on which side of the balance sheet you stand, and how dynamically you manage your assets across your life cycle.

My view on this quote

Einstein’s quote is a reminder that the greatest challenge in finance is not mathematics, but patience. We discussed the importance of patience in an article about the following quote from Warren Buffett: “The stock market is designed to transfer money from the impatient to the patient”. Read the full article here .

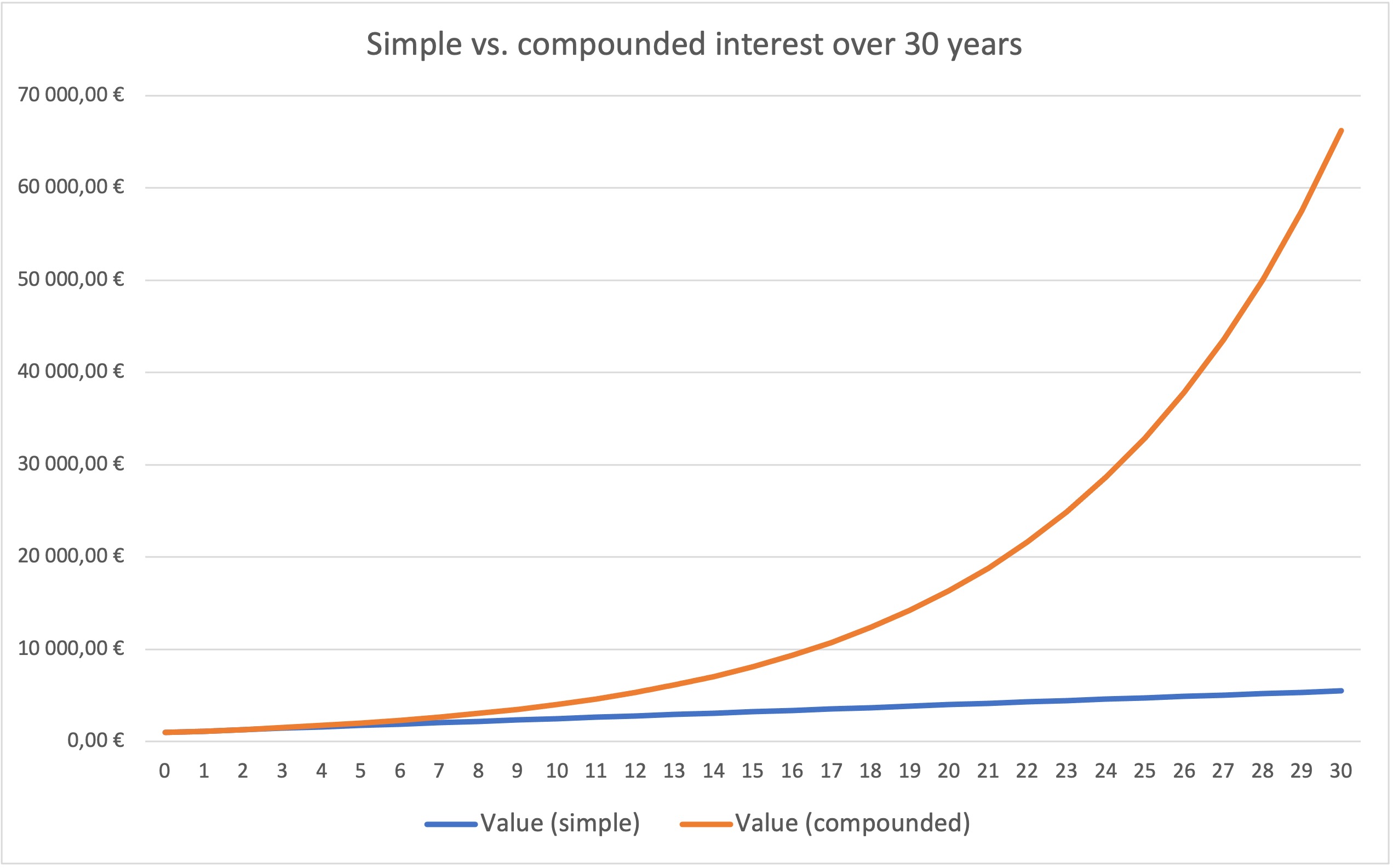

Most people fail to “earn” compound interest because they cannot endure the “boring” years, when the curve looks flat. However, if you respect the laws of physics that govern capital, you realize that you don’t need to be a genius to build wealth, you simply need to be disciplined enough to let the math do the work for you, and reach the exponential part of the curve.

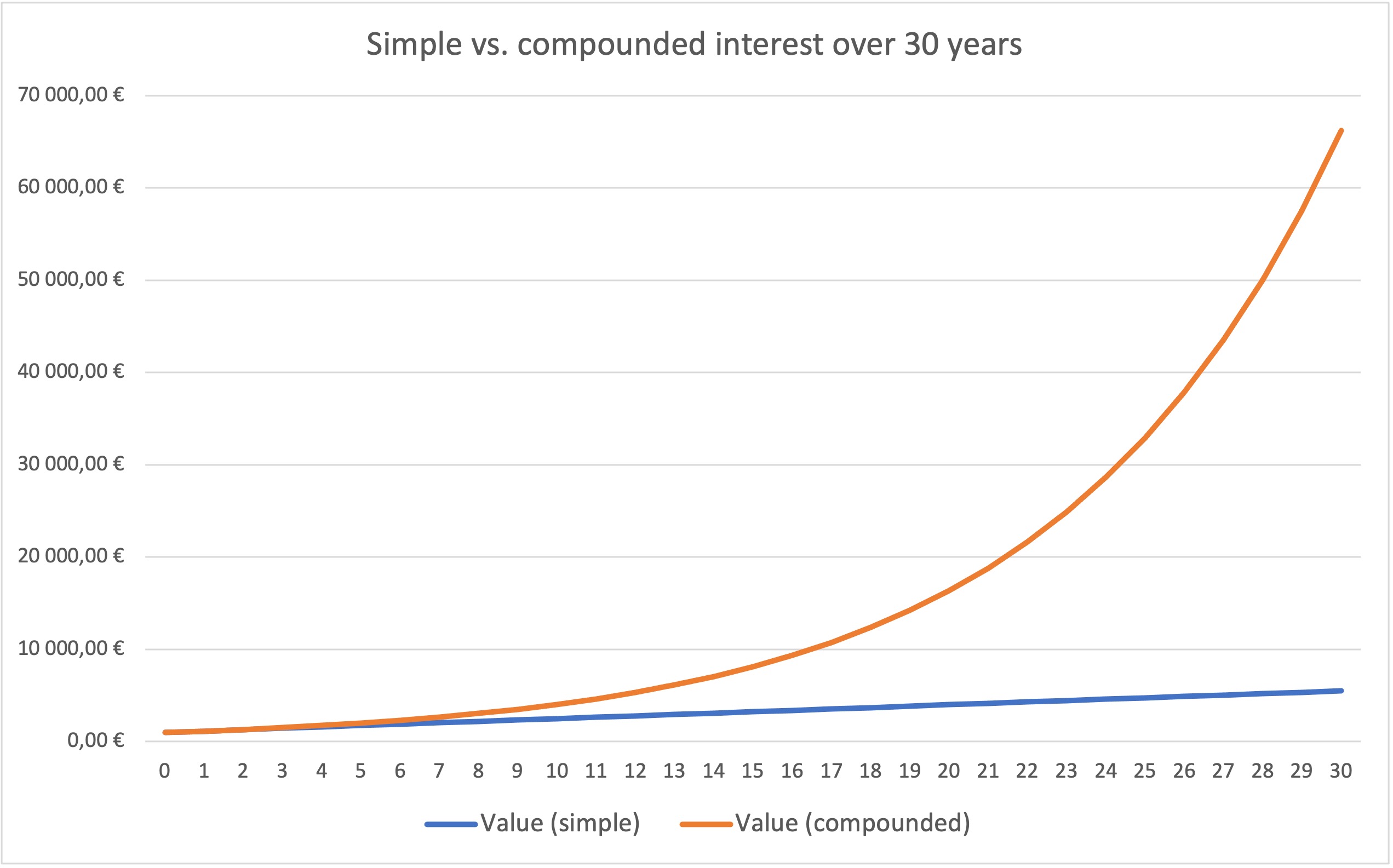

This is exactly what any compound interest curve shows : you need to wait a long time until compound interest starts making a big difference with linear one.

The math behind compound interest

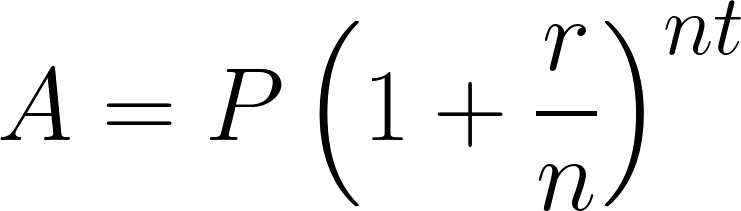

To move beyond the rhetoric, we must understand the formula that governs this “wonder.” Unlike simple interest, which is calculated only on the initial principal, compound interest is calculated on the principal plus the accumulated interest of previous periods.

The standard formula for the future value of an investment is:

Where:

- A = the future value of the investment

- P = the principal investment amount

- r = the annual interest rate (decimal)

- n = the number of times that interest is compounded per unit t

- t = the time the money is invested for

The most critical variable in this equation is t (time). Because it is an exponent, time has a disproportionate impact on the final result. This is why “time in the market” is vastly superior to “timing the market.”

The number of times interest is compounded per year, n, is also important because it reflects the speed of compounding. When interest is compounded more frequently (for example, daily rather than annually), each gain is reinvested sooner and can start generating additional returns within the same year. This accelerates the growth of the investment over time.

A technical case study about the cost of delaying your investments

We are now going to follow three different individuals, that are investing for their retirement (we do not consider public pensions). They adopt three distinct behaviors:

- The first investor is well disciplined. He invests €200 every month throughout his 40 years long career.

- The second investor wants to retire early. To do so, he invests €500 every month, but retires after only 20 years.

- The third investor forgets about retirement until he his 55 years old. He wants to catch-up, so he invests €1000 every month, trying to catch-up with the other two, but he only has 10 years left until retirement.

How much money can each of these three investors expect to have for their retirement, and much will they be able to spend every month when retired? Download this Excel file and answer all three questions to find out.

Financial Modeling Exercise: To calculate the exact future values and monthly retirement allowances for each scenario, you can download the simulation model here: Excel Simtrade Compound Interest Exercise .

Analysis of the results

These simulations should prove to you the following points:

- Spending more time in the markets is much more important than investing more: Investor C invested just as much as investor B, but because he did so in 10 years instead of 20, his final monthly pension is much lower. Similarly, despite contributing in total much less than the other two, investor A’s pension ends up being the largest one by far.

- Catching-up when you are late is almost impossible: Q3 shows that investor C would have to invest €3,576 every month for 10 years to get the same pension as investor A. In real life, this would be very difficult to achieve without a high-paying job, whereas investor A only had to put aside €200 every month…

Ultimately, this exercise proves that the “cost of delay” is not linear, but exponential. Every year of procrastination at 25 years old costs much more than a year of procrastination at 55 years old.

Related articles on the SimTrade blog

Business & Finance quotes

Quotes related to personal finance:

▶ Hadrien PUCHE Diversification is protection against ignorance – Warren Buffett

▶ Hadrien PUCHE In investing, what is comfortable is rarely profitable – Robert Arnott

▶ Hadrien PUCHE Time in the market beats timing the market – Kenneth Fisher

▶ Hadrien PUCHE Markets can remain irrational longer than you can remain solvent – Keynes

Quotes about time in finance

▶ Hadrien PUCHE Patience is bitter, but its fruit is sweet – Aristotle

▶ Hadrien PUCHE Most people overestimate what they can do in a year, and underestimate what they can do in ten – Bill Gates

Other resources

- Merton, R. (1969), “Lifetime Portfolio Selection under Uncertainty: The Continuous-Time Case,” Review of Economics and Statistics, 51(3), pp. 247–257.

- Samuelson, P. (1969), “Lifetime Portfolio Selection by Dynamic Programming,” Review of Economics and Statistics, 51(3), pp. 239–246.

About the Author

This article was written in May 2026 by Hadrien PUCHE (ESSEC Business School, Grande École Program, Master in Management, 2023-2027).

▶ Discover all articles by Hadrien PUCHE

Source : Amazon

Source : Amazon Source : Singsaver

Source : Singsaver

Source : ResearchGate

Source : ResearchGate