Is wealth a result of how much you earn, how much you spend, or how much you save? When it comes to personal finance, many assume that a higher salary is the only way to get rich. However, Robert Kiyosaki, the author of Rich Dad Poor Dad, suggests that the difference isn’t in the size of the paycheck, but in the size of the spending.

In this article, Hadrien PUCHE (ESSEC Business School, Grande École Program, Master in Management, 2023-2027) discusses Kiyosaki’s famous distinction between the “rich” and “poor” mindsets and analyzes the underlying financial mechanisms.

About Kiyosaki and this quote

Robert Kiyosaki is an American personal development author and businessman, who has become a well-known figure in financial education. He is famous for his 1997 book Rich Dad Poor Dad, which advocates financial independence through investing, real estate, and starting businesses.

Source : Amazon

Source : Amazon

This quote is deeply rooted in the first lesson of his book: “The rich don’t work for money.” Through the narrative of his “Rich Dad,” Kiyosaki explains that wealthy individuals prioritize their Asset Column, buying things that put money in their pockets, before addressing their Expense Column. By “investing first,” the rich ensure their wealth grows before lifestyle inflation takes hold.

Source : Singsaver

Source : Singsaver

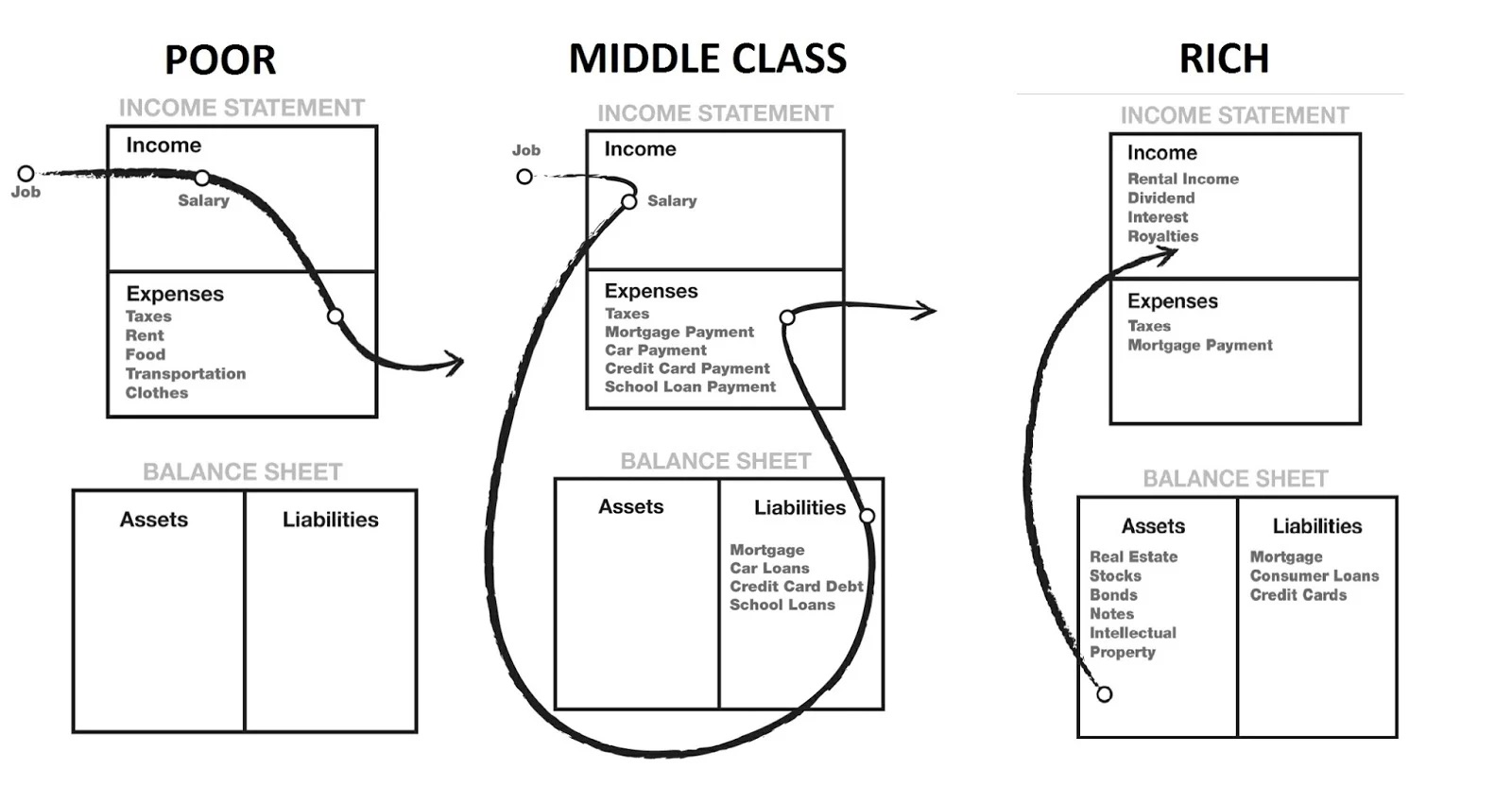

According to this framework, the distinctions are not just about the amount of money, but where it flows:

- The Poor: their primary source of income is usually a job. This income flows directly into immediate expenses such as rent, food, and transportation. They typically possess no significant assets nor liabilities (because they can’t afford to buy any).

- The Middle Class: like the poor, their primary source of income is a job. However, as their income rises, they often acquire what they perceive as assets but are actually liabilities (a house with a mortgage, a car with a loan, etc.). These liabilities create a cycle where a large portion of their income is diverted to debt payments before it even reaches their daily expenses.

- The Rich: they focus on building their assets column first. Their income is primarily generated by assets such as real estate, stocks, bonds, and intellectual property. This passive income then flows into their income statement, covering their expenses and allowing for further investment back into more assets.

This visualization highlights why the “invest first” philosophy is so critical. While the middle class is often caught in a trap of working harder to pay for increasing liabilities, the rich use their income to buy things that eventually pay for their lifestyle.

It is important to note that Kiyosaki’s philosophy was heavily influenced by his mentor, the business philosopher Jim Rohn. Rohn frequently taught: “Poor people spend their money and save what’s left. Rich people save their money and spend what’s left.” Kiyosaki essentially refined this wording to emphasize “investing” over “saving,” reflecting a more aggressive approach to capital allocation.

The key difference between saving and investing is the willingness to take risks. Saving focuses on capital preservation, risk aversion and short-term liquidity, at the cost of a low yield, whereas investing means accepting risk (and / or illiquidity) in exchange for a greater return.

Analysis of the quote

The core idea behind the quote is a fundamental distinction between two different financial behaviors:

- The ‘Rich’ behavior: invest first and then live off the rest. A rich person is someone who has reached a level of capital where they no longer have to care about the cost of daily living, so they can afford to invest the bulk of their income and spend the remaining without anxiety.

- The ‘Poor’ behavior: live first, and then eventually invest what is left. A poor person must always address immediate survival needs first, leaving investing as a secondary (and often unreachable) goal.

However, if we look at the literal reality, the quote’s view on poor people’s behavior is quite unfair to them.

- Statistics show that a significant portion of the population lives paycheck to paycheck (62% in the US according to PYMNTS, and 43% in France according to ADP), meaning they literally have nothing “left” after basic necessities. For them, the choice to “invest first” does not make sense at it is impossible for them to live properly and save.

- Personal development gurus often argue that if you “think” like the rich, you will become rich. While a disciplined mindset is helpful, this quote can be seen as “unpractical” because it ignores the structural reality of low wages and the high cost of living.

Essentially, the quote is more about financial discipline than a literal description of social classes. It defines “rich” as someone who achieves freedom by making their money work for them, rather than being a slave to their expenses. It is a valuable financial lesson, even though the term ‘Poor’ would be better replaced by ‘Middle class’.

Financial concepts linked to this quote

Kiyosaki’s philosophy is a good opportunity for us to examine three key financial concepts that are linked to this quote: assets vs. liabilities, compound interest and the time value of money, and opportunity cost.

Assets vs. Liabilities

Kiyosaki’s most famous contribution is his simplified and cash-flow-centric way to define assets and liabilities. In traditional corporate accounting, an asset is broadly defined as an economic resource owned or controlled by an entity, whereas a liability is an obligation or debt owed to an external party. Under this conventional framework, a primary residence or a personal vehicle is classified as an asset because it possesses measurable intrinsic and market value.

However, Kiyosaki challenges this traditional view by narrowing the definitions down to a single variable: the direction of net cash flow.

- An asset is strictly something that puts money in your pocket. This includes tangible and intangible holdings: rental properties, dividend-paying stocks, or a business that can run without your daily presence.

- A liability is something that takes money out of your pocket. This often includes items that people mistakenly view as “investments”, such as a car or a primary residence. While these may have market value, they require constant outflows for monthly maintenance, insurance, and taxes without generating direct income, so Kiyosaki believes you should see them as liabilities.

This distinction is crucial, because many individuals mistakenly believe they are building wealth when they are actually accumulating liabilities, that require increasing amounts of cash flow to maintain. For a sophisticated investor, the goal is to use income to acquire assets that generate even more income, creating a self-sustaining loop.

This is the “Rich” mindset Kiyosaki is all about: you should target a life where the cashflows from your assets cover the expenses from your liabilities. This way, you no longer have to work for money, as your money is the one working for you.

Another benefit of assets is that they allow investors to multiply their returns through financial leverage. By borrowing other people’s money at a fixed borrowing rate of X%, and investing it in an income-generating asset for a return of Y%, as long as Y is greater than X, the investor captures a positive spread that maximizes their return on equity (ROE). Because Kiyosaki advises prioritizing the asset column, utilizing strategic debt becomes a primary mechanism to scale an investment portfolio far faster than organic cash savings would allow.

An important note on risk: Financial leverage is fundamentally a double-edged sword. While a positive spread ($Y > X$) exponentially accelerates wealth accumulation, leverage works both ways: it severely magnifies downside risk. If the asset’s returns fall or cash flows dry up while the mandatory debt service remains fixed ($Y < X$), the investor faces heavy financial stress, margin calls, or outright insolvency.

Compound Interest and the Time Value of Money

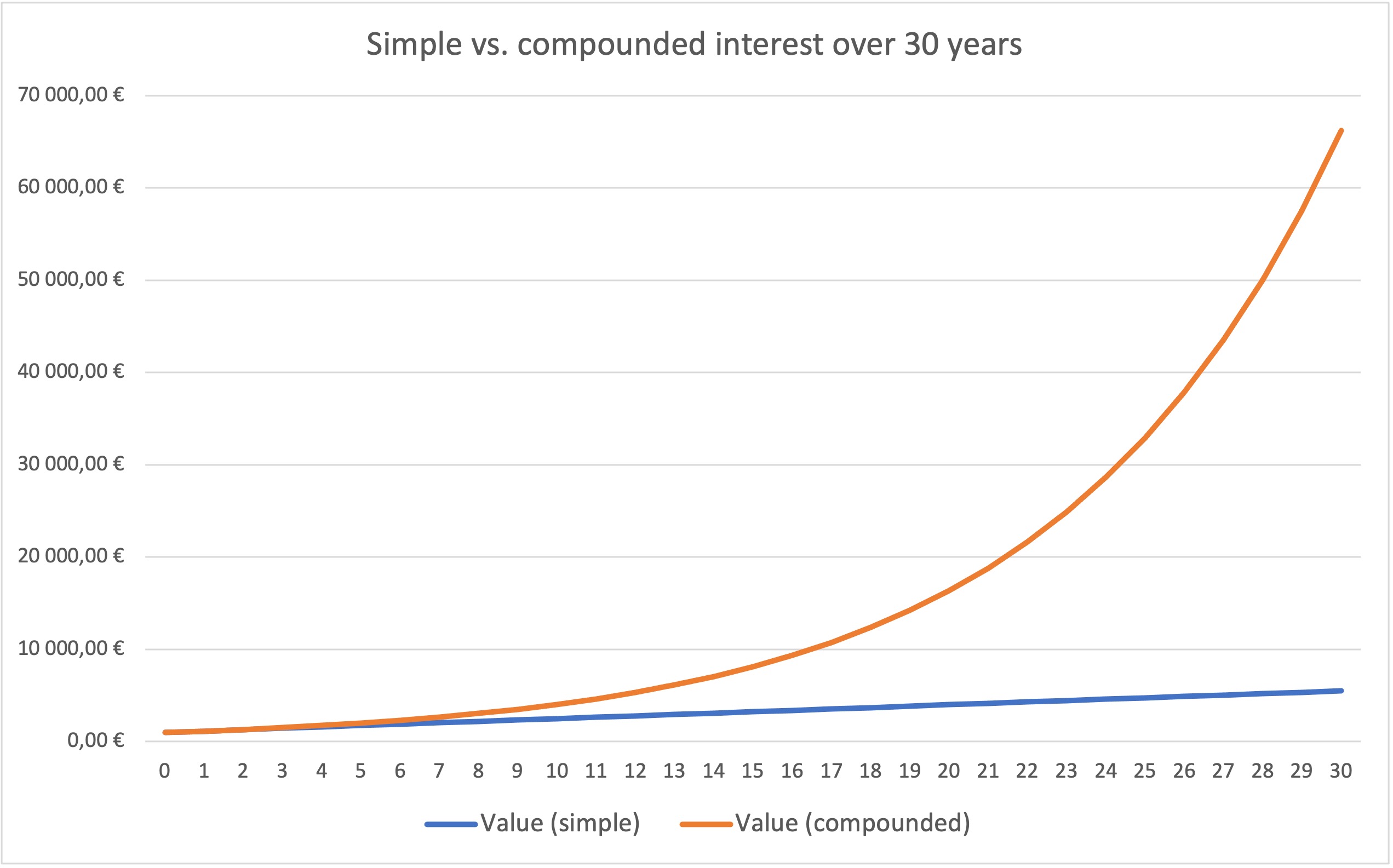

By “investing first,” an individual maximizes the time their money spends in the market. This is good because of one of the most important aspects of investing: compound interest.

Compounding interest is the process where the returns on an investment generate returns of their own the next year, creating an exponential growth curve over time.

As you can see on this graph, compound interest leads to exponential returns, whereas simple interest only leads to linear returns over time.

Compound interest works because of another key concept: the time value of money. The idea is that a dollar today is worth more than a dollar tomorrow because of its potential earning capacity (you could invest it and have more money tomorrow).

When a poor person waits to “invest what is left”, it also means missing more years of exponential growth for the capital, as the “cost” of waiting is not linear, but compounded.

Opportunity Cost

Every euro spent on a luxury item or an unnecessary expense carries an opportunity cost with it. In finance, capital is never free; every dollar tied up in a trade or a purchase is a dollar that isn’t earning a return for you. To truly calculate the price of a purchase, you must look beyond the sticker price and consider the “future value” that capital could have achieved if invested in a “risk-free” benchmark (or a diversified portfolio).

By spending first, you aren’t just losing the money today; you are losing the future wealth that money was destined to create.

As an example: If you spend €1,000 on a new phone today instead of investing it at a 7% annual return, the “real” cost of that phone over 10 years is actually ~$1,967. Over 30 years, that single €1,000 purchase represents an opportunity cost of over €7,600. This is why disciplined investors view market prices through the lens of intrinsic value rather than social status. By prioritizing spending, you are effectively selling your future financial freedom at a premium price for a temporary luxury.

The Life-Cycle framework and the rational borrowing phase theory

In Robert Kiyosaki’s popular framework, debt is viewed through a binary lens: it is either “good” (if it directly funds income-producing assets) or “bad” (if it is used for personal consumption). However, mainstream financial economics provides a more nuanced and structurally rigorous perspective through the lens of the Life-Cycle Hypothesis.

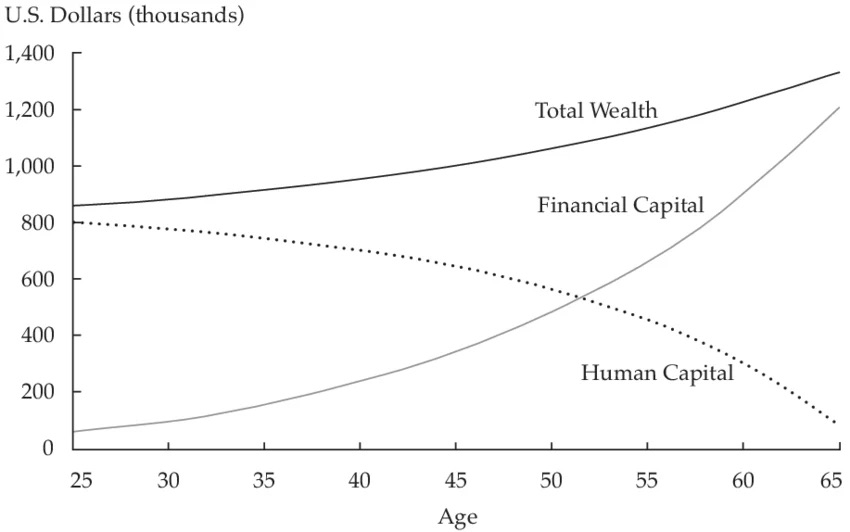

In the foundational models developed by Robert Merton and Paul Samuelson (1969), an individual’s total lifetime wealth is split into two distinct pillars:

- Financial Capital: All tangible, investable assets in the traditional accounting sense.

- Human Capital: The discounted present value of all future labor income.

What makes this framework highly compelling is how it redefines early-career balance sheets. At the start of a professional life, an individual’s financial capital is typically near zero, yet their human capital is at its absolute peak. From a corporate finance standpoint, this means young professionals are not asset-poor; rather, they possess a massive, illiquid asset that they ought to leverage through a strategic borrowing phase.

Source : ResearchGate

Source : ResearchGate

Taking on early liabilities (student debt, a first mortgage…) becomes economically rational when evaluated against the aggregate of both financial and human capital. In essence, this leverage is securely collateralized by expected future labor earnings.

Conversely, a rigid adherence to Kiyosaki’s precepts would discourage taking on debt that doesn’t immediately yield cash flow. In practice, this dogmatic view would mean avoiding early leverage entirely, disincentivizing investments in one’s own education and long-term human capital.

Why should you keep this quote in mind?

This principle serves as a vital warning against lifestyle inflation. As most people progress in their careers and earn more, they instinctively increase their spending: buying a bigger house, a faster car, or more expensive clothes.

By following the “poor” philosophy of spending first, their net worth remains stagnant regardless of their salary. Keeping this quote in mind forces you to prioritize your future self over current impulses.

My view on this quote

While the quote is mostly there to motivate people, I find it to be quite unpractical in its purest form. It presents a binary choice that does not consider the nuances of daily survival. You cannot simply “act rich” to become rich; the reality of personal finance is that you must first secure your basic needs before you can even begin to consider an investment strategy.

The practicality of this mantra heavily depends on the underlying national financial culture, like how people invest for their retirement.

- In the United States, investing in equity markets is seen as a crucial mean of wealth building, particularly when pensions are mostly built through capitalization. Because of this, it makes sense to remind individuals that they need to invest first (including for their retirement) and spend after, because if they spend everything, they won’t be able to retire.

- On the other hand, in countries like France, where most pensions are obtained through redistribution, people can afford to ‘forget’ to invest, as it won’t have devastating consequences on their retirement.

In my opinion, the wisest strategy is to target a middle ground. Rather than blindly investing every cent and hoping you have enough left for rent (a recipe for financial stress), one should start by making a rational budget. As an example, you can first take everything you really need to spend every month (rent, food, etc.) and then split the rest between leisure and savings. This way, you can manage your lifestyle within reasonable bounds.

Ultimately, simply copying the habits of the wealthy will never guarantee an entry into the 1%. However, by being careful about how you spend, you might not immediately become “rich” in the Kiyosaki sense, but you will certainly become less poor, and it will contribute to developing an analytic rigor that may be useful in other aspects of your personal or professional life.

Related articles on the Simtrade blog

▶ Hadrien PUCHE Investing is stupid if you’re more worried about short-term volatility than long-term quality – Charlie Munger

▶ Hadrien PUCHE “The four most dangerous words in investing are, it’s different this time” – Sir John Templeton

▶ Hadrien PUCHE In investing, what is comfortable is rarely profitable – Robert Arnott

▶ Hadrien PUCHE “The stock market is designed to transfer money from the impatient to the patient” – Warren Buffett

Useful resources

Kiyosaki, R. T. (1997). Rich Dad Poor Dad. Warner Books.

Rich Dad Cash Flow Patterns and Wealth.

Merton, R. (1969). Lifetime Portfolio Selection under Uncertainty: The Continuous-Time Case. The Review of Economics and Statistics, 51(3), 247–257.

Samuelson, P. (1969). Lifetime Portfolio Selection by Dynamic Stochastic Programming. The Review of Economics and Statistics, 51(3), 239–246.

About the Author

This article was written in May 2026 by Hadrien PUCHE (ESSEC Business School, Grande École Program, Master in Management, 2023-2027).

▶ Discover all articles by Hadrien PUCHE