In this article, Alexandre GANNE (ESSEC Business School, Global Bachelor in Business Administration (GBBA), 2025) shares key insights from his bachelor thesis on blockchain technology and its implications for traditional banking systems.

Introduction

This post is the result of a year-long academic research project conducted as part of my final thesis at ESSEC Business School. It explores how the growing adoption of blockchain technology is redefining core principles of traditional financial systems and the strategic implications this transformation holds for banking institutions.

The disruptive nature of blockchain

Blockchain is often described as the cornerstone of the next technological revolution in finance. It allows for the decentralization of data storage and value exchange, eliminating the need for central authorities to validate transactions. With distributed consensus mechanisms and cryptographic security, blockchain systems can operate autonomously and transparently. These features make it not just a new tool, but a foundational shift that could reshape core banking functions such as recordkeeping, interbank transfers, and credit issuance. Its key characteristics, immutability, programmability, disintermediation, and transparency, pose significant challenges to the centralized model of traditional finance.

From intermediation to decentralization

One of blockchain’s most radical promises is disintermediation. Traditional financial systems are heavily reliant on intermediaries such as banks, brokers, and clearinghouses to establish trust and validate transactions. Blockchain introduces the ability to execute trustless peer-to-peer exchanges using cryptographic proofs and decentralized ledgers. For example, platforms like Ethereum enable the deployment of smart contracts, self-executing programs that automatically enforce the terms of a contract without human intervention, drastically reducing friction and cost.

Security and auditability

Unlike traditional databases that are vulnerable to manipulation or single points of failure, blockchain offers a tamper-proof and chronologically auditable data structure. This makes it a valuable tool for regulatory compliance and fraud prevention.

Implications for the banking sector

Custody and settlement

Traditional banks act as intermediaries for the settlement of securities and custody of assets. Blockchain-based tokenization could eliminate the need for such intermediaries by allowing real-time settlement and direct ownership recording on-chain.

Compliance

Know Your Customer (KYC) and Anti-Money Laundering (AML) procedures are critical, yet often duplicative and costly for financial institutions. Blockchain can streamline these processes by allowing users to maintain a single, verified digital identity that can be securely shared across multiple entities. Through permissioned blockchain networks, institutions can access and update identity records in real time, increasing efficiency while maintaining regulatory compliance. Additionally, immutable audit trails enhance traceability and accountability.

New business models

The rise of decentralized finance (DeFi) introduces new paradigms in financial services, automated lending, yield farming, insurance, and derivatives, all operating without traditional intermediaries. In response, incumbent banks are exploring strategic partnerships, investments in blockchain startups, and internal initiatives to tokenize assets or build proprietary custodial solutions. Hybrid models, blending regulated infrastructure with decentralized services, are likely to emerge as a dominant trend over the next decade.

Why should I be interested in this post?

For any ESSEC student or finance professional interested in the frontier of financial innovation, this article distills the key findings of a year-long academic thesis dedicated to understanding how blockchain is transforming our industry. It bridges theory and practice, highlighting both opportunities and risks. As regulators, institutions, and entrepreneurs continue to shape the future of financial systems, understanding blockchain is no longer optional, it is essential to navigate and lead in tomorrow’s economy.

In this article, Alexandre GANNE (ESSEC Business School, Global Bachelor in Business Administration (GBBA), 2025) shares his professional experience as Finance Assistant Manager at Kpler.

About the company

Kpler is a fast-growing technology and data intelligence company offering transparency solutions in commodity markets. Its platforms collect and analyze data from hundreds of sources: including radar, satellites, shipping databases, and government publications, to provide real-time insights into global supply and demand dynamics. Kpler’s clients include energy giants, trading houses, public utilities, and financial institutions such as hedge funds and banks.

Logo of Kpler.

Source: the company.

Headquartered in Paris, Kpler has a strong international presence with offices in London, Singapore, Dubai, Houston, and New York. Its diverse team and innovative culture have made it one of the key disruptors in the financial and energy data sectors.

My internship

My missions

During my internship, I worked within the Finance Department as a Finance Assistant Manager, contributing to Kpler’s accounts receivable processes. As my first business school internship, which I completed at just 19 years old over a period of three months, this role gave me early exposure to the financial operations of a rapidly scaling tech firm. My responsibilities included issuing and monitoring invoices across multiple international entities (France, UK, UAE, US, Singapore), tracking and securing timely customer payments, and managing unresolved payment situations in coordination with sales and operations teams. I was also in charge of analyzing client payment performance metrics (e.g. Days Sales Outstanding), supporting forecasting tasks, and escalating at-risk accounts to senior management.

Required skills and knowledge

The internship required strong organizational and analytical skills, with an understanding of accounting principles and international tax practices. Proficiency in Microsoft Excel and familiarity with ERP or invoicing software were essential for data manipulation and reporting. Additionally, this position demanded a high level of professional communication, especially in client interactions regarding payment reminders, dispute resolution, and follow-ups, often involving senior finance stakeholders.

What I learned

This experience gave me a detailed view of how financial flows are managed in a fast-paced, multinational tech company. I enhanced my technical skills in accounts receivable management, financial forecasting, and reporting. The daily collaboration with sales and legal teams further reinforced my ability to work across departments and navigate complex operational settings in English and French. I also learned to use software tools such as NetSuite and Salesforce.com. Beyond technical knowledge, I discovered what it means to work in a 21st-century startup environment, which contrasts significantly with traditional corporate structures. I learned to manage my own working hours, adapt to flexible geographies, including remote work setups, although I preferred being on-site in the Paris office to engage directly with the talented Kpler teams. Finally, I developed the ability to communicate effectively with people from diverse professional backgrounds, including engineers, developers, and sales specialists.

Financial concepts related to my internship

I present below three financial concepts related to my internship: Days Sales Outstanding (DSO), Cash Flow Forecasting, and Credit Risk Assessment.

Days Sales Outstanding (DSO)

DSO measures the average number of days it takes for a company to collect payment after a sale. At Kpler, I regularly tracked this KPI across entities to identify underperforming accounts. A high DSO can indicate liquidity issues and may require proactive engagement strategies. My tasks involved identifying trends in DSO, generating dashboards to report them, and communicating with internal teams to initiate corrective actions with clients.

Cash Flow Forecasting

Cash flow forecasting involves projecting future cash inflows and outflows to ensure the company can meet its financial obligations. As part of the finance team, I supported the preparation of weekly and monthly forecasts based on outstanding invoices, historical payment behavior, and contractual terms. Accurate forecasting is crucial for maintaining solvency and planning investments in high-growth companies like Kpler.

Credit Risk Assessment

Credit risk assessment evaluates the likelihood that a customer will default on their payment obligations. At Kpler, I participated in risk reviews using payment histories and financial data to inform internal decisions regarding client credit terms. For high-risk clients, I contributed to drafting escalation reports and supported the implementation of preemptive actions such as revised payment terms or partial upfront invoicing.

Why should I be interested in this post?

This post is particularly relevant for students interested in finance within innovative environments. It provides exposure to international operations, cross-functional collaboration, and practical financial risk management. Working at Kpler allows you to evolve in a data-driven culture that sits at the intersection of finance, technology, and energy markets. It is also a unique opportunity to contribute meaningfully to strategic processes in a fast-scaling tech firm.

In this article, Alexandre GANNE (ESSEC Business School, Global Bachelor in Business Administration (GBBA), 2025) shares his professional experience as Depositary Control Auditor at CACEIS Bank.

About the company

CACEIS Bank is a leading European financial institution specializing in asset servicing. A subsidiary of Crédit Agricole and Santander, CACEIS provides custody, depositary, and fund administration services to institutional clients, management companies, and large corporates. The group supervises more than €2.3 trillion in assets under custody and over €3 trillion in assets under administration.

Logo of CACEIS Bank

Source: the company.

The Depositary Control team plays a critical role in investor protection, ensuring that asset managers operate in compliance with applicable regulations. It verifies the correct valuation of assets, control of financial ratios, and the conformity of transactions made on behalf of the funds.

My internship

My missions

As a Depositary Control Auditor, my primary responsibility was to conduct thematic audits on European investment management companies with assets exceeding €5 billion. I focused on key control areas such as asset valuation, regulatory ratios, and Value at Risk (VaR). I also carried out analytical reports on current macroeconomic trends to assess their potential impact on asset management practices. Additionally, I worked on recurring and ad hoc studies, such as evaluating the impact of the ongoing real estate crisis on real estate investment funds (REITs, OPCIs, SCPI), analyzing their asset exposure, liquidity constraints, and valuation resilience.

Required skills and knowledge

This role required a solid understanding of financial regulations and investment vehicles, as well as proficiency in the Microsoft Office suite, especially Excel for financial modeling and reporting. Soft skills such as rigor, autonomy, and teamwork were crucial to ensure the reliability of our audit reports and smooth communication with asset managers. A high level of professionalism in client communication was essential, particularly when addressing sensitive compliance issues with senior representatives of management companies.

What I learned

This apprenticeship allowed me to develop a comprehensive understanding of the regulatory ecosystem of European asset management. I acquired expertise in risk control, asset valuation methodologies, and fund auditing practices. I also improved my organizational skills, learning to manage several audit missions simultaneously while respecting strict deadlines and reporting requirements.

Financial concepts related to my internship

I present below three financial concepts related to my internship: asset valuation, Value at Risk (VaR), and key regulatory ratios.

Asset Valuation

Asset valuation is the process of determining the fair market value of assets held in an investment portfolio. This is a critical step in calculating the Net Asset Value (NAV) of a fund. In practice, I reviewed how management companies priced listed assets (using mark-to-market techniques) and unlisted assets (using models like discounted cash flows or multiples comparison). I ensured that valuation methods adhered to regulatory guidelines and were consistently applied, especially for complex or illiquid assets.

Value at Risk (VaR)

Value at Risk (VaR) quantifies the potential maximum loss of a portfolio under normal market conditions over a specific time period and confidence level (e.g., 99% over 10 days). I assessed the robustness of VaR models used by asset managers, ensuring they incorporated appropriate volatility measures, stress scenarios, and backtesting. VaR helped us monitor whether funds stayed within authorized market risk limits and provided a quantitative basis for risk-based oversight.

Regulatory Ratios

Regulatory ratios include leverage, liquidity, and concentration limits imposed by the AIFM and UCITS directives. During audits, I verified that asset managers respected these ratios daily and that breaches were properly justified and resolved. This involved reviewing internal control mechanisms and examining historical data to detect anomalies or patterns of non-compliance, thereby reinforcing the protection of investor interests.

Why should I be interested in this post?

This internship is particularly valuable for students interested in financial regulation, risk oversight, or asset management. Beyond that, it is a gateway to multiple career paths in finance. I am honored to be the fifth ESSEC student to hold this position at CACEIS Bank. Many of my predecessors went on to successful careers in investment banking, private equity, or consulting, demonstrating that this experience builds a strong foundation even beyond the field of risk management. Being part of this legacy pushes me to give my best and uphold the high standards set by those who came before me.

In this article, Mathias DUMONT (ESSEC Business School, Global Bachelor in Business Administration (GBBA), 2022-2026) explains how weather risk impacts the pricing of agricultural derivatives like futures and options, and how climate-based data can be integrated into stochastic pricing models. Combining academic insights and practical examples, including a mini-case from the SimTrade Blé de France simulation, the article illustrates adjustments to models such as the Black-Scholes-Merton model for temperature and rainfall variables in valuing agricultural contracts.

Introduction

Extreme weather has always been a critical factor in agriculture, but climate change is amplifying the frequency and severity of these events. From prolonged droughts to unseasonal floods, weather shocks can send crop yields and commodity prices on wild rides. This rising uncertainty has given birth to weather derivatives – financial instruments designed to hedge weather-related risks – and has made volatility forecasting a key challenge in pricing agricultural contracts. In fact, as businesses grapple with climate volatility, trading volume in weather derivatives has surged. CME Group saw a 260% increase last year (CME Group, 2023). The question for traders and risk managers is: how do we quantitatively factor weather risk into the pricing of futures and options on crops like wheat and corn?

Weather Risk and Agricultural Markets

Weather directly affects crop supply. A bumper harvest following ideal weather can flood the market and depress prices, whereas a drought or frost can decimate yields and trigger price spikes. These supply swings translate into volatility for agricultural commodity markets. For example, during the U.S. drought of 2012, corn prices skyrocketed, and the implied volatility of corn futures jumped by over 14 percentage points within a month, reaching ~49% in mid-July. Such surges reflect the market rapidly repricing risk as participants absorb new climate information (in this case, worsening crop prospects). Seasonal patterns are also evident: harvest seasons tend to coincide with higher price volatility because that’s when weather uncertainty is at its peak. Studies show that harvesting cycles create predictable seasonal volatility patterns in crop markets – when a critical growth period is underway, any shift in rainfall or temperature forecasts can send prices swinging.

Beyond affecting supply quantity, weather can influence crop quality (e.g., excessive rain can spoil grain quality) and even logistic costs (flooded transport routes, etc.), further feeding into prices. The interconnected global nature of agriculture means a drought in one region can reverberate worldwide. As noted in the SimTrade Blé de France case, weather conditions in France influence the quantity and quality of wheat the company harvests, while weather conditions around the world influence the international wheat price. In the Blé de France simulation (which models a French wheat producer’s stock), participants see how news of floods or droughts translate into stock price moves. For instance, the company might project a 7-million-ton wheat harvest, but analysts’ forecasts range from 6.5 to 7.2 Mt – with the realized level highly weather-dependent in the final weeks of the season. A poor weather turn not only shrinks the crop but boosts global wheat prices, creating a complex revenue impact on the firm. This mini-case underlines that weather risk entails both volume uncertainty and price uncertainty, a double-whammy for agricultural firms and their investors.

Case Study: Weather Shocks in Wheat Markets

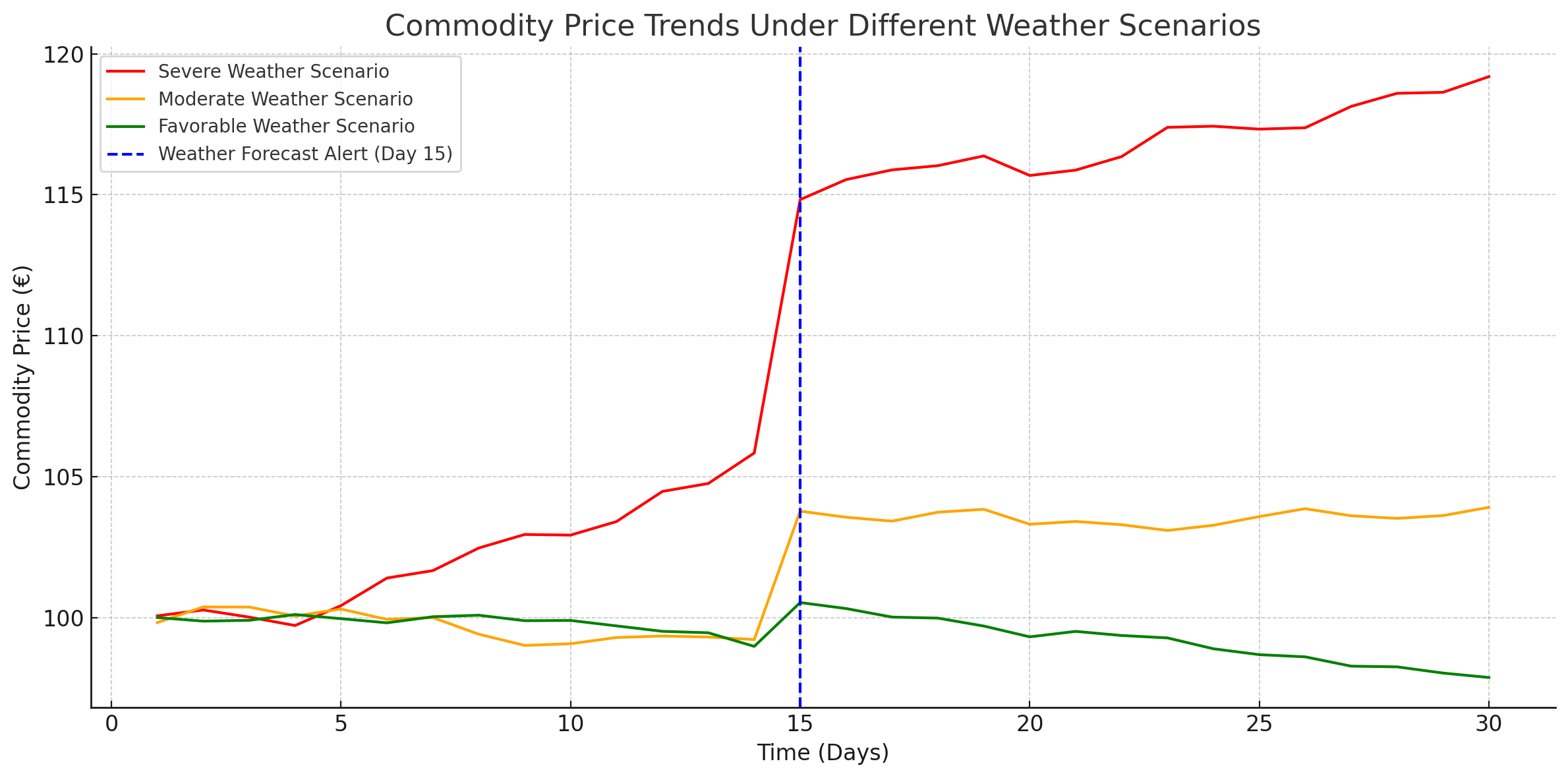

To illustrate the impact of weather risk on commodity pricing, consider three simulated scenarios for an upcoming wheat growing season: (1) **Favorable weather**, (2) **Moderate conditions**, and (3) **Severe weather** such as drought. Each scenario generates a distinct price trajectory in the wheat market. Under favorable weather, prices tend to remain stable or decline slightly, particularly at harvest, due to strong yields and potential oversupply. In moderate conditions, prices may rise modestly as the market adjusts to balanced supply and demand. In contrast, severe weather triggers early price rallies as concerns about yield shortfalls emerge, followed by sharp spikes once crop damage becomes evident. For producers and traders, anticipating these divergent price paths is essential for pricing contracts, managing risk exposure, and structuring hedging strategies effectively.

Figure 1. Simulated commodity price paths under three weather scenarios.

Source: Author’s simulation.

Figure 1. shows the simulation of commodity price paths under three weather scenarios: severe weather (red), moderate weather (orange), and favorable weather (green). A mid-season weather forecast alert (Day 15) triggers a shift in market expectations, causing price divergence. This simulation illustrates how weather shocks and forecasts impact commodity pricing through volatility and revised yield expectations.

From a risk management perspective, tools exist to handle these contingencies. Farmers or firms concerned about catastrophic weather can turn to weather derivatives for protection. Weather derivatives are financial contracts (often based on indexes like temperature or rainfall levels) that pay out based on specific weather outcomes, allowing businesses to offset losses caused by adverse conditions. They have been used by a wide range of players – from utilities hedging warm winters, to breweries hedging late frosts. These instruments can be customized over-the-counter or traded on exchanges. Notably, CME Group lists standardized weather futures and options tied to indices such as heating degree days (HDD) and cooling degree days (CDD) for various cities. The existence of such contracts means that even when commodity producers cannot fully insure their crop yield, they might hedge certain aspects of weather risk (like an unusually hot summer) via financial markets. In our context, a wheat farmer worried about drought could, say, buy a weather option that pays off if rainfall falls below a threshold, providing funds when their crop output (and thus futures position) suffers.

Climate-Based Volatility in Derivatives Pricing

How can weather uncertainty be incorporated into derivative pricing models? Classic option pricing, such as the Black-Scholes-Merton model, assumes a fixed volatility for the underlying asset’s returns. For agricultural commodities, that volatility is anything but constant – it ebbs and flows with the weather and seasonal progress. Practitioners thus often use stochastic volatility models or at least adjust the volatility input over time. For example, one might use higher volatility estimates during the crop’s growing season and lower volatility post-harvest when output is known. This practice parallels how equity traders anticipate higher volatility in stock prices ahead of major earnings or profit announcements, and lower volatility after the announcement of profits by the firm.

Like companies facing performance surprises, weather shocks inject information asymmetry into the market, which must be priced into the option premiums. This aligns with the observed Samuelson effect, where futures contracts on commodities tend to have higher volatility when they are near maturity (coinciding with harvest uncertainty).

Market prices of options themselves reflect these expectations. When a looming weather event is expected to cause turmoil, options premiums will rise. The metric capturing this is implied volatility – the volatility level implied by current option prices. Implied vol is essentially forward-looking and will jump if traders foresee choppy waters ahead. Empirical evidence shows that extreme weather forecasts translate into higher implied vols for crop options. In 2012, as drought fears intensified, corn option implied volatility spiked (alongside futures prices). Conversely, once a forecasted drought started being relieved by rains, implied volatility eased off, signaling that some uncertainty had been resolved. A recent study also found that integrating meteorological data (like rainfall and temperature anomalies) into volatility modeling significantly improves the ability to hedge risk in agricultural markets. In other words, the more information we feed into our models about the climate, the more accurately we can price and hedge these derivatives.

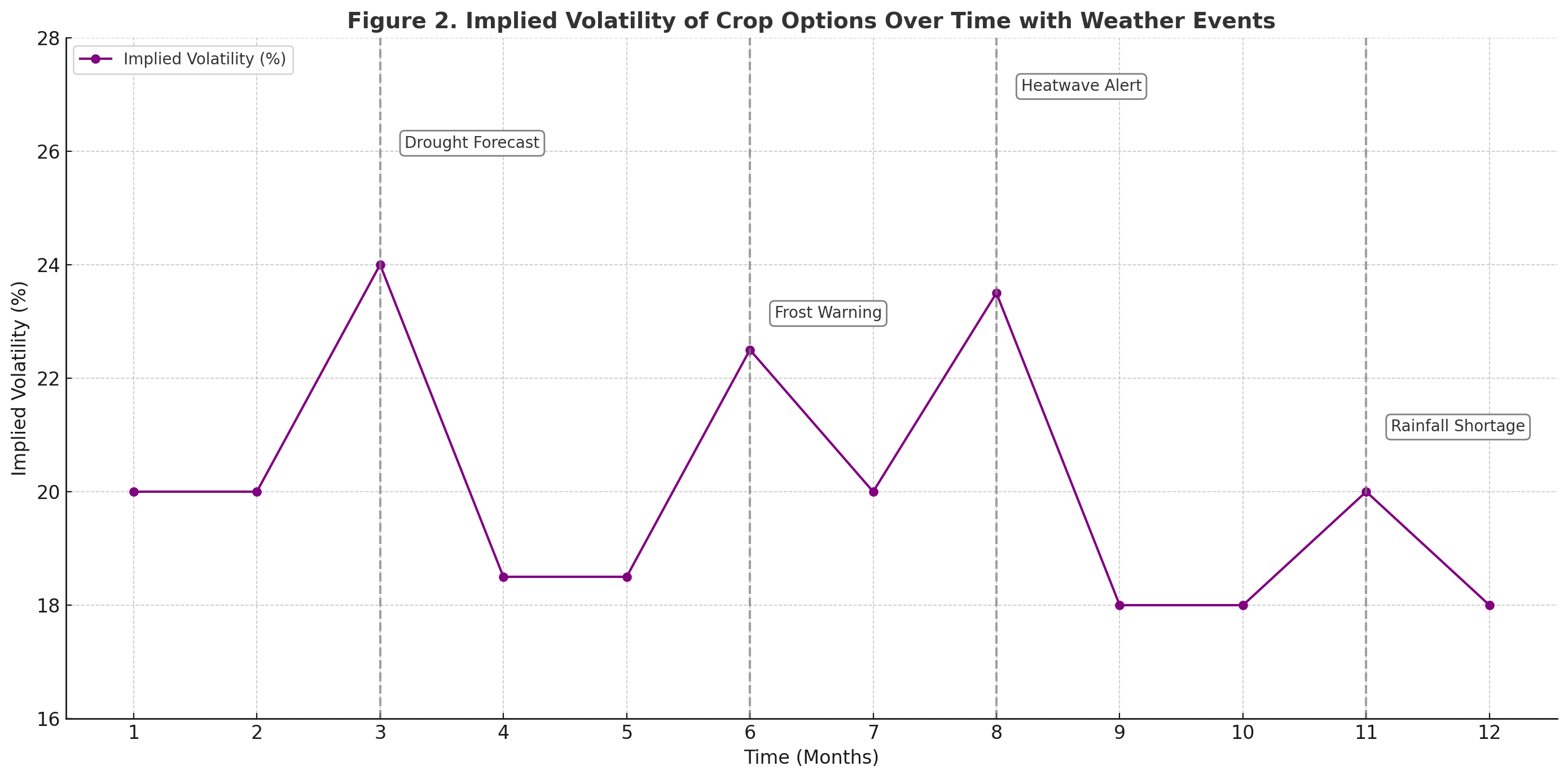

Figure 2. Implied Volatility of Crop Options Over Time with Weather Events

Source: Author’s simulation.

This simulation illustrates the evolution of implied volatility over a 12-month crop cycle. Forecasted climate events—drought (Month 3), frost (Month 6), heatwave (Month 8), and rainfall shortage (Month 11)—lead to moderate but distinct volatility spikes. As uncertainty resolves, volatility returns to baseline.

One practical approach to pricing under climate uncertainty is to use scenario-based or simulation-based models. Instead of assuming a single volatility number, an analyst can simulate thousands of possible weather outcomes (perhaps using historical climate data or meteorological forecast models) and the corresponding price paths for the commodity. Each simulated price path yields a payoff for the derivative (e.g. an option’s payoff at expiration), and by averaging those payoffs (and discounting appropriately), one can derive a weather-adjusted theoretical price. This Monte Carlo style approach effectively treats weather as an external random factor influencing the commodity’s drift and volatility. It’s particularly useful for complex derivatives or when the payoff depends explicitly on weather indices (such as a derivative that pays out if rainfall is below X mm).

When the derivative’s underlying is the commodity itself (e.g. a corn futures option), traditional risk-neutral pricing arguments still apply, but the challenge is forecasting volatility. Traders often adjust the volatility smile/skew on agricultural options to account for asymmetric weather risks – for instance, if a drought can cause a much bigger upside move than a rainy season can cause a downside move, call options might embed a higher implied volatility (reflecting that upside risk of price spikes). This is observed in practice as well; extreme weather events can distort the implied volatility “skew” of crop options, as out-of-the-money calls become more sought after as disaster insurance.

In contrast, if the derivative’s underlying is a pure weather index (say an option on cumulative rainfall), then pricing becomes more complex because the underlying (rainfall) is not a tradable asset. In such cases, the Black-Scholes-Merton formula is not directly applicable. Instead, pricing relies on actuarial or risk-neutral methodologies that incorporate a market price of risk for weather. For example, one method is to estimate the probability distribution of the weather index from historical data, then add a risk premium to account for investors’ risk aversion to weather variability, and discount expected payoffs accordingly. Another method uses “burn analysis” – taking historical weather outcomes and the associated financial losses/gains had the derivative been in place, to gauge a fair premium. Academic research has proposed models ranging from modified Black-Scholes-Merton-type formulas for rainfall (with adjustments for the non-tradability) to advanced statistical models (e.g. Ornstein-Uhlenbeck processes with seasonality for temperature indices. The key takeaway is that whether it’s directly in commodity options or in dedicated weather derivatives, climate factors force us to go beyond textbook models and embrace more dynamic, data-driven pricing techniques.

Why should I be interested in this post?

For an ESSEC student or a young finance professional, this topic sits at the intersection of finance and real-world impact. Understanding weather risk in markets is not just about farming – it’s about how big data and climate science are increasingly intertwined with financial strategy. Agricultural commodities remain a cornerstone of the global economy, and volatility in these markets can affect food prices, inflation, and even economic stability in various countries. By grasping how to value derivatives with climate-based volatility inputs, you are gaining insight into a growing niche of finance that deals with sustainability and risk management. Moreover, the skills involved – scenario analysis, simulation modeling, blending of economic and scientific data – are highly transferable to other domains (think energy markets or any sector where uncertainty reigns). In a world facing climate change, expertise in weather-related financial products could open career opportunities in commodity trading desks, insurance/reinsurance firms, or specialized hedge funds. Ultimately, this post encourages you to think creatively and interdisciplinarily: the best hedging or valuation solutions may come from combining financial theory with environmental intelligence.

In this article, Olivia BRÜN (ESSEC Business School, Global Bachelor in Business Administration (BGBA), and ESIC Business School, Bachelor of Business Administration and Management (BBAM), 2022–2026) analyses the concept of break-even analysis, a widely used financial technique employed to determine business profitability. This article illustrates the method in a case study of Watches of Switzerland Group, a publicly listed upscale watch retailer with its headquarters in the United Kingdom.

Introduction and Context

Break-even analysis is a critical component of managerial decision-making and financial planning. It allows companies to determine the level (volume) of sales that will cover all costs, both variable and fixed, before the company can be profitable. The break-even point is a crucial milestone in the operations of a firm. Sales below the break-even point create losses, while sales above it enable every extra unit sold to contribute to overall profitability.

This method is widely used in various industries to evaluate new projects, determine pricing strategies, and examine the financial feasibility of corporate decisions. Especially in capital-intensive industries or businesses focused on product offerings, understanding the break-even point is key to sound financial management and setting realistic sales targets.

History of the Concept

Break-even analysis stems from cost-volume-profit (CVP) analysis. Originating in managerial accounting in the early 20th century, CVP distinguishes between fixed costs (independent of production volume) and variable costs (dependent on production volume). By comparing these costs to projected revenues, decision-makers can identify the break-even point.

Case Study: Watches of Switzerland Group

This case study applies the break-even method to Watches of Switzerland Group PLC, a retailer of high-end watches. The following figures are taken from the company’s 2022 Annual Report:

Using these values, we compute the variable cost per unit and contribution margin per unit as follows:

Variable cost per unit: £3,132 (= £966.5 million / 308,560)

Contribution margin per unit: £1,868 (= £5,000 – £3,132 )

Break-even point (units): 220,128 units (= Fixed Costs / Contribution Margin per Unit = £411.2 million / £1,868).

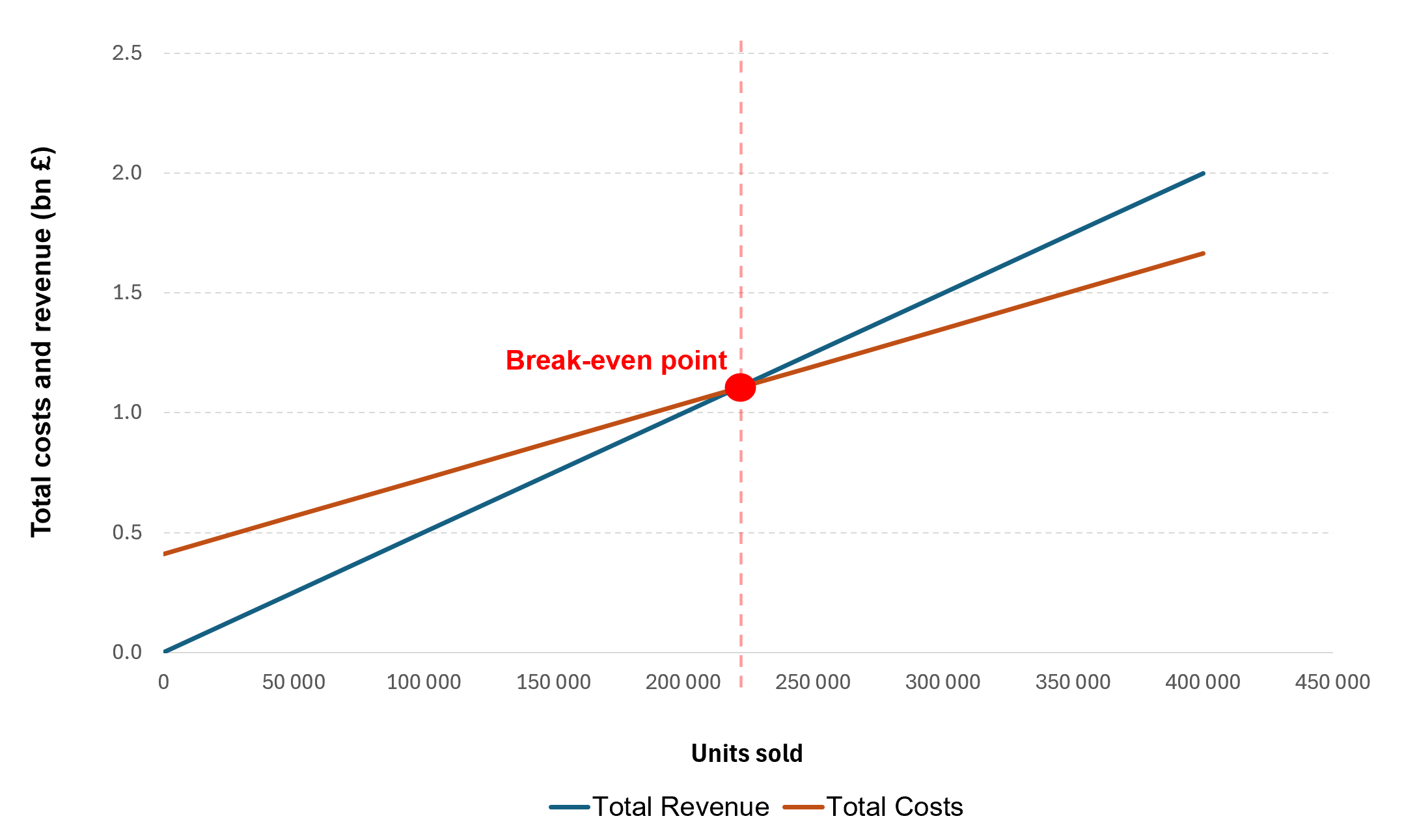

At the break-even point, total revenues and total costs are approximately £1.1 billion. Sales above this point generate operating profit.

Break-even Chart from Excel

The chart below illustrates the relationship between total revenue and total cost across different sales volumes. The break-even point is located where the two lines intersect, at approximately 220,128 units, equivalent to around £1.1 billion in revenue. This marks the threshold at which the company covers all fixed and variable costs, resulting in neither profit nor loss.

The underlying Excel model (see “READ ME” tab for detailed explanations) allows for interactive analysis. Users can adjust inputs such as fixed costs, average selling price, and variable cost per unit. The break-even point updates automatically, making the tool highly practical for scenario analysis and financial planning. This kind of sensitivity analysis is essential in real world decision making, especially in industries with high fixed costs like luxury retail.

Break-even Analysis for Watches of Switzerland Group

Source: Excel computation based on data from Watches of Switzerland Group

You may download the Excel file used to do the computations and produce the chart above.

Why should I be interested in this post?

Break-even analysis is fundamental in both theoretical and applied finance. It is widely used in consultancy, financial planning, and entrepreneurship. Understanding this concept allows business professionals to assess cost structures, pricing strategies, and financial viability of new projects.

For an ESSEC student pursuing business or finance, mastering break-even analysis equips you to analyze operational leverage and forecast how profits change with varying sales levels. This insight helps in making informed strategic decisions, managing risk, and ensuring sustainable business growth.

Useful resources

Academic resources

Horngren, C. T., Datar, S. M., & Rajan, M. V. (2015) Cost Accounting: A Managerial Emphasis (15th ed.). Pearson Education. – This foundational textbook offers detailed explanations of break-even analysis, cost behavior, and their relevance in managerial decision-making.

Atrill, P., McLaney, E. (2022) Management Accounting for Decision Makers (10th ed.). Pearson. – This book focuses on applying break-even and contribution analysis in real business contexts, helping students and professionals make informed financial decisions.

The article was written in May 2025 by Olivia BRÜN (ESSEC Business School, Global Bachelor in Business Administration (BGBA), and ESIC Business School, Bachelor of Business Administration and Management (BBAM), 2022–2026), 2022–2026).

In this article, Adelaide RIDER-NICHOLSON (ESSEC Business School, Global Bachelor in Business Administration (GBBA) – Exchange Student, 2025) shares their internship experience with the Government of Canada at the Ministry of Citizenship and Multiculturalism. They explore the structure of the Ministry, its mandate, and their involvement in policy research and community engagement projects.

About the Ministry of Citizenship and Multiculturalism

The Ministry of Citizenship and Multiculturalism is a part of the Government of Canada and is responsible for advancing inclusive policies, promoting multicultural values, and ensuring that newcomers and minority communities are supported through public services and community initiatives. The Ministry plays a critical role in shaping Canada’s multicultural identity and ensuring equitable access to opportunities across all communities.

Logo of Government of Ontario.

Source: the Government of Ontario.

As a public institution, the Ministry’s focus is not profit-driven but centered on social impact, public service, and civic responsibility. Its work ranges from supporting newcomer integration, funding ethnocultural community organizations, and developing anti-racism strategies to promoting civic engagement and Canadian values of pluralism and diversity.

The Working Process

Like many public service departments, the Ministry follows a structured approach to designing and implementing programs. This process often involves:

Step 1: Policy Mandate & Strategic Planning

All projects begin with a mandate from the provincial or federal government. These directives outline focus areas — such as improving access to services for racialized communities or enhancing civic education among youth. Strategic planning follows, during which interdepartmental teams define objectives, allocate resources, and consult stakeholders.

Step 2: Research and Community Engagement

To ensure that initiatives reflect lived experiences, the Ministry often conducts stakeholder engagement, community consultations, and data analysis. As an intern, I was involved in this step—compiling demographic reports, preparing surveys, and participating in virtual town halls with community leaders and non-governmental organizations (NGOs).

Step 3: Policy Development and Program Delivery

Once the research and feedback are analyzed, policy advisors draft policy proposals or refine programs. These may include funding frameworks, anti-racism toolkits, or educational materials. Interns assist by reviewing comparative policy models, drafting briefing notes, or supporting communications plans for public outreach.

Each level of the organization plays a specific role—from data collection and research at the analyst level to shaping the long-term vision of the Ministry at the executive level. Cross-functional teamwork is essential, especially between communications, operations, and policy units.

Work Environment & Ethics

Working at the Ministry was defined by its strong commitment to equity, inclusion, and accountability. Unlike the private sector, timelines are often influenced by legislative cycles and public consultations, which means balancing patience with precision. The emphasis on confidentiality and clarity in communication is paramount—every briefing note or report may eventually inform public policy.

Colleagues were incredibly supportive and willing to share their career journeys in public service. Weekly check-ins, mentorship coffee chats, and access to learning portals created a welcoming and growth-oriented atmosphere.

One important takeaway was the Ministry’s emphasis on evidence-based policy—decisions were never rushed and were always informed by extensive research and inclusive dialogues.

Required skills and knowledge

During my internship at the Ministry of Citizenship and Multiculturalism, I developed a balanced mix of hard and soft skills essential for a career in public policy and beyond. On the technical side, I strengthened my analytical abilities by working with demographic data, preparing briefing notes, and evaluating policy frameworks with measurable outcomes. I also became proficient in using government reporting tools and adhering to formal policy-writing standards. Equally important were the soft skills I honed: navigating cross-cultural communication during community consultations, adapting to a formal bureaucratic environment, and presenting complex findings in a clear, accessible way for both internal and public stakeholders. These experiences sharpened my critical thinking, diplomacy, and attention to detail—skills that are invaluable for any ESSEC student aiming to lead responsibly in business, government, or international organizations.

What I learned

One of the most impactful lessons I learned during my internship was how deeply interconnected public policy is with real-world social outcomes. I gained a clearer understanding of how decisions made at the ministry level directly influence funding for grassroots organizations, support for immigrant communities, and the implementation of inclusive practices across the province. I also came to appreciate the importance of patience and persistence in government work—policy change is often gradual, requiring continuous stakeholder engagement and rigorous documentation. Perhaps most importantly, I learned how to approach complex social challenges with a structured, evidence-based mindset, and how public institutions balance political direction with long-term societal goals.

Financial concepts related to my internship

I present below three financial concepts related to my internship: public budgeting, cost-benefit analysis, and grant funding allocation. These concepts were central to my work at the Ministry of Citizenship and Multiculturalism and helped me understand how financial principles are applied in public policy decision-making.

Public Budgeting

Public budgeting is the process by which government departments plan, allocate, and manage financial resources in alignment with policy goals. During my internship, I observed how the Ministry sets budget priorities based on strategic objectives such as promoting multiculturalism and supporting newcomer integration. This involved reviewing financial plans, aligning spending with program goals, and ensuring accountability in how public funds are used. Through this, I gained an understanding of how budgets are not just numbers but reflect broader social and political commitments.

Cost-Benefit Analysis

Cost-benefit analysis (CBA) is a tool used to evaluate the efficiency of public programs by comparing expected costs with anticipated benefits. I encountered this concept while working on internal policy reviews, where analysts used CBA to assess the viability of expanding or adjusting government initiatives. For example, I contributed to a report evaluating the effectiveness of community grants in reducing barriers for racialized youth. CBA helped inform whether the social outcomes achieved justified the public investment, which is crucial for responsible policy-making.

Grant Funding Allocation

Grant funding allocation refers to the process of distributing government funds to external organizations that align with specific policy objectives. One of my key tasks was helping review grant applications from community groups. This required assessing the financial soundness of proposals, projected outcomes, and how well each initiative aligned with Ministry goals. I learned how financial evaluation, transparency, and strategic impact all factor into deciding which organizations receive public funding. This experience deepened my appreciation for the financial scrutiny that underpins every public dollar awarded.

Why should I be interested in this post?

For an ESSEC student passionate about business, finance, and public impact, this internship experience highlights how government institutions like the Ministry of Citizenship and Multiculturalism play a vital role in shaping inclusive economic policies and managing resource allocation across diverse communities. Understanding how policy is developed, funded, and implemented not only broadens your perspective on governance but also strengthens your ability to assess financial decisions through a social lens. This exposure is especially relevant for those aiming to work in ESG investing, impact consulting, or public-private partnerships—where financial strategy and social responsibility go hand in hand.

The article was written in May 2025 by Adelaide RIDER-NICHOLSON (ESSEC Business School, Global Bachelor in Business Administration (GBBA) – Exchange Student, 2025).

In this article, Anant JAIN (ESSEC Business School, Grande Ecole Program – Master in Management, 2019-2022) talks about the hyperinflation in Hungary during the period 1945-46.

Introduction

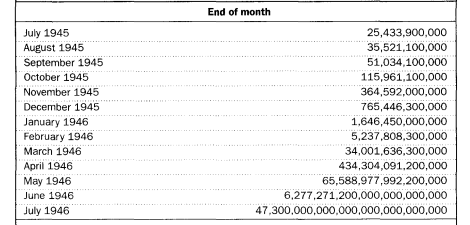

Hungary was affected by one of the most severe hyperinflation episodes ever seen, which was caused by the aftermath of World War II. During this time, from August 1945 to July 1946, the monthly inflation rate exceeded 19,000 percent as prices skyrocketed.

Causes Of Hyperinflation

Certain factors contributed to the economic and social catastrophe the country experienced:

War Devastation

The Economy of Hungary was in a very poor place due to the physical damage experienced in World War II. The war resulted in lost factories, bridges, railways, as well as the land that was destroyed rendered the supply chain and industrial output even further crippled. Many farms were also affected as huge portions of the land went wild and a lot of the required equipment was decimated as well.

Reparations & Occupation

Hungary was obligated to pay reparations to the Soviet Union, placing a significant strain on its economy. The Soviet occupation further exacerbated the situation by extracting resources, including raw materials and industrial goods, which were sent to the Soviet Union.

Excessive Money Printing

As a response to the economic issues, the Hungarian government drastically increased the money supply in an attempt to address economic concerns, which worsened the situation revealing the deficiencies of the Hungarian pengő. The central government continuously introduced bigger and bigger banknotes into the economy, but this only made the situation worse. The peak of this chaos ended in the introduction of the 100 quintillion pengo banknote which happened at the end of the hyperinflation period.

Hyperinflation peaked in July 1946, with prices doubling approximately every 15 hours. The highest inflation rate was estimated to be at 350% in the worst day and in its course, the value of the pengo began to lessen and when this era came to an end, it meant that 1 dollar was almost equivalent to 59 billion pengos. The sad case was that inflation bred poverty, this cycle would leave the masses struggling.

Impact on Society

The hyperinflation had devastating effects on Hungarian society:

Savings Wiped Out

People’s life savings were rendered worthless almost overnight. Many individuals who had saved diligently for years found themselves destitute. The middle class, in particular, was hit hard, as their financial security evaporated in a matter of months.

Barter System

The trade of products and services through the bartering system saw a massive resurgence. All sorts of markets began to trade items such as foodstuff, clothing and tools directly, thus avoiding the worthless currency. In this way, the barter system remained inefficient and further made daily life more difficult to manage.

Economic Instability

Businesses struggled to operate in such an unpredictable economic environment, leading to widespread closures and unemployment. Employers could not pay their workers in stable currency, and many businesses went bankrupt. The lack of a stable currency also hindered investment and economic planning.

Efforts To Stabilize The Situation

On August 1, 1946, the Hungarian government attempted to curb hyperinflation by introducing forint currency, substituting pengõ at rate of four hundred octillion pengos per unit of forint. The introduction of this currency was a major step towards the reclamation of the economy, yet it must be noted that the currency was coupled with other very important factors of the economy as well.

Monetary Reform

Through monetary reform, the government put in place restrictions that were aimed at minimizing the money supply, and thereby inflation. This included an end to printing money to the extreme and guaranteeing that the new currency is fully backed by tangible assets. These were necessary conditions for enhancing public confidence in the currency and in managing inflation.

Pengő tax reform

In the hyperinflationary context, a temporary measure, designated “tax pengő index,” was implemented. Operating on a daily basis, this system served to smoothen the conversion rates with the changes in the prices which helped the transactions to be adequately organized and the control over the economy to some extent restored.

Economic Reforms

In combination with the monetary reform, the government undertook much more comprehensive measures with the goal of directing the rebuilding of the economy. It included actions intended to boost industrial output, increase agricultural production and restore hidden economy. These reforms were significant in setting the stage for enduring and efficient economic policies.

4. International Aid and Cooperation

Hungary also received assistance from international organizations and allied nations. This aid was vital in providing the necessary resources for economic recovery and in supporting the stabilization efforts. International cooperation played a significant role in Hungary’s ability to overcome the hyperinflation crisis.

Impact On Today’s Hungarian Economy

The hyperinflation that went through Hungary in the years of 1945-46 shaped the country turning it into what can be viewed as today’s Hungary, and many of those changes became more obvious.

A. Key Economic Takeaway

1. Monetary Policy Awareness

The onslaught of hyperinflation was a serious lesson learnt by Hungary in managing the basics of monetary policy. Even this single historical experience of the country has changed how it thinks about inflation and more so about currency stability as it makes them very conscious about the chances of inflation and printing of money beyond acceptable limits.

2. Economic Reforms and Stability

The time of hyperinflation masqueraded the need for deep economic reforms including the inception of the new currency the forint and monetary dispensations. These reforms transformed the prospects of the Hungarian economy as one seeking sound management and policy measures to avert crises.

3. Institutional Strengthening

The lesson from the crisis was strong financial institutions and supervision is essential. In the last decades, Hungary has tried to create such capable institutions in order to cope with future economic shocks and secure their economy.

B. Social and Cultural Aspects

1. Public Trust In Currency

The hyperinflation phase notably diminished public confidence in its domestic currency, a sentiment that was difficult to restore. Such memories of history have made Hungarians very sensitive to episodes of inflation and depreciation of their currency. This makes Hungarians have an unpredictable attitude regarding policies concerning economic aspects and management of money.

2. Economic Resilience

The economic culture prevailing in Hungary after hyperinflation shows understanding economics and having a variety of ways to adjust in the economy. These experiences of the past are helping an entire generation in restructuring their businesses and household models.

C. Modern Economic Policies

1. Inflation Targeting

The central bank of Hungary ‘Magyar Nemzeti Bank’ (MNB) has adopted an approach of inflation targeting which has become part of its monetary policy framework. This was aimed at maintaining inflation at or between specified levels and focused also on maintaining other aspects of economic growth as well.

2. Fiscal Discipline

Hyperinflation has made Hungarians economically sound. They did learn after the painful experience of economic chaos. The nation is careful to prevent these situations from occurring again by first approaching the problem of balancing the budget while ensuring their public debt stays low.

Conclusion

The hyperinflation which took place in Hungary between 1945 and 1946 is perhaps the single most striking example of what can happen when economic management techniques are not employed and more pertinently how consequential the effects of war can be. While it is often recognized as one of the most severe cases of hyperinflation, only a handful of other instances throughout the world rival it. The key point to be understood from this episode is the significance of having a sound economic policy framework as well as international coordination, particularly for post-war rebuilding purposes.

The years 1945-1946 will be marked in history as the years of hyperinflation in Hungary, and it was devastating for the economy of Hungary. The memories of these years are still fresh and remain close to the countries monetary and fiscal policies. The cost of hyperinflation is now taken care of as many years have gone past, but the impact of hyperinflation can still be seen as ravage in the economy of Hungary. Hungary seems to have adopted a very watchful and strategic approach towards its economy.

In this article, Anant JAIN (ESSEC Business School, Grande Ecole Program – Master in Management, 2019-2022) talks about Bank Of Japan’s policy shift in 2024.

Introduction

In a significant alteration in its policy in 2024, the Bank of Japan (BoJ) has announced the abandonment of its long- held negative interest rate policy alongside the discontinuation of its Quantitative and Qualitative Monetary Easing (QQE) program with Yield Curve Control (YCC). Having made this announcement in September 2024, it is indeed a historic occasion in the economic history of Japan because it mirrors the growth potential of the economy while demonstrating the central banks trust in Japan’s economic recovery and the ability to revert back to a traditional, arms’ length monetary policy stance.

Understanding QQE With Yield Curve Control

Quantitative and Qualitative Monetary Easing (QQE)

Quantitative Easing (QE) involves central banks purchasing financial assets (like government bonds) from the market to increase money supply and stimulate economic activity.

Qualitative Easing (QE) focuses on the types of assets purchased, often including riskier assets (like corporate bonds or equities) rather than just government bonds. The idea is to influence not just the quantity of money but also the quality of the central bank’s balance sheet.

Yield Curve Control (YCC)

YCC involves targeting specific interest rates along the yield curve, typically focusing on short-term and long-term government bond yields. The central bank commits to buying or selling bonds in the market as necessary to keep these yields at or below the target levels.

QQE With Yield Curve Control

In the year 2013, the Bank of Japan incorporated the adoption of QQE With Yield Curve Control as a bold measure to address deflation issues and spur the economy in what was the introduction of its new strategy. It further aimed to influence borrowing and investments through lower interest rates across the entire yield curve by enhancing liquidity in the economy through large upwards shifts in the purchases of government issued bonds and other financial instruments.

The BoJ (on 21st September, 2016) expanded its efforts to implement monetary easing by adding the ability to control the entire yield curve by making appropriate adjustments to the interest rate of Japan’s 10-year government bonds. As a result, this policy resulted in the expansion of high liquidity in the country as Japan’s economy was already forecasted to face deflationary pressures. The policy was aimed at eventually pushing Japan’s economy to higher longer-term interest rates which in turn, would allow for greater economic stability in Japan.

The End Of Negative Interest Rates

Implemented in 2016, the BOJ’s negative interest rate policy was an unconventional measure aimed at stimulating economic activity by imposing a negative rate of -0.1% on excess reserves held by commercial banks. This policy was intended to encourage banks to lend more and invest, thereby boosting consumption and economic growth. However, after 8 years, the BOJ has decided to raise the short-term interest rate to a range of 0% to 0.1%. This shift towards normalization reflects the central bank’s recognition of improving economic conditions and the need to mitigate potential negative effects of prolonged negative rates, such as financial imbalances and reduced bank profitability.

While opting to end the negative interest policy, the BoJ has also opted for the gradual phasing out of its QQE with YCC program. This program, a central part of the BoJ’s approach to achieving its inflation target of 2% in the medium term, was of a gradual practice of large scale buying of assets and managing the yield curve in order to contain long term interest rates. The decision to discontinue this program indicates the BoJ’s belief that the economy is self-sustainable and does not require extraordinary measures to support growth and stable inflation.

Implications For The Japanese Economy

BoJ policy adjustment is likely to yield several changes with regards to different facets of the Japanese economy:

Interest Rates And Borrowing Costs

The removal of negative interest rates suggests that the cost of borrowing for a firm and a consumer is expected to rise. Although this may withdraw consumption and investment at the beginning, it is anticipated that this change in interest rates will encourage a better interaction with money by mitigating chances of asset bubble.

Financial Markets

A gradual return to normal levels of monetary policy may cause turbulence in financial markets as the participants are able to slowly adapt to the changes. However, on the flip side, it does point towards a return of business conditions that are expected to be more stable and predictable which in the long run may boost the confidence of investors.

Banking Sector

The removal of negative rates can in one way enhance the profitability of banking institutions. These financial intermediaries have always been working at unpalatable margins during the prevailing negative rate policy and with the new norm they should be able to make a decent lend and participate more meaningfully at the level of the economy.

Inflation And Economic Growth

The BoJ is confident that inflation will remain on average close to its target rate of 2%. Some of these inflation expectations could allow for better and resistant economic growth as businesses and the general populace refer to the new inflationary tendencies to make more informed decisions.

Global Implications Of The Policy Change Of Bank of Japan

The policies that the Bank of Japan has changed from are vastly relevant not only to Japan but also to the global economic network in general.

Global Financial Markets

As one of the world’s largest economies, changes in Japan’s monetary policy are capable of affecting world financial markets. Countries can supplement their capital structure from Japan after the era of negative interest rates and pooling of assets into the country will take place upon normalization of policy.

Exchange Rates

The shift in policies may have a direct effect on the Japanese yen’s rate. The enhanced interest rates may lead to a more robust yen which would in turn have an effect on Japan’s balance of trade and the cost of their exports. This, in a sense, may modify international trade relations and the economic status of nations that trade with Japan.

Central Bank Policies

Japan’s turn towards normalization, might compel other central banks to reconsider their own money policies especially in view of recovery of economies and the behavior of inflation during the time of recovery. In this respect, one may expect a more widespread pattern of policy tightening of monetary conditions across the globe economy.

Investment Strategies

Investors across the world may be forced to realign their strategies as a result of the new measures put in place by Japan’s key decision makers. Any shifts in interest rates and or conditions within the financial markets in Japan may impact investment strategies in terms of portfolio management and even risk management.

Conclusion

The Bank of Japan’s 2024 policy change is indicative of the beginning of the end for its unconventional monetary policies and is the start of a new chapter in the economic history of Japan. The BOJ, through the removal of negative interest rates and by discontinuing QQE with YCC, is demonstrating its faith in the performance and strength of the economy and is willing to implement more orthodox solutions. It is perceived that this action will have serious ramifications not only for Japanese economy and its financial markets but also for the prevailing global economic environment, paving the way for a more balanced and healthy future economy.

In this article, Olivia BRÜN (ESSEC Business School, Global Bachelor in Business Administration (BGBA), and ESIC Business School, Bachelor of Business Administration and Management (BBAM), 2022–2026) shares her professional experience as a Product Management Intern at MagentaTV, the TV and streaming service of Telekom Deutschland.

About the company

Telekom Deutschland’s flagship product, MagentaTV, supplies a wide variety of TV, streaming, and on-demand media to a large consumer base. Product Management is key to making the platform meet user expectations and align with the strategic goals of the company at large.

My group was tasked with improving customer happiness as part of the broad category of user experience, which encompasses long-term user engagement, content suggestion, and product discovery. This project cut across various industries, involving editorial management, user experience research and studies, marketplace research, and the implementation of customized content plans.

Logo of Telekom Deutschland.

Source: the company.

My internship

In the summer of 2023, I completed a two-month internship in the Product Management department of MagentaTV, which is a part of Telekom Deutschland. My duties covered major areas such as Editorial Campaign Management, Conceptual Development, Sales and Customer Journey Mapping, User Experience and Personalization.

As part of this internship, I gained valuable insights into the customer-focused aspects of the entertainment industry tied to Germany’s market-leading telecommunication provider and its management of digital media products. In addition, I was exposed to the intersection of product innovation, marketing technology, and corporate strategy in a large-scale organization.

My missions

During my internship, I was given the following responsibilities:

Organizing editorial functions to carry out emphasized content and promotional campaigns.

Conducting competitive and market research related to streaming in the DACH region.

Assessing customer experience, identifying areas of concern, and recommending improvements.

Leading workshops to improve user experience and create innovative product offerings.

Contributing to data-driven marketing initiatives, including personalization strategies for various user segments.

By completing these assignments, I gained a hands-on understanding of how consumer demands and technological limitations shape media products. Cross-functional collaboration with marketing, analytics, and user experience (UX) teams offered key insights into organizational dynamics.

Required skills and knowledge

The internship required sound analytical reasoning, structured conceptual thinking, and strong communication skills. Knowledge of consumer behaviour and digital trends was essential, especially in developing personalization strategies and campaign concepts. Technical tools like PowerPoint, Excel, and basic CMS were part of my daily toolkit. Above all, adaptability and attention to detail were vital in a fast-paced environment.

What I learned

My experience at MagentaTV gave me deeper insight into translating customer needs into meaningful product features. I learned how business strategy and product design merge in the context of digital platforms. I also developed an appreciation for how cross-functional teams collaborate across business, editorial, UX, and technical areas to shape user centered media services.

Financial concepts related my internship

Although I didn’t engage directly in financial analysis, my work was informed by a number of financial principles: customer lifetime value (CLV), return on investment (ROI) for campaigns, and subscription-based revenue models.

Customer Lifetime Value (CLV)

Retention strategies and personalization efforts were guided by the aim to increase CLV, a metric assessing the long-term value each customer adds to the business.

Return on Investment (ROI) for Campaigns

Evaluating editorial and marketing initiatives involved understanding KPIs that reflect campaign efficiency in terms of engagement, conversion, and acquisition costs.

Subscription-Based Revenue Models

Working with MagentaTV helped me understand the importance of recurring revenue, churn rates, and customer satisfaction in sustaining subscription-based business models.

Why should I be interested in this post?

This internship is particularly relevant for students interested in digital media, marketing, and product strategy. It illustrates how business thinking, technical execution, and customer engagement converge in real-world settings. It also highlights the importance of user-centric product development as a strategic advantage in subscription-based businesses.

ForaSoft – Streaming App UX Best Practices

An article offering industry insights into optimal user experience design in streaming applications, relevant to MagentaTV’s personalization and product innovation efforts.

Hotbot – Unlocking the Benefits of MagentaTV in 2023

A feature article exploring the core functionalities and improvements of MagentaTV, shedding light on user experience enhancements from a customer perspective.

MIPBlog – Best Interfaces of Streaming Platforms

Compares interface design across major platforms and positions MagentaTV within a competitive UX landscape — highly relevant to user journey mapping work.

About the author

The article was written in May 2025 by Olivia BRÜN (ESSEC Business School, Global Bachelor in Business Administration (BGBA), and ESIC Business School, Bachelor of Business Administration and Management (BBAM), 2022–2026), 2022–2026).

In this article, Olivia BRÜN (ESSEC Business School, Global Bachelor in Business Administration (BGBA), and ESIC Business School, Bachelor of Business Administration and Management (BBAM), 2022–2026) shares her professional experience as a Strategy Intern at ANXO Management Consulting.

About the company

ANXO is a moderately sized consultancy company based in Frankfurt am Main, Germany. The firm specializes in strategy development, organizational restructuring, transformation processes, and digitalization, offering its services to public and private sector organizations. ANXO guides organizations through complex change processes while also supporting the creation of sustainable strategic projects.

Logo of ANXO Management Consulting.

Source: the company.

I was with one team during my internship and provided support to partners on specific projects from time to time. I supported consultants in organizing internal and external workshops, assisted in the coordination of meetings, and was involved in communications and marketing functions.

My internship

From late May to mid-August 2024, I completed a three-month full-time internship at ANXO Management Consulting GmbH. As a Strategy Intern, I was involved in various internal and external projects, worked on client-related projects, attended association events, and supported projects across the whole organization.

One of the key aspects of my internship was working with Ralf Strehlau, President of the Federal Association of German Management Consultants (BDU) and Managing Director of ANXO. This experience gave me important insights into the operations of consultancy companies with regards to business and industry representation.

My missions

My tasks included:

Conducting analysis of industry trends and competitive forces for project leadership and consultants.

Organizing and documenting workshops and strategic planning sessions in the organization.

Enabling autonomous collaboration between internal divisions, clients, and professional bodies.

Planning a client-focused business trip to Düsseldorf and coordinating a VR pipeline demonstration at a trade show.

Helping in the formulation and organization of ANXO’s web relaunch initiative.

Organizing internal corporate functions involving management staff and consultants.

Required skills and knowledge

The internship required a high degree of self-management, professional communication skills, and the ability to work independently under strict time constraints. The ability to quickly absorb and analyze information and then convert it into practical outcomes was particularly critical.

Analytical research skills were necessary, especially for competitive analysis and preparing reports used in association meetings. Attention to detail and maintaining high standards in communication and operations were key to delivering value in a consultancy environment.

What I learned

My time at ANXO gave me a practical and contextualized understanding of the consultancy sector, especially within a medium-sized organization. I developed transferable skills in research, communication, and stakeholder engagement.

Taking part in a public trade fair presentation and collaborating with clients highlighted the importance of clear, confident communication in business settings. This experience helped me gain a deeper appreciation for the structured, analytical, and people-oriented nature of consulting work.

Financial concepts related my internship

I present below three financial concepts related to my internship: project cost awareness, resource utilization, and consulting business models.

Project Cost Awareness

While coordinating meetings and planning travel, I became more aware of how resource planning and time budgeting affect the implementation of consulting projects. For mid-sized firms juggling multiple projects, managing these elements efficiently is essential to financial sustainability.

Resource Utilization

I observed how consultants allocated time across various projects and tasks. This gave me initial exposure to utilization rates — a vital performance metric in consulting that affects staffing and overall profitability.

Consulting Business Models

Through internal coordination and client engagement support, I gained familiarity with the business economics of consulting firms, including time-based billing, project pricing strategies, and the economics of client retention.

Why should I be interested in this post?

This internship gave me practical insight into the consultancy industry and the dynamics of a medium-sized firm. For ESSEC students curious about project delivery, strategy, or professional services, this experience offers a realistic preview of consulting work, with its mix of analytical, operational, and interpersonal challenges.

Dartmouth CPD – Consulting 101 Resource

An overview of consulting industry fundamentals, useful for students exploring roles and skills relevant to consulting internships.

About the author

The article was written in May 2025 by Olivia BRÜN (ESSEC Business School, Global Bachelor in Business Administration (BGBA), and ESIC Business School, Bachelor of Business Administration and Management (BBAM), 2022–2026), 2022–2026).

In this article, Snehasish CHINARA (ESSEC Business School, Grande Ecole Program – Master in Management, 2022-2025) explores the optimal capital structure for firms, which refers to the balance between debt and equity financing. This post dives into the article written by Modigliani and Miller (1958) which explores the case of no corporate tax and a frictionless market (no bankruptcy costs).

Introduction to Capital Structure

Capital structure refers to the mix of debt and equity financing that a company uses to fund its operations and growth. It is a critical component of corporate finance, as it directly impacts a firm’s cost of capital, financial risk, and overall valuation. The choice of capital structure affects a company’s ability to raise funds, weather economic downturns, and pursue strategic investments.

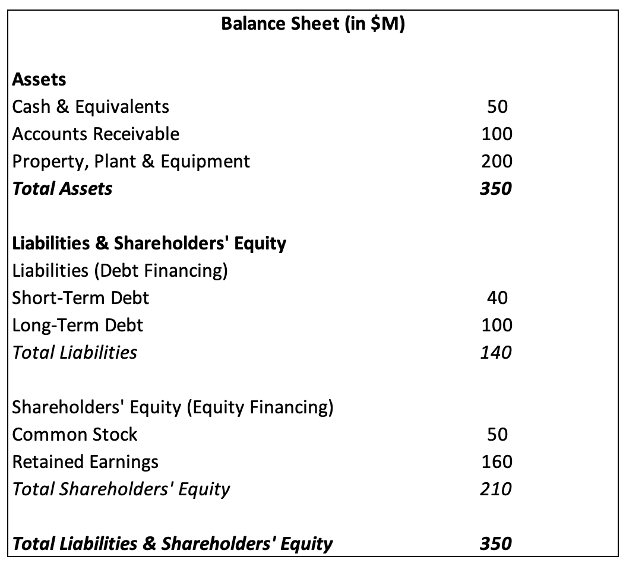

Capital structure is reflected in a company’s balance sheet, which provides a snapshot of its financial position at a given point in time. Specifically, it is composed of two primary financing sources:

Debt (Liabilities) – Found under the Liabilities section, debt includes short-term borrowings, long-term loans, bonds payable, and lease obligations. Debt financing requires periodic interest payments and repayment of principal, increasing financial obligations but also benefiting from potential tax shields.

Equity (Shareholders’ Equity) – Located under the Shareholders’ Equity section, equity includes common stock, preferred stock, retained earnings, and additional paid-in capital. Equity financing does not require fixed interest payments but dilutes ownership among shareholders.

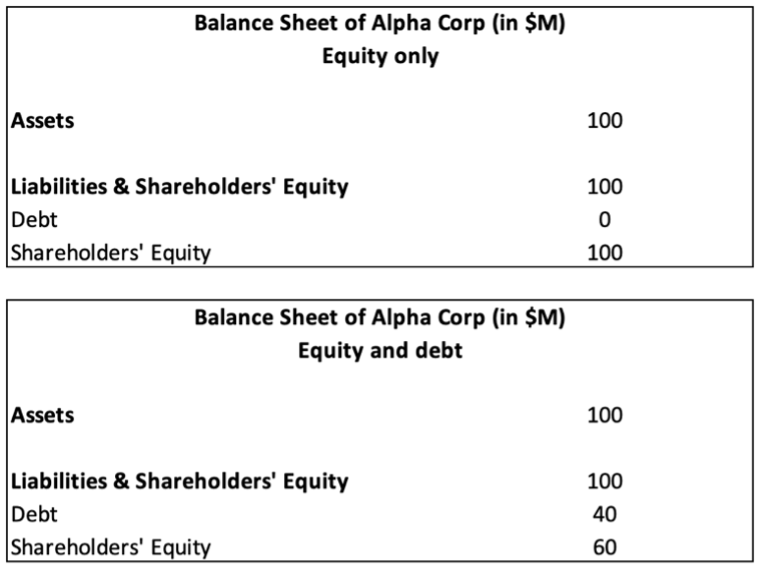

Table 1 below gives a simplified version of a balance sheet.

Table 1 – Simplified Balance Sheet Example

Table 1 shows that the firm finances its $350M in assets with $140M in debt (40%) and $210M in equity (60%), demonstrating a debt-to-equity ratio of 0.67 (=140/210). Additionally, the debt ratio, D/(D+E), measures the proportion of total financing that comes from debt 40% (=140/(140+210)). This indicates that a significant portion of capital is funded through borrowed money, allowing the company to take advantage of the use of debt, but also exposing it to higher financial risk if it faces difficulties in meeting debt obligations. These ratios are a few key indicators used to assess a company’s financial leverage and risk exposure.

A higher reliance on debt can lead to increased financial risk due to interest obligations, while too much equity financing may dilute shareholder returns. Therefore, finding an optimal capital structure is crucial for maintaining a healthy balance between risk, return, and financial stability.

Capital structure is one of the most fundamental decisions in corporate finance, influencing a firm’s financial stability, cost of capital, and overall value. At the heart of this discussion lies the Modigliani-Miller (M&M) theorems (M&M 1958 and M&M 1963), which provides the foundational framework for understanding how a company’s choice between debt and equity affects its valuation. However, while MM’s initial work (1958) proposed that capital structure is irrelevant in a frictionless market, real-world complexities such as taxation, bankruptcy costs, and financial distress challenge this assumption, leading to more nuanced theories.

The Modigliani-Miller 1958 Theorem (M&M 1958)

The Modigliani-Miller theorem (M&M 1958), introduced in 1958 by Franco Modigliani and Merton Miller, is a cornerstone of modern corporate finance. It provides a theoretical framework for understanding the role of capital structure in determining a firm’s value. M&M 1958’s core argument is that in a perfect market, a firm’s value is independent of its capital structure, meaning that the choice between debt and equity financing has no impact on firm valuation.

M&M 1958 Proposition I: Capital Structure Irrelevance

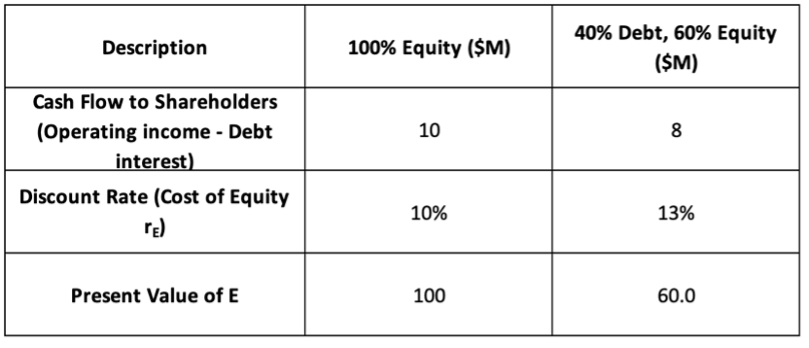

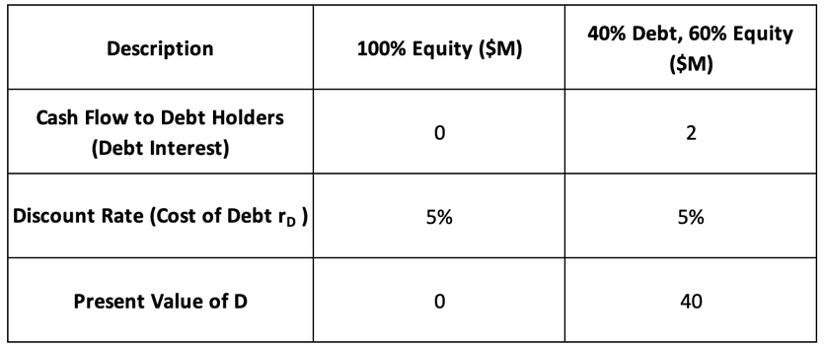

For the problem of the determination of the optimal capital structure of the firm, we assume that the firm (and its managers) seek to maximize the financial or economic value of the shareholders’ equity.

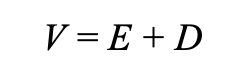

M&M’s first proposition states that, in a world with no taxes, no transaction costs, and perfect information, the total value of a firm (V) is unaffected by its financing decisions. Whether a company is financed with 100% equity, 100% debt (almost), or any combination of both, its market value remains the same because investors can create their own leverage through homemade financing.

M&M’s first proposition says that a company’s value is determined by its business operations (profits, assets, and growth potential), not by how it finances those operations.

Since in a perfect world, investors can create leverage on their own. If a company doesn’t use debt, an investor can borrow money separately to create the same effect. This means that whether the company uses debt or not, its overall value remains the same.

For a firm with market value V, total assets A, and financed by debt D and equity E:

According to M&M Proposition I, in a frictionless world:

where:

VL is the value of a levered firm using debt.

VU is the value of a unlevered firm not using debt but only equity

Key Assumptions:

No taxes (in reality, firms pay corporate taxes).

No bankruptcy costs (in reality, firms pay costs if they go bankrupt).

No financial distress (in reality, too much debt can make investors nervous).

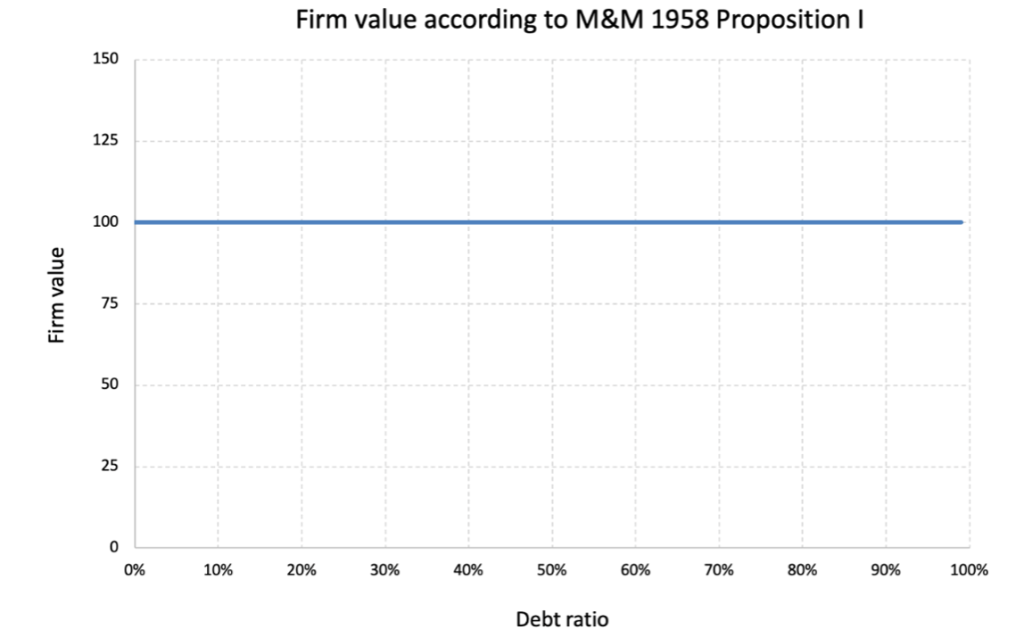

Figure 1. Firm Value vs Debt Ratio according to M&M 1958: Proposition I

In Figure 1, according to M&M 1958 Proposition I, the firm value remains constant regardless of the debt ratio. The flat blue line represents the idea that whether a firm is 100% equity-financed or takes on debt, its total value does not change in a perfect world with no taxes, no bankruptcy costs, and no market imperfections.

M&M 1958 Proposition II: Cost of Equity and Leverage Relation

While M&M Proposition I states that firm value is independent of capital structure, Proposition II explains how leverage affects the cost of equity (and then then total cost of financing measured by the weighted average cost of capital or WACC). It shows that as a firm increases its debt, equity becomes riskier, leading to an increase in the cost of equity (rE) to compensate for higher financial risk.

When a firm increases its leverage, its cost of debt (rD) is typically lower than its cost of equity (rE) due to the priority of debt holders in the capital structure and the fixed nature of interest payments. However, as leverage rises, the firm’s equity becomes riskier because debt obligations take precedence, amplifying the volatility of residual earnings available to shareholders. According to Modigliani-Miller Proposition II, this higher financial risk leads to an increase in the required return on equity (rE), as shareholders demand greater compensation for bearing the amplified risk exposure.

where:

rE = cost of equity for a levered firm

rU = cost of equity for an unlevered firm

rD = cost of debt

D/E = debt to equity ratio measuring leverage

This formula highlights that with higher leverage, the cost of equity increases, offsetting any benefit from the lower cost of debt. Thus, while leverage amplifies returns, it also raises financial risk, maintaining the firm’s overall cost of capital.

Shareholders bear more risk as leverage increases due to the following reasons –

Residual Claimants: Shareholders are last in line for cash flows, meaning higher debt increases fixed interest obligations, reducing the certainty of equity returns.

Earnings Volatility: With more debt, small fluctuations in operating profits cause larger swings in equity returns, making equity riskier.

Default & Financial Distress Risk: If debt levels rise too much, the firm faces a higher probability of default or financial distress, further increasing required equity returns.

WACC according to M&M 1958 Proposition II

The Weighted Average Cost of Capital (WACC) is a key financial metric that represents a firm’s overall cost of financing by combining the costs of equity and debt. Under Modigliani-Miller Proposition II (1958), the WACC is given by the formula:

Where:

WACC = Weighted Average Cost of Capital

E = Value of equity

D = Value of debt

rE = Cost of equity (which increases with leverage)

rD = Cost of debt (fixed by assumption)

M&M 1958 Proposition II states that as a firm increases its debt financing, its cost of equity rE rises to compensate for the additional financial risk. However, because debt is cheaper than equity, the lower cost of debt rD balances out the increase in rE, keeping WACC constant.

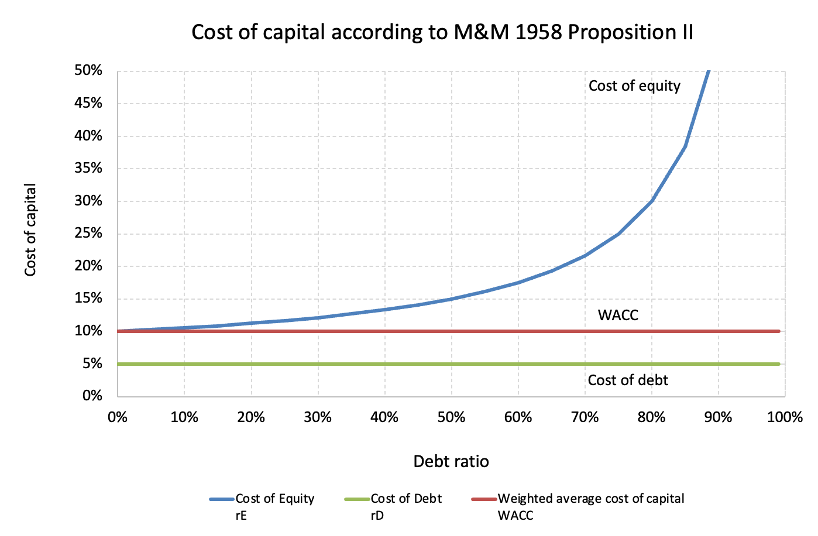

Figure 2. Modigliani-Miller View Of Gearing And WACC: No Taxation (MM 1958 Proposition II)

Based on Figure 2, implication for firms are as follows:

In a world with no taxes and bankruptcy costs, leverage does not create or destroy firm value.

Higher leverage increases equity risk, leading to higher required returns for shareholders.

The Weighted Average Cost of Capital (WACC) remains constant regardless of debt-equity mix.