In this article, Saral BINDAL (Indian Institute of Technology Kharagpur, Metallurgical and Materials Engineering, 2024-2028 & Research assistant at ESSEC Business School) explains the implied volatility surface: its characteristic shapes, static arbitrage constraints, and application using S&P 500 index options data.

Introduction

In financial markets characterized by uncertainty, volatility is a crucial factor in the valuation of derivative securities. For options traders, an option price is essentially volatility. Although options are traded at monetary prices, professionals routinely quote and compare them in terms of implied volatility (%), making volatility the common language of options markets. Moreover, in a reverse way, implied volatility occupies a central role as a forward-looking indicator that reflects the market’s expectations of future price fluctuations embedded in option prices.

Under the Black-Scholes-Merton (BSM) model, volatility is assumed to be constant and independent of option characteristics like the strike price (K) and the time to maturity (T). Empirical evidence, however, reveals that implied volatility varies across option contracts and especially depends on both parameters K and T of the option.

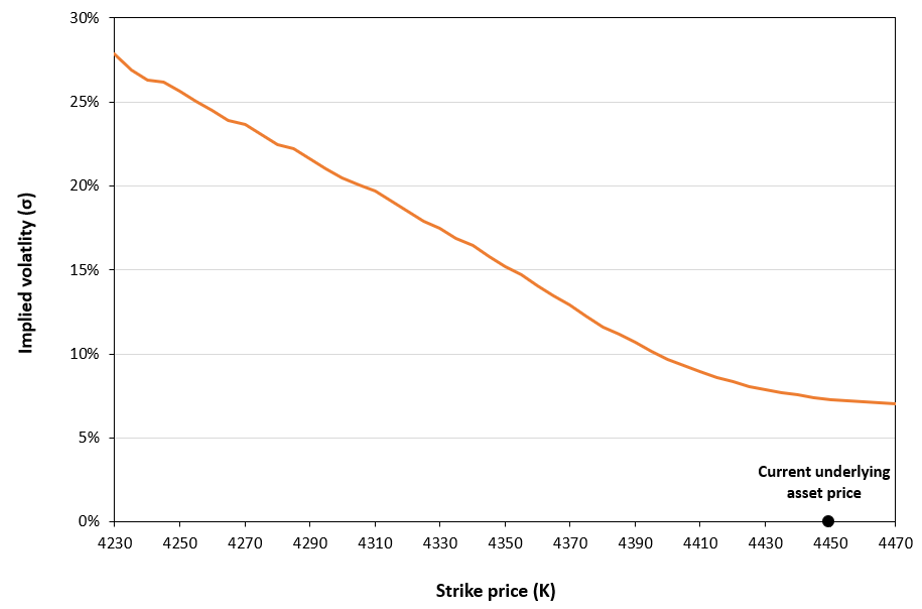

Implied volatility curves: the strike dimension

Volatility curves represent a cross-sectional view of the implied volatility surface (IVS), depicting the relationship between implied volatility and strike price for a fixed maturity. They are constructed by plotting implied volatility as a function of strike while holding time-to-maturity constant.

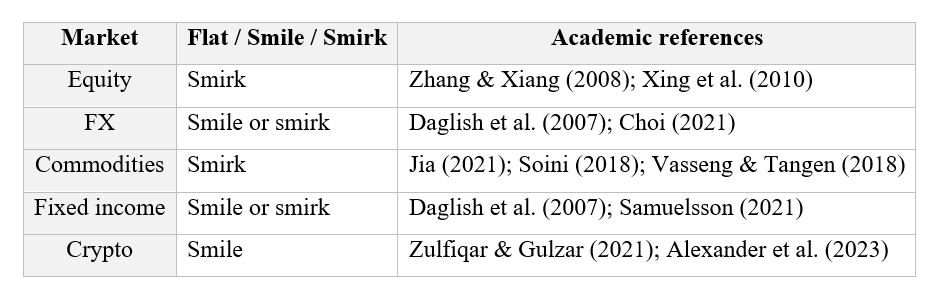

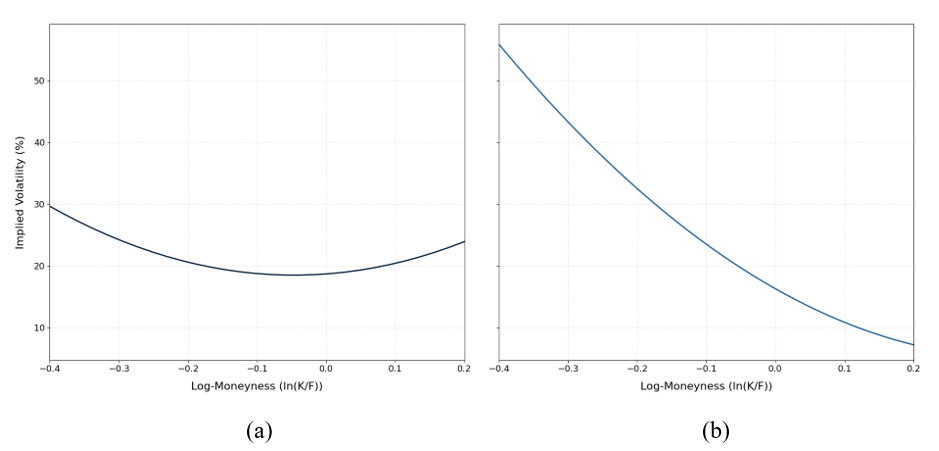

The volatility curves are commonly observed in two distinct shapes, most notably the volatility smile and the volatility smirk. A detailed discussion of the empirical relationship between implied volatility and option moneyness, the associated stylized facts, and their economic interpretation can be found in the article Volatility curves: smiles and smirks.

Figure 1 below illustrates the implied volatility smile (1a) and smirk (1b).

Figure 1a and 1b. Implied Volatility Smile and Smirk

Source: computation by the author (with python).

Term structure of implied volatility: the maturity dimension

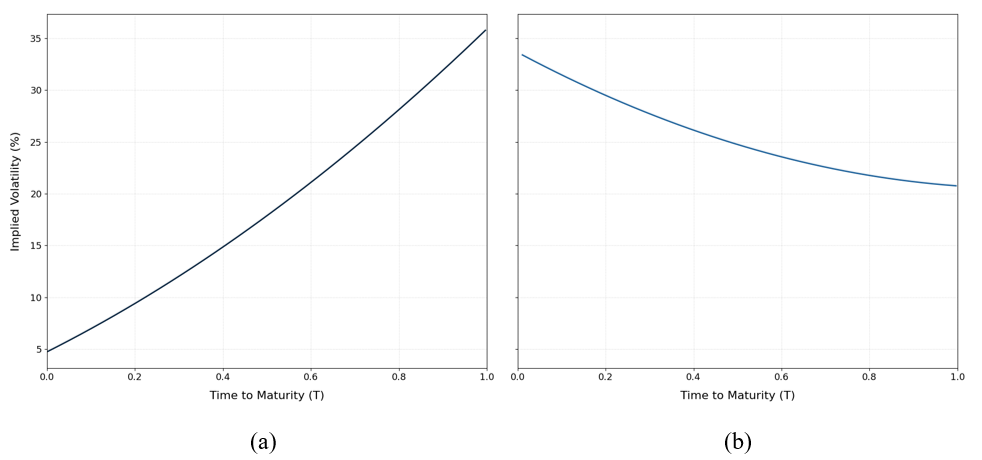

While volatility curves describe the strike dependence of implied volatility, the maturity dimension captures how implied volatility varies across expiration dates for a given strike. This relationship is commonly referred to as the term structure of implied volatility.

Using daily implied volatility data for S&P 100 index options (December 1983 to September 1987), Stein (1989) documented that volatility shocks are transmitted across maturities more strongly than predicted by standard rational expectations theory. Under this standard theoretical framework, because implied volatility is strongly mean-reverting, a near-term shock should naturally decay over time, causing long-dated implied volatilities to change by only a fractional amount. However, following an increase in short-dated implied volatility, long-dated implied volatilities tend to rise by a disproportionately large amount, indicating that changes in near-term uncertainty heavily influence market expectations over a broad range of maturities.

Using data for options on the S&P 500, FTSE 100, DAX 30, CAC 40, and Nikkei 225 stock indexes spanning the period May 9, 1994 to October 12, 2001, Mixon (2007) suggested mean reversion as a key characteristic of the implied volatility term structure. While short-dated implied volatilities exhibit substantial sensitivity to changes in market conditions, long-dated implied volatilities remain comparatively stable, reflecting expectations of convergence toward a long-run volatility level. Consequently, the term structure is generally upward sloping (contango) during periods of low market uncertainty but may become inverted (backwardation) during episodes of market stress, when short-term volatility rises sharply.

Figure 2 illustrates an upward-sloping (2a) and a downward-sloping (2b) implied volatility term structure.

Figure 2a and 2b. Implied Volatility Term Structure

Source: computation by the author (with python).

Christoffersen, Heston, and Jacobs (2009) demonstrate that the volatility term structure is not necessarily monotonic, arguing that capturing its true dynamics requires multifactor stochastic volatility frameworks. Evaluating European S&P 500 call options from 1990 through 2004, their empirical evidence reveals that implied volatility frequently displays significant curvature across maturities. This non-monotonic curvature is difficult to reconcile with traditional single-factor specifications like the benchmark Heston (1993) model, which restricts the term structure of implied volatility because it relies on only a single variance factor to model volatility over time.

Volatility Surface

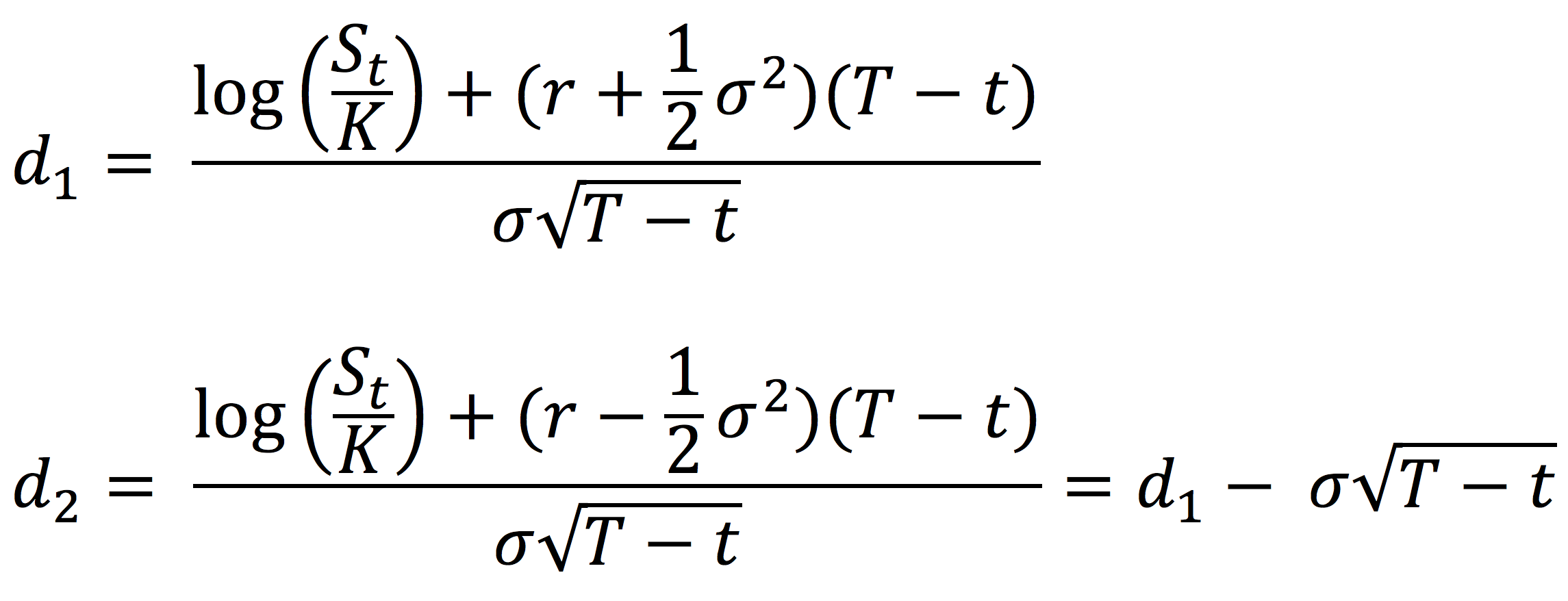

The volatility surface provides a three-dimensional representation of implied volatility across strike prices and maturities. It is represented by the function σ(K,T), which assigns an implied volatility to each combination of strike price K and time to maturity T that reproduces the observed market option prices under the Black-Scholes-Merton (BSM) model.

Constructed from a cross-section of traded options, the volatility surface provides a comprehensive description of how the market prices uncertainty across both strike price (K) and maturity (T).

Arbitrage constraints

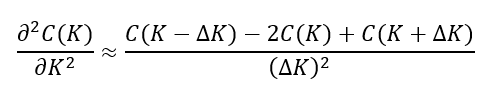

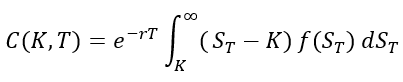

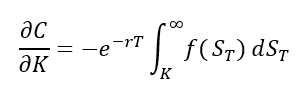

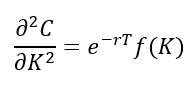

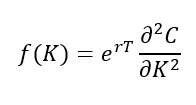

In practice, market option quotes are available only for a discrete set of strikes and maturities. Constructing a continuous volatility surface therefore requires interpolation and smoothing techniques. To ensure economic consistency, we must have σ(K,T) ≥ 0 for all strikes K and expirations T and the resulting surface must satisfy the static no-arbitrage conditions: namely the absence of butterfly arbitrage across strikes and calendar-spread arbitrage across maturities. (see, Breeden & Litzenberger, 1978; Gatheral, 2006)

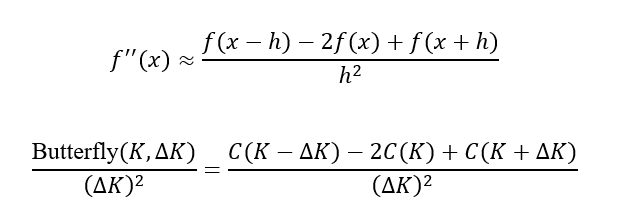

The absence of butterfly arbitrage requires option prices to remain convex with respect to strike. Equivalently, the risk-neutral probability density implied by option prices must remain non-negative across all strikes, this condition can be expressed as:

A violation of this condition implies a negative risk-neutral probability density over some range of strikes and leads to arbitrage opportunities.

The absence of calendar-spread arbitrage states that with increase in maturity of an option, it should not result in a reduction of its value, since a longer-dated option provides all the rights of an otherwise identical shorter-dated option together with additional time for favourable price movements to occur. In volatility surface modelling, this condition is typically expressed in terms of the total implied variance

where σBS(K,T) denotes the Black-Scholes-Merton implied volatility for strike K and maturity T. Total implied variance measures the total accumulated expected variance over the entire life of the option

For a fixed strike, total implied variance must be non-decreasing with maturity

A violation would imply that a longer-dated option embeds less cumulative uncertainty than a shorter-dated option at the same strike, resulting in an arbitrage opportunity.

Together, the butterfly-arbitrage and calendar-spread-arbitrage constraints ensure that the interpolated volatility surface produces arbitrage-free option prices and a valid risk-neutral distribution.

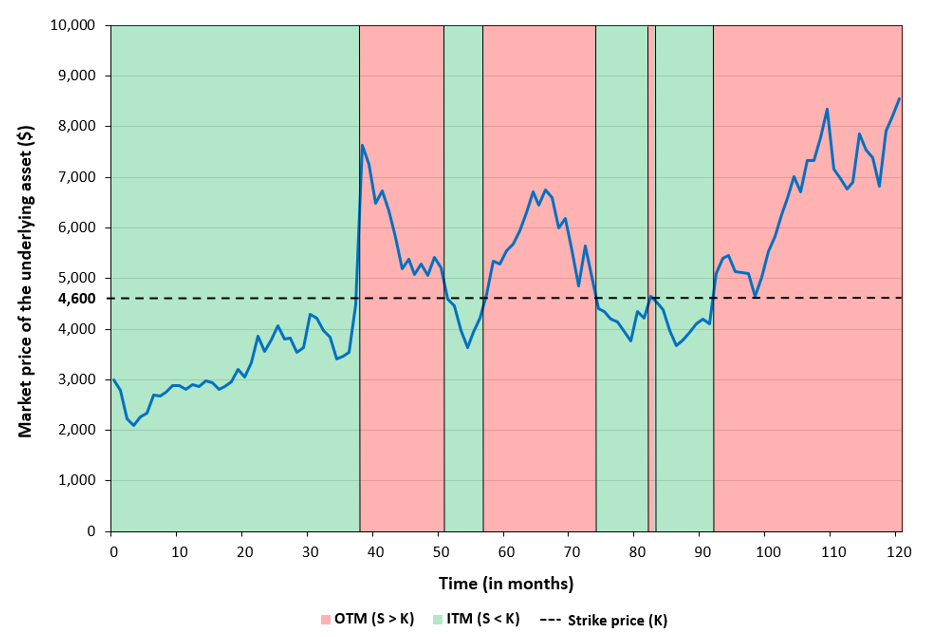

An Empirical Analysis of the S&P 500 Implied Volatility Surface

In this section, we discuss how an implied volatility surface can be estimated from the S&P 500 index observed market option prices using a parametric model to fit the data and how the parameters can be adjusted to represent different macro-economic stress conditions.

Data collection and filtration

To construct the implied volatility surface, we import the S&P 500 index option chain (set of call and put options across various strikes and maturities) directly from Yahoo! Finance. Because raw market data often contains stale quotes and asynchronous prices, we apply a robust set of filtering techniques to clean the dataset before model estimation.

First, we apply illiquidity filters, removing any option contracts with zero trading volume or zero open interest. Second, we filter the dataset to retain only Out-of-the-Money (OTM) options (OTM puts where K < S0, and OTM calls where K > S0). This is a standard practice, as implied volatility is theoretically independent of option type due to Put-Call Parity, focusing strictly on OTM contracts ensures we utilize the most liquid instruments (liquidity being measured by the bid-ask spread) to minimize pricing noise.

Third, we enforce intrinsic value and no-arbitrage boundary conditions. Any contracts with mispriced or economically impossible quotes are filtered out by verifying the upper and lower price bounds for the option contracts as given below

where:

- K: strike price of the option

- S0: spot price of the underlying asset

- T: time to maturity

- C: mid-price of a call option

- P: mid-price of a put option

- r: risk-free rate

- q: continuous dividend yield

Finally, we check for vertical (strike) arbitrage to ensure the data adheres to fundamental shape restrictions. We sort the contracts by time-to-maturity and then by strike price in ascending order. We then verify shape monotonicity: for any given maturity, call prices must strictly decrease as the strike price increases, and put prices must strictly increase as the strike price increases. Applying these standard empirical filters ensures a clean, arbitrage-free dataset ready for surface estimation.

Methodology

To model and plot the implied volatility surface as shown below in Figure 1, we implement a parametric approach originally proposed by Dumas, Fleming, and Whaley (1998). This technique fits a deterministic volatility function (DVF) directly through the observed option market data. Under this framework, the implied volatility function is expressed as a second-order polynomial function across log-moneyness (M) and time-to-maturity (T):

where:

- α0 : Measures the baseline implied volatility level where both log-moneyness and time-to-maturity are equal to zero. Geometrically, this shifts the entire surface straight up or down uniformly

- α1 : Measures the rate of change of volatility across different strikes. Geometrically, this rotates the surface along the moneyness axis, tilting the left wing (puts) up and the right wing (calls) down.

- α2 : Measures the rate of change of the curvature across strikes, defining how sharply the volatility curve bends. Geometrically, this bends the surface into a U-shaped bowl or flattens it into a smooth plane.

- α3 : Measures the rate of change of volatility across the horizon, establishing the slope of the term structure. Geometrically, this tilts the surface front-to-back, altering the premium difference between short-term and long-term contracts.

- α4 : Measures the rate of change of the curvature in the volatility in the term structure across different maturities. Geometrically, this creates a non-linear bend along the time horizon axis.

- α5 : Measures the co-dependency between moneyness and time-to-maturity, modelling how the skew changes as maturity extends. Geometrically, this causes the corners to bend upward or downward simultaneously.

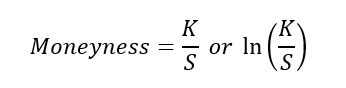

In the polynomial function above, we utilize the log-forward moneyness (M), defined as:

where F0 is the forward price of the underlying asset, calculated as:

This is usually done in practice because it is F0, and not S0, that represents the expected stock price on the option’s maturity date in a risk-neutral world. Consequently, traders often define an “at-the-money” option as a contract where K = F0, rather than an option where K = S0.

To fit this model, we first apply a numerical root-finding algorithm to invert the Black-Scholes-Merton (BSM) pricing model against observed market prices (mid prices defined as the average of bid and ask prices) to extract the market implied volatilities. We restrict our sample to contracts with maturities under one year (T < 1.0) and a log-moneyness of |M| < 0.45. This filters out deep Out-of-the-Money (OTM) options, which typically suffer from low trading volumes and wide bid-ask spreads, as they are primarily held for structural tail-hedging by institutional investors.

Finally, we apply Ordinary Least Squares (OLS) regression to the filtered dataset to solve for the six α parameters simultaneously. Once estimated, these parameters can be used to generate the implied volatility curves, term structures, and 3D surfaces under various macroeconomic stress scenarios, as discussed below.

Empirical Results

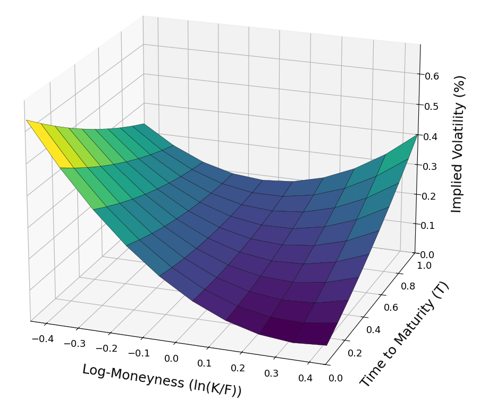

Figure 3 illustrates the estimated implied volatility surface of the S&P 500 index using options data collected on June 18, 2026. The market environment at the time of collection was defined by an index spot price (S0) of $7496.04, a risk-free interest rate (r) of 3.658%, and a continuous dividend yield (q) of 1.04%. Based on these inputs, the resulting empirical surface is presented below.

Figure 3. Implied Volatility Surface of the S&P 500 index options (June 18, 2026)

Source: computation by the author (with python).

From the surface, we can observe that amid ongoing US-Iran tensions in the Middle East, out-of-the-money (OTM) put options exhibit high implied volatility for short-term maturities. This reflects panic buying of downside protection due to fears of conflict escalation and immediate uncertainty in the market. Toward the far end of the maturity, however, the surface balances out with OTM call options. This indicates that while near-term sentiment is dominated by risk aversion, long-term market expectations are highly speculative, positioning for a potential recovery once the geopolitical uncertainty resolves. To isolate and observe these market dynamics more precisely, the individual implied volatility smiles (by strike) and term structures (by maturity) are plotted below.

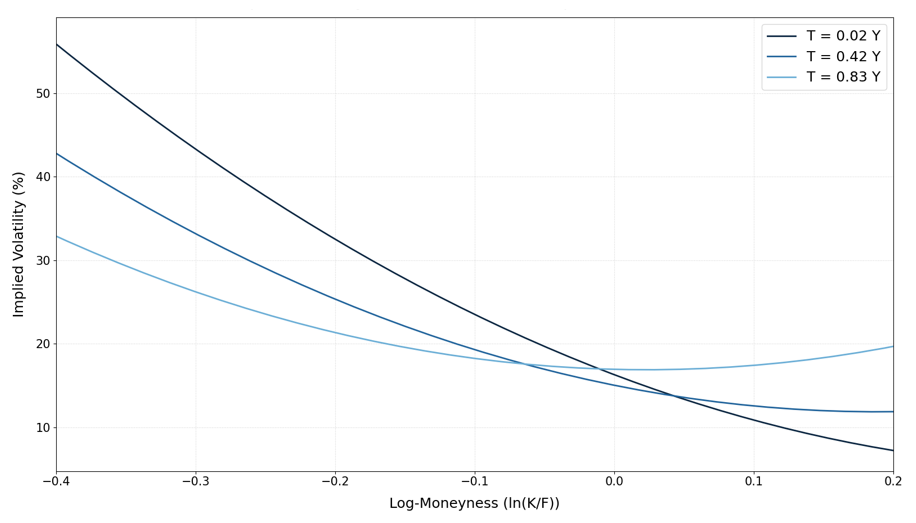

Figure 4 illustrates the implied volatility curves for three distinct maturities. As discussed above, we can clearly observe the steep downside skew flattening out and transitioning into a asymmetric smile as maturity increases.

Figure 4. Implied Volatility Curves of the S&P 500 options (June 18, 2026)

Source: computation by the author (with python).

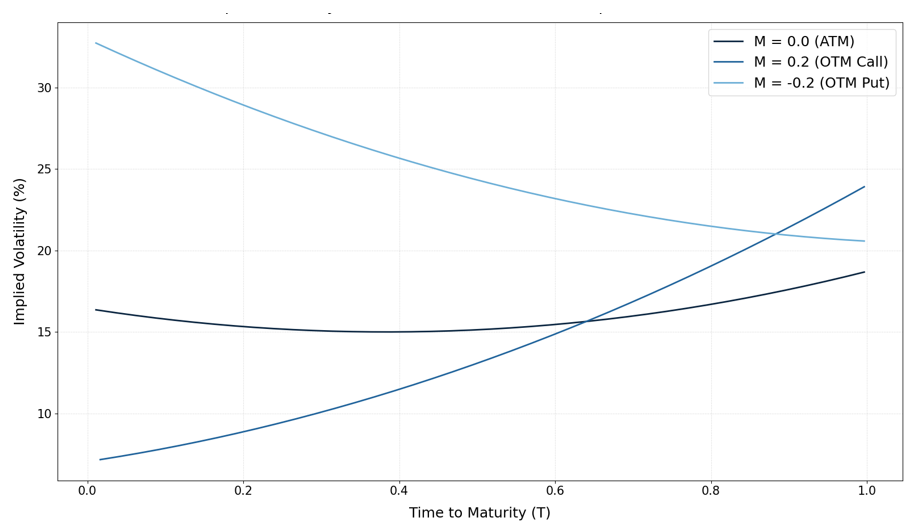

Figure 5 illustrates the implied volatility term structure (up to 1 year) for three different strike prices. For out-of-the-money (OTM) call options, we can observe that the term structure is upward-sloping, indicating a long-term uncertainty alongside expectations of an upward market movement. Conversely, the OTM put option term structure is inverted and reflecting high short-term panic and uncertainty. Over the time horizon, this near-term panic subsides, balancing out with the OTM call options in the long run.

Figure 5. Implied Volatility Term Structure of the S&P 500 index options (June 18, 2026)

Source: computation by the author (with python).

The at-the-money (ATM) option term structure exhibits a shallow, non-monotonic U-shape, characterized by elevated short-dated volatility, a flattened middle region, and higher long-term volatility. This reflects that, in the short-to-medium term, the curve demonstrates the classic mean-reversion, where the immediate geopolitical shock dissipates and flattens out over a 3-to-6-month horizon. Conversely, the upward drift at the longer end of the mature horizon reflects the structural term premium demanded by investors to account for broader, open-ended macroeconomic uncertainties, as discussed above in the stylized facts section.

Structural Shifts under Macroeconomic Stress: A Comparative Scenario Analysis

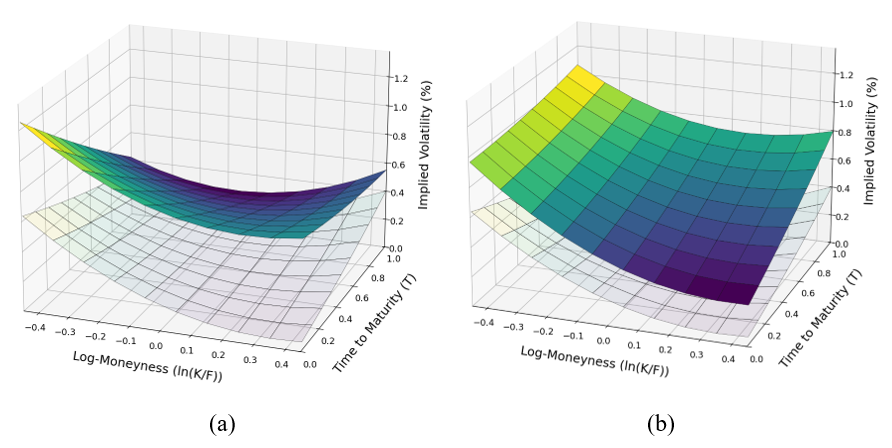

Figure 6 provides a compelling visual framework for observing how the implied volatility surface structurally shifts under different stress conditions. The surface on the left (a) represents the systemic crash caused by the COVID-19 pandemic (2020), while the surface on the right (b) illustrates the hypothetical impact on index options if the ongoing US-Iran conflict were to escalate significantly. These surfaces are constructed by adjusting the values of the six model parameters estimated in the preceding section; as such, they serve as illustrative examples of structural shifts rather than exact numerical forecasts.

Figures 6a and 6b. Implied Volatility Surface of the S&P 500 options under different stress environments

Source: computation by the author (with python).

Note: In both figures, the lightly shaded surface serves as the baseline, representing the actual market implied volatility surface as of June 18, 2026.

From Figure 6a, we can observe a massive surge in overall implied volatility across the board, driven by widespread panic buying of both out-of-the-money (OTM) puts and calls. This systemic shock resulted in a relatively flatter skew but severe inversion across the maturity spectrum, reflecting the acute, immediate fear of economic collapse as global lockdowns were implemented.

In contrast, Figure 6b models a scenario where the US-Iran conflict escalates into a full-scale regional crisis. Such an event would severely disrupt global oil supply chains, acting as a prolonged macroeconomic drag that hits S&P 500 corporate earnings over many months. Because this represents a lingering economic threat rather than an overnight liquidity freeze, the market’s response is highly asymmetric: demand is heavily concentrated in OTM puts for long-term downside protection and a steady increase in long-term implied volatility across the maturity.

While these stress scenarios represent extreme events, day-to-day movements follow structured patterns. Cont and Da Fonseca (2002) showed that daily dynamic deformations of the S&P 500 volatility surface are not chaotic. Instead, using principal component analysis, they demonstrated that surface movements are driven by just a few common statistical factors: parallel shifts, changes in the strike slope (skew), and twists in the maturity curvature.

You can download the Python code provided below, for the construction of the implied volatility curves, term structures and surfaces under different stress conditions as discussed above.

Alternatively, you can download the R code below with the same functionality as in the Python file.

Volatility Surface Models

A volatility surface determines the risk-neutral distributions implied by option prices (see Option Implied Risk-Neutral Distribution), but it does not uniquely specify the underlying stochastic process governing asset-prices. As highlighted by Cont (2006), this introduces significant model uncertainty: different mathematical frameworks can calibrate perfectly to the exact same market volatility surface today, yet yield wildly divergent prices and hedges for exotic options because they imply different future surface dynamics. Consequently, a substantial body of research has focused on developing models capable of reproducing both the observed shape of the volatility surface and its evolution through time.

The principal modelling approaches include local volatility models, stochastic volatility models, parametric surface models and, more recently, rough volatility models.

Local Volatility Models

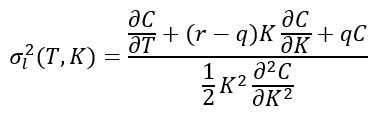

In the standard BSM formula, volatility is assumed constant, which however does not correspond to reality, as markets exhibit volatility smile and skews. Local volatility model, extends the BSM, by assuming that volatility is a function of stock price (St) and time (t), and the instantaneous local volatility is given by σt( St,t).

The Dupire (1994) formula that links the instantaneous local volatilities, to the implied volatility surface is given as follows:

Stochastic Volatility Models

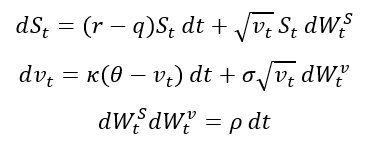

Stochastic volatility refers to the modelling of volatility using time-dependent stochastic processes, in contrast to the constant volatility assumption made in the standard BSM model. These models are better able to capture the observed features such as volatility clustering and mean reversion. One of the most widely used stochastic volatility models is the Heston (1993) model. The model describes the dynamics of the underlying asset price and its variance using a system of two coupled stochastic differential equations (SDEs), given by:

Where:

- St: is the asset price

- vt: is the instantaneous variance

- r: is the risk-free interest rate

- q: is the continuous dividend yield

- κ: is the speed of mean reversion

- θ: is the long-run variance level

- σ: is the volatility of variance (volatility-of-volatility)

- ρ: is the correlation between shocks to the asset price and variance

Parametric Surface Models

Parametric volatility surface models are used to interpolate and extrapolate implied volatility across strikes and maturities, for sparse or illiquid strikes and ensure the resulting surface is free from static arbitrage (butterfly and calendar arbitrage).

Among the most widely used approaches is the SVI (Stochastic Volatility Inspired) parametrization, developed by Gatheral and Jacquier (2014), which is commonly applied to equity and index volatility surfaces. It models the total implied variance as a function of log-moneyness, providing a parsimonious representation of the volatility smile.

Other important parametric frameworks include the SABR model (Stochastic Alpha, Beta, Rho), which is widely used in interest rate and FX markets, and SSVI (Surface SVI), which extends the SVI framework to ensure arbitrage-free surface dynamics across maturities.

Rough Volatility Models

Rough volatility models represent one of the most important recent developments in volatility modelling. Gatheral, Jaisson, and Rosenbaum (2018) provided the empirical evidence that log-volatility behaves essentially as a fractional Brownian motion with Hurst exponent H of order 0.1, at any reasonable timescale.

The Hurst exponent (H) is a statistical parameter that characterises the roughness of a stochastic process: when H = 0.5, the process reduces to a standard Brownian motion with no memory, corresponding to a random walk. Whereas, values of H > 0.5 indicate persistent behaviour, while H < 0.5 imply anti-persistence, where increments tend to reverse direction more frequently, leading to rougher sample paths.

This observation, led to adoption of the fractional stochastic volatility (FSV) model of Comte and Renault (1998). The Rough FSV (RFSV) in contrast to FSV, is remarkably consistent with financial time series data. Compared to classical stochastic volatility models, it better captures the extremely rough nature of volatility paths and enables improved forecasting of realized volatility.

Why should I be interested in this post?

Implied volatility surfaces are among the most important tools in modern quantitative finance. They play a central role in the pricing and hedging of derivatives, particularly exotic options, and are widely used in risk management, stress testing, and scenario analysis. A good understanding of volatility surfaces is therefore essential for students, practitioners, and anyone seeking a career in derivatives, quantitative finance, trading, or risk management.

Related posts on the SimTrade blog

▶ Saral BINDAL Historical Volatility

▶ Saral BINDAL Implied Volatility and Option Prices

▶ Saral BINDAL Volatility curves: smiles and smirks

▶ Saral BINDAL Option Implied Risk-Neutral Distribution

Useful resources

Academic research on Option pricing

Black, F., & Scholes, M. (1973). The pricing of options and corporate liabilities. Journal of Political Economy, 81(3), 637-654.

Breeden, D. T., & Litzenberger, R. H. (1978). Prices of state-contingent claims implicit in option prices. Journal of Business, 51(4), 621-651.

Hull J.C. (2015) Options, Futures, and Other Derivatives, Eleventh Edition, Global Edition, Chapter 15 – The Black-Scholes-Merton model, 338-369.

Merton, R.C. (1973). Theory of rational option pricing. The Bell Journal of Economics and Management Science, 4(1), 141-183.

Academic Research on Stylized Facts on Option Volatility

Christoffersen, P., Heston, S., & Jacobs, K. (2009). The shape and term structure of the index option smirk: Why multifactor stochastic volatility models work so well. Management Science, 55(12), 1914-1932.

Heston, S. L. (1993). A closed-form solution for options with stochastic volatility with applications to bond and currency options. The Review of Financial Studies, 6(2), 327-343.

Mixon, S. (2007). The implied volatility term structure of stock index options. Journal of Empirical Finance, 14(3), 333-354.

Stein, J. C. (1989). Overreactions in the options market. Journal of Finance, 44(4), 1011-1023.

Academic Research on Empirical Analysis of Implied Volatility Surfaces

Cont, R., & Da Fonseca, J. (2002). Dynamics of implied volatility surfaces. Quantitative Finance, 2(1), 45-60.

Gatheral, J. (2006). The Volatility Surface: A Practitioner’s Guide. John Wiley & Sons, Chapter 2 – Implied Volatility Surface, 25-42.

Hull J.C. (2015) Options, Futures, and Other Derivatives, Eleventh Edition, Global Edition, Chapter 20 – Volatility smiles and volatility surfaces, 451-467.

Dumas, B., Fleming, J., and Whaley, R.E. (1998). Implied volatility functions: Empirical tests. The Journal of Finance, 53(6), 2059-2106.

Academic Research on Implied Volatility Surface Models

Comte, F., & Renault, E. (1998). Long memory in continuous-time stochastic volatility models. Mathematical Finance, 8(4), 291-323.

Cont, R. (2006). Model uncertainty and its impact on the pricing of derivative instruments. Mathematical Finance, 16(3), 519-547.

Dupire, B. (1994). Pricing with a smile. Risk, 7(1), 18-20.

Gatheral, J., & Jacquier, A. (2014). Arbitrage-free SVI volatility surfaces. Quantitative Finance, 14(1), 59-71.

Gatheral, J., Jaisson, T., & Rosenbaum, M. (2018). Volatility is rough. Quantitative Finance, 18(6), 933-949.

Heston, S. L. (1993). A closed-form solution for options with stochastic volatility with applications to bond and currency options. Review of Financial Studies, 6(2), 327-343.

About the author

The article was written in June 2026 by Saral BINDAL (Indian Institute of Technology Kharagpur, Metallurgical and Materials Engineering, 2024-2028 & Research assistant at ESSEC Business School). His interests include tracking geopolitical developments and analysing their direct impact on macroeconomic factors such as inflation, trade balances, and currency volatility, with a focus on using data to quantify these global economic ripple effects.

Discover all posts written by Saral BINDAL.