This article written by Akshit GUPTA (ESSEC Business School, Grande Ecole Program – Master in Management, 2019-2022) presents the derivative contract of interest rate swaps used to hedge interest rate risk in financial markets.

Introduction

In financial markets, interest rate swaps are derivative contracts used by two counterparties to exchange a stream of future interest payments with another for a pre-defined number of years. The interest payments are based on a pre-determined notional principal amount and usually include the exchange of a fixed interest rate for a floating interest rate (or sometimes the exchange of a floating interest rate for another floating interest rate).

While hedging does not necessarily eliminate the entire risk for any investment, it does limit or offset any potential losses that the investor can incur.

Forward rate agreements (FRA)

To understand interest rate swaps, we first need to understand forward rate agreements in financial markets.

In an FRA, two counterparties agree to an exchange of cashflows in the future based on two different interest rates, one of which is a fixed rate and the other is a floating rate. The interest rate payments are based on a pre-determined notional amount and maturity period. This derivative contract has a single settlement date. LIBOR (London Interbank Offered Rate) is frequently used as the floating rate index to determine the floating interest rate in the swap.

The payoff of the contract is as shown in the formula below:

(LIBOR – Fixed Interest Rate) * Notional amount * Number of days / 100

Interest rate swaps (IRS)

An interest rate swap is a hedging mechanism wherein a pre-defined series of forward rate agreements to buy or sell the floating interest rate at the same fixed interest rate.

In an interest rate swap, the position taken by the receiver of the fixed interest rate is called “long receiver swaps” and the position taken by the payer of the fixed interest rate is called “long payer swaps”.

How does an interest rate swap work?

Interest rate swaps can be used in different market situations based on a counterparty’s prediction about future interest rates.

For example, when a firm paying a fixed rate of interest on an existing loan believes that the interest rate will decrease in the future, it may enter an interest rate swap agreement in which it pays a floating rate and receives a fixed rate to benefit from its expectation about the path of future interest rates. Conversely, if the firm paying a floating interest rate on an existing loan believes that the interest rate will increase in the future, it may enter an interest rate swap in which it pays a fixed rate and receives a floating rate to benefit from its expectation about the path of future interest rates.

Example

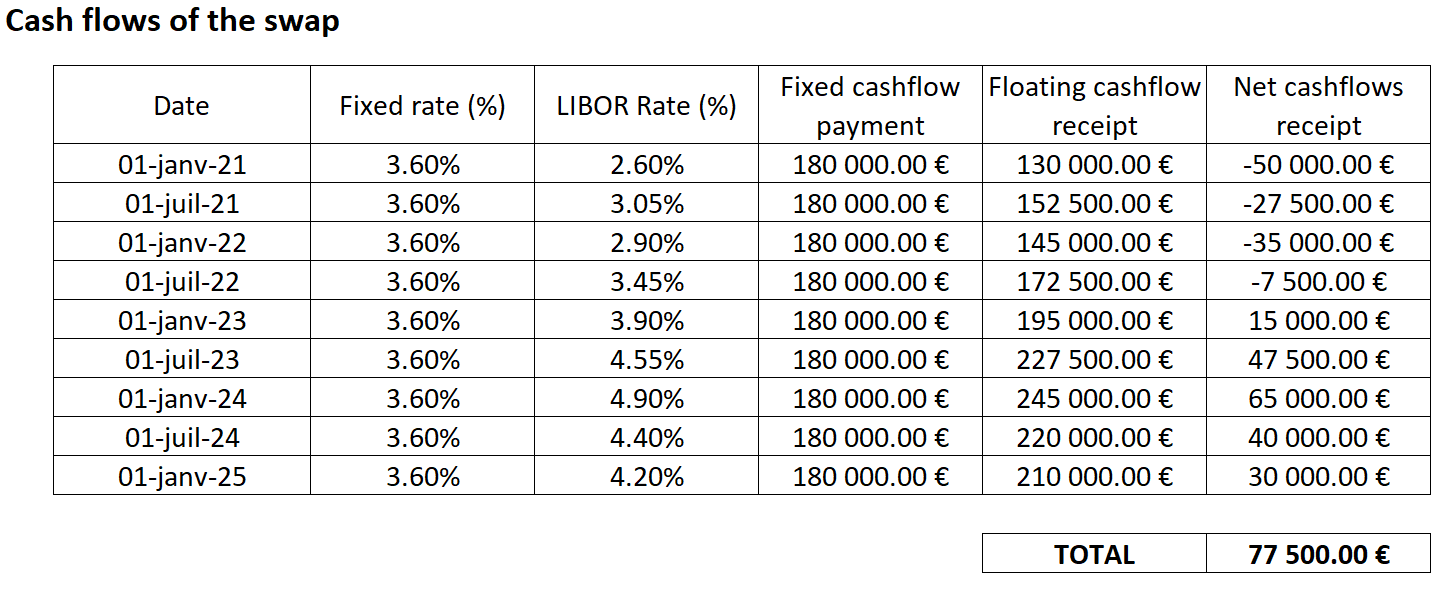

Let’s consider a 4-year swap between two counterparties A and B on January 1, 2021. In this swap, counterparty A agrees to pay a fixed interest rate of 3.60% per annum to counterparty B every six months on an agreed notional amount of €10 million. Counterparty B agrees to pay a floating interest rate based on the 6-month LIBOR rate, currently at 2.60%, to Counterparty A on the same notional amount. Here, the position taken by Counterparty A is called long payer swap and the position taken by Counterparty B is called the long receiver swap. The projected cashflow receipt to Counterparty A based on the assumed LIBOR rates is shown in the below table:

Table 1. Cash flows for an interest rate swap.

Source: computation by the author

In the above example, a total of eight payments (two per year) are made on the interest rate swap. The fixed rate payment is fixed at €180,000 per observation date whereas the floating payment rate depend on the prevailing LIBOR rate at the observation date. The net receipt for the Counterparty A is equal to €77,500 at the end of 5 years. Note that in an interest rate swap the notional amount of €10 million is not exchanged between the counterparties since it has no financial value to either of the counterparties and that is why it is called the “notional amount”.

Note that when the two counterparties enter the swap, the fixed rate is set such that the swap value is equal to zero.

Excel file for interest rate swaps

You can download below the Excel file for the computation of the cash flows for an interest rate swap.

Related Posts

▶ Jayati WALIA Derivative Markets

▶ Akshit GUPTA Forward Contracts

▶ Akshit GUPTA Options

Useful resources

Hull J.C. (2015) Options, Futures, and Other Derivatives, Ninth Edition, Chapter 7 – Swaps, 180-211.

www.longin.fr Pricer of interest swaps

About the author

Article written in December 2022 by Akshit GUPTA (ESSEC Business School, Grande Ecole Program – Master in Management, 2019-2022).