This article written by Akshit GUPTA (ESSEC Business School, Grande Ecole Program – Master in Management, 2019-2022) introduces Forward contracts.

Introduction

Forward contracts form an essential part of the derivatives world and can be a useful tool in hedging against price fluctuations. A forward contract (or simply a ‘forward’) is an agreement between two parties to buy or sell an underlying asset at a specified price on a given future date (or the expiration date). The party that will buy the underlying is said to be taking a long position while the party that will sell the asset takes a short position.

The underlying assets for forwards can range from commodities and currencies to various stocks.

Forwards are customized contracts i.e., they can be tailored according to the underlying asset, the quantity and the expiry date of the contract. Forwards are traded over-the-counter (OTC) unlike futures which are traded on centralized exchanges. The contracts are settled on the expiration date with the buyer paying the delivery price (the price agreed upon in the forward contract for the transaction by the parties involved) and the seller delivering the agreed upon quantity of underlying assets in the contract. Unlike option contracts, the parties in forwards are obligated to buy or sell the underlying asset upon the maturity date depending on the position they hold. Generally, there is no upfront cost or premium to be paid when a party enters a forward contract as the payoff is symmetric between the buyer and the seller.

Terminology used for forward contracts

A forward contract includes the following terms:

Underlying asset

A forward contract is a type of a derivative contract. It includes an underlying asset which can be an equity, index, commodity or a foreign currency.

Spot price

A spot price is the market price of the asset when the contract is entered into.

Forward price

A forward price is the agreed upon forward price of the underlying asset when the contract matures.

Maturity date

The maturity date is the date on which the counterparties settle the terms of the contract and the contract essentially expires.

Forward Price vs Spot Price

Forward and spot prices are two essential jargons in the forward market. While the strict definitions of both terms differ in different markets, the basic reference is the same: the spot price (or rate according to the underlying) is the current price of any financial instrument being traded immediately or ‘on the spot’ while the forward price is the price of the instrument at some time in the future, essentially the settlement price if it is traded at a predetermined date in the future. For example, in currency markets, the spot rate would refer to the immediate exchange rate for any currency pair while the forward rate would refer to a future exchange rate agreed upon in forward contracts.

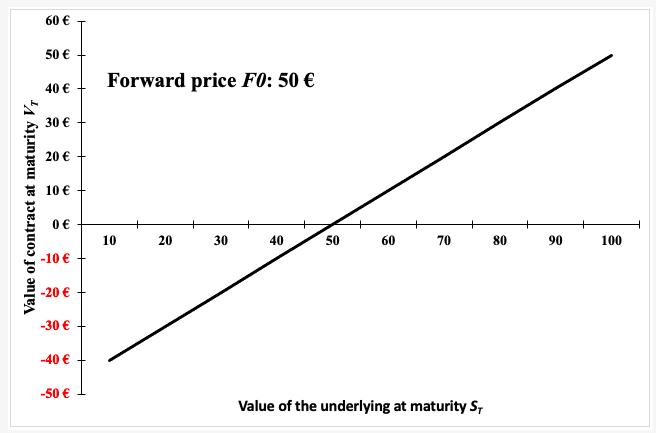

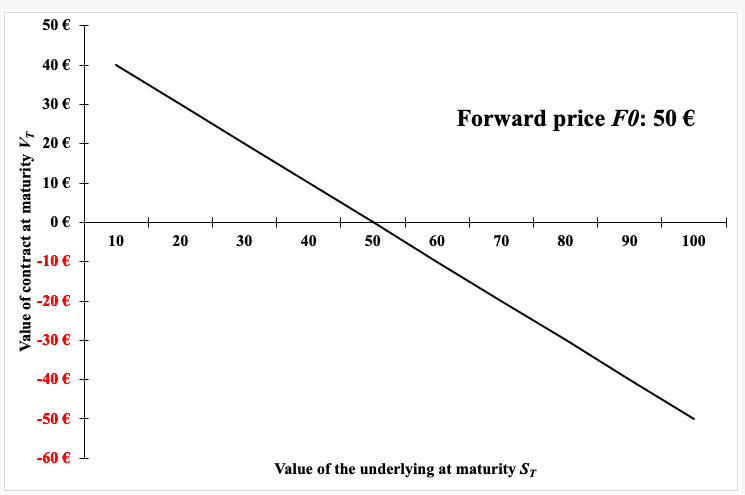

Payoff of a forward contract

The payoff of a forward contract depends on the forward price (F0) and the spot price (ST) at the time of maturity.

Pay-off for a long position

Pay-off for a short position

With the following notations:

N: Quantity of the underlying assets

ST = Price of the underlying asset at time T

F0 = Forward price at time 0

For example, an investor can enter a forward contract to buy an Apple stock at a forward price of $110 with a maturity date in one month.

If at the maturity date, the spot price of Apple stock is $120, the investor with a long position will gain $10 from the forward contract by buying Apple stock for $110 with a market price of $120. The investor with a short position will lose $10 from the forward contract by selling the apple stock at $110 while the market price of $120.

Figure 1. Payoff for a long position in a forward contract

Payoff for a short position in a forward contract

Use of forward contracts

Forward contracts can be used as a means of hedging or speculation.

Hedging

Traders can be certain of the price at which they will buy or sell the asset. This locked price can prove to be significant especially in industries that frequently experience volatility in prices. Forwards are very commonly used to hedge against exchange rates risk with most banks employing both spot and forward foreign exchange-traders. In a forward currency contract, the buyer hopes the currency to appreciate, while the seller expects the currency to depreciate in the future.

Speculation

Forward contracts can also be used for speculative purposes though it is less common than as forwards are created by two parties and not available for trading on centralized exchanges. If a speculator believes that the future spot price of an asset will be greater than the forward price today, she/he may enter into a long forward position and thus if the viewpoint is correct and the future spot price is greater than the agreed-upon contract price, she/he will gain profits.

Risks Involved

Liquidity Risk

A forward contract cannot be cancelled without the agreement of both counterparties nor can it be transferred to a third party. Thus, the forward contract is neither very liquid nor very marketable.

Counterparty risk

Since forward contracts are not traded on exchanges, they involve high counterparty risk. In these contracts, either of the counterparties can fail to meet their obligation resulting in a default.

Regulatory risk

A forward contract is traded over the counter due to which they are not regulated by any authority. This leads to high regulatory risk since it is entered with mutual consent between two or more counterparties.

Related posts in the SimTrade blog

▶ Akshit GUPTA Futures contract

Useful Resources

Hull J.C. (2015) Options, Futures, and Other Derivatives, Ninth Edition, Chapter 1 – Introduction, 23-43.

Hull J.C. (2015) Options, Futures, and Other Derivatives, Ninth Edition, Chapter 5 – Determination of forward and futures prices, 126-152.

About the author

Article written in June 2021 by Akshit GUPTA (ESSEC Business School, Grande Ecole Program – Master in Management, 2019-2022).