In this article, Youssef LOURAOUI (ESSEC Business School, Global Bachelor of Business Administration, 2017-2021) presents the quality factor, which is based on a risk factor that aims to get exposure to businesses with long-term business plans and competitive advantages.

This article is structured as follows: we begin by defining the quality factor and reviewing academic studies. The MSCI Quality Factor Index, which is well used as a benchmark in the asset management industry, is next presented in terms of performance and risk-return trade-off. We showcase the ETF market for investors looking to profit from the quality factor.

Definition

In the world of investing, a factor is any characteristic that helps explain an asset’s long-term risk and return performance. In the late 1970s, the portfolio management industry’s objective was to capture the market return on a portfolio. As a result of Markowitz and Tobin’s earlier research, William Sharpe, John Lintner, and Jan Mossin independently developed the Capital Asset Pricing Model (CAPM). Because it enabled investors to properly value assets in terms of systematic risk, the CAPM was a significant evolutionary step forward in the theory of capital market equilibrium (Mangram, 2013).

Eugene Fama and Kenneth French, following the CAPM’s original work, developed the Fama-French Three-Factor model in 1993 to solve the CAPM’s inadequacies. It claims that, in addition to the market risk component of the CAPM, two other factors have an effect on the returns on securities and portfolios: market capitalization (called the “size” factor) and the book-to-market ratio (referred to as the “value” factor). Other factor characteristics were developed to capture some additional performance as financial research advanced and significant contributions were made.

The quality factor is based on a risk factor that aims to get exposure to businesses with long-term business plans and competitive advantages. It can also be defined as the attributes for which investors are prepared to pay a premium (Hsu et al., 2019).

Academic research

The long-term outperformance of the quality factor over the market is well documented in the financial literature. Eugene Fama and Kenneth French added two quality-related components to their distinctive three-factor model (firm size, business value, and market risk): profitability and asset growth. Numerous active strategies have prioritized quality growth in their premium selection and portfolio construction processes. In 2012, Robert Novy-Marx published an essay proving that profitability and stability were just as useful as traditional value measures for assessing returns (MSCI Factor research, 2021).

Asness et al. (2018) propose a valuation model that illustrates how stock prices should increase if qualitative qualities such as profitability, growth, and safety improve. They demonstrate experimentally that high-quality stocks do fetch a premium on average, but not by a huge margin (Asness et al., 2018). Perhaps as a result of this perplexingly little influence of quality on price, high-quality stocks provide appealing risk-adjusted returns. Indeed, in the United States and 24 other countries, a factor that invests in high-quality companies and shorts low-quality companies generates significant risk-adjusted returns. The price of quality fluctuates throughout time, reaching a low point during the internet bubble, and a low price of quality suggests that QMJ will give a high rate of return in the future. Analysts’ price targets and earnings predictions indicate that systemic errors in return and earnings expectations are occurring as a result of quality issues (Asness et al., 2018).

MSCI Quality Factor Index

MSCI Factor Indexes are rule-based, transparent indexes that target equities with favorable factor qualities, as determined by academic discoveries and empirical outcomes, and are designed for easy implementation, replicability, and usage in both standard indexed and active portfolios. The MSCI Quality Factor Index measures the quality factor using three fundamental variables (MSCI Factor research, 2021) :

- Return on equity – a measure of a company in generating profits

- Debt to equity – a measure of a company’s leverage

- Earnings variability – a measure of how smooth earnings growth has been.

Quality is a “defensive” component, which means that it has historically benefited during periods of economic recession (MSCI Factor research, 2021). The quality factor has aided in explaining the performance of equities with low debt, steady profits, and a high profit margin.

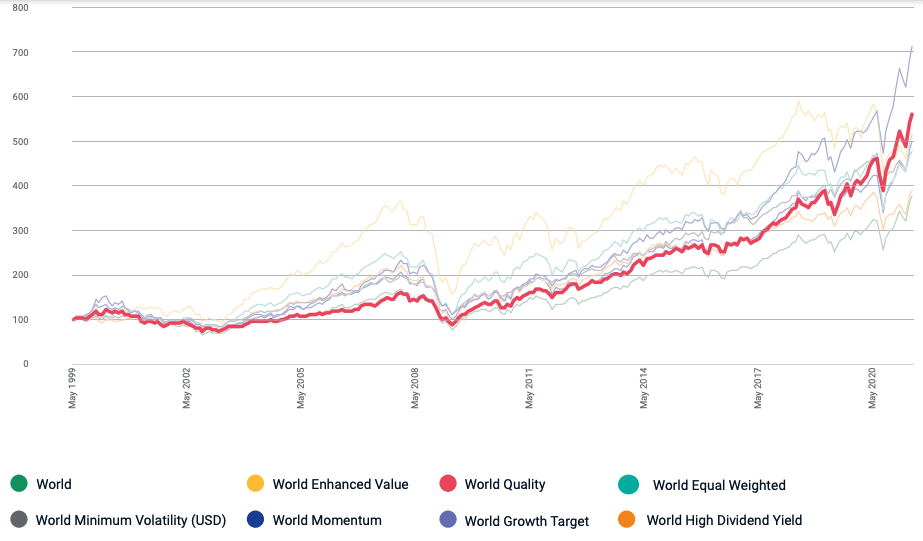

Performance of the MSCI Quality Factor Index from

Figure 1 compares the MSCI Quality Factor Index’s performance to those of other factors from May 1999 to May 2020. All indices are rebalanced on a 100-point scale to ensure consistency in performance and to facilitate factor comparisons

Figure 1. Performance of the MSCI Quality Factor Index from 1999-2020.

Source: MSCI Factor research (2021).

The MSCI Quality Factor Index has traditionally outperformed the MSCI World Index in the long term, with a 1.98 percent annual return over the MSCI World Index since 1999, as seen below (MSCI Factor research, 2021).

Risk-return profile of MSCI Quality Factor Index

Figure 2 shows the MSCI Quality Factor Index compared to other factors over the period May 1999 – May 2020 in terms of risk/reward. The risk-return trade-off states that the potential return rises with an increase in risk. Individuals connect low levels of uncertainty about future returns with low potential returns, while high levels of uncertainty or risk are associated with large potential returns. According to the risk-return trade-off, an investor’s money can generate higher returns only if the investor is willing to endure a higher risk of loss as shown in Figure 2.

Figure 2. Risk-return profile of MSCI Yield Factor Index compared to a peer group.

Source: MSCI Factor research (2021).

Behavior of the MSCI Quality Factor Index during the Covid-19 crisis

The Covid-19 crisis has not only caused significant social and economic suffering, but it had also an impact on financial markets. To study the behavior of the factors during the Covid-19 crisis, we compute the return of the MSCI Factor indexes during the different stages of the crisis. The MSCI Factor indexes are: value, size, quality, momentum and minimum volatility. Following Pagano et al. (2020) and Hasaj and Sherer (2021), we decompose the Covid-19 crisis into five stages: origin, incubation, outbreak, fever, and treatment. Each stage is described below.

- Origin (01/11/2019 – 01/01/2020): the first instances are reported in Wuhan, China.

- Incubation (02/01/2020 – 17/01/2020): during this phase, the number of patients began to rise at a faster rate, raising concerns about the disease’s severity.

- Outbreak (20/01/2020 – 21/02/2020): the number of cases rose to the point that the World Health Organization (WHO) decided that this illness may pose a major threat to the world’s population, and the pandemic was proclaimed.

- Fever (24/02/2020 – 20/03/2020): markets are extremely volatile, owing to government restrictions aimed at flattening the infection curve, with the decision to impose a lockdown in numerous nations as the most notable measures, among others.

- Treatment (23/03/2020 – 15/04/2020): most of this turnaround occurs between March and June 2020, which corresponds with the start of good news about the discovery and widespread use of the vaccine.

Table 1 gives the performance of the MSCI factor indexes during the different stages of the Covid-19 crisis. Performance is measured by the return computed on the time-period of each stage, and then annualized for comparison across the different stages. We use data are from Thomson Reuters.

Table 1. Performance of the MSCI factor indexes during the Covid-19 crisis.

Source: computation by the author. Data source: Thomson Reuters.

A conclusive statement can be made based on our analysis. The quality component was the strongest performer throughout the COVID crisis’s inception in late 2020 and during the fever phase, when severe limitations were implemented, resulting in a collapsing market.

ETFs to capture the Quality factor

Let us recall that an Exchange-Traded Fund (ETF) is an investment vehicle that seeks to mirror the performance of a benchmark like an equity index and is traded on a continuous basis during the day like stocks. By investing in ETFs, an investor gains access to a plethora of diversification options through several asset classes (equity, bonds, currency, commodity, real estate, etc.).

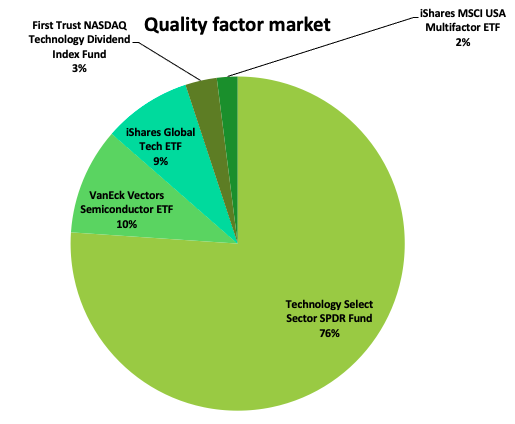

Figure 3 illustrates the overall ETF distribution of the major providers of quality factor ETFs in terms of percentage of asset under management. By examining the market overview for quality factor investments, we can observe SPDR dominance in this factor investing market, with 76.07%, representing more than three quarters of the overall quality factor ETF market.

Figure 3. Quality factor ETF market.

Source: etf.com (2021).

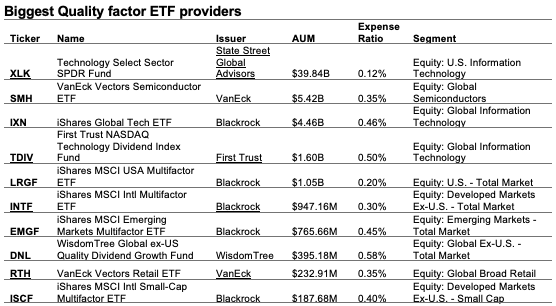

Table 2 gives more detailed information about the biggest quality factor ETF providers: the asset under management (AUM), expense ratio (ER) and the segment for the investments.

Table 2. Ranking of the biggest Quality ETF providers.

Source: etf.com (2021).

Why should I be interested in this post?

If you are an undergraduate or graduate student at a business school or university, you may have encountered the CAPM in your 101 finance course. This post raises awareness of the presence of another market-priced risk factor.

If you are an investor, you may wish to consider increasing your exposure to the quality factor in order to boost your portfolio’s total return.

Related posts on the SimTrade blog

▶ Youssef LOURAOUI Minimum Volatility

▶ Youssef LOURAOUI Value Factor

▶ Youssef LOURAOUI Yield Factor

▶ Youssef LOURAOUI Momentum Factor

▶ Youssef LOURAOUI Size Factor

▶ Youssef LOURAOUI Growth Factor

Useful resources

Academic research

Clifford S. Asness & Andrea Frazzini & Lasse Heje Pedersen, 2019. “Quality minus junk,” Review of Accounting Studies, 24(1): 34-112.

Hasaj, M., Sherer, B., 2021. Covid-19 and Smart-Beta: A Case Study on the Role of Sectors. EDHEC-Risk Institute Working paper, 1-35.

Mangram, M.E., 2013. A simplified perspective of the Markowitz Portfolio Theory. Global Journal of Business Research, 7(1): 59-70.

Pagano, M., Wagner, C., Zechner, J., 2020. Disaster Resilience and Asset Prices, Working paper.

Business analysis

etf.com, 2021. Biggest Quality ETF providers.

MSCI Investment Research, 2021. Factor Focus: Quality.

About the author

The article was written in September 2021 by Youssef LOURAOUI (ESSEC Business School, Global Bachelor of Business Administration, 2017-2021).

9 thoughts on “Quality Factor”

Comments are closed.