In this article, Raphaël ROERO DE CORTANZE (ESSEC Business School, Grande Ecole Program – Master in Management, 2019-2022) explains how credit rating agencies work.

What are Credit Rating Agencies?

Credit Rating Agencies are private companies whose main activity is to evaluate the capacity of debt issuers to meet their financial commitments. The historical agencies (Moody’s, Standard & Poor’s and Fitch Ratings) hold about 85% of the market. But national competitors have emerged over the years, such as Dagong Global Credit Rating in China. Nonetheless, there is little competition in this market as the barriers to entry are very high. The rating agencies’ business model is based on remuneration paid by the rated entities, consulting activities, and the dissemination of rating-related data.

The rating gives an opinion (in the form of a grade) on the ability of an issuer to meet its obligations to its creditors, or of a security to generate the capital and interest payments in accordance with the planned schedule. The rated entities are therefore potentially all financial or non-financial agents issuing debt: governments, public or semi-public bodies, financial institutions, non-financial companies. The rating may also relate not to an issuer in general, but to a security.

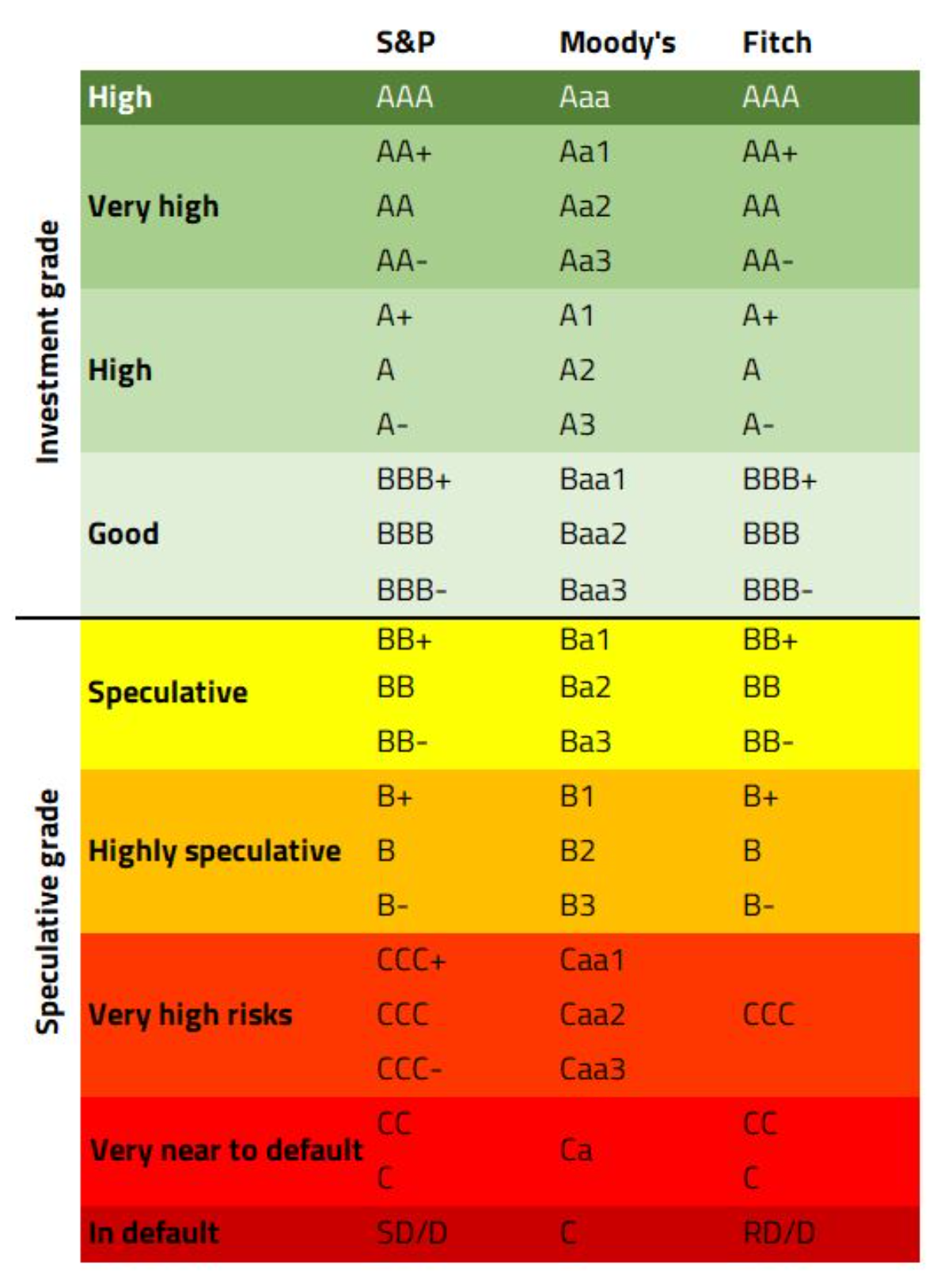

S&P, Moody’s, and Fitch rating scales

Source: internet.

Rating agencies are key players in the markets. Indeed, ratings are widely used in the regulatory framework on the one hand, and also in the strategies of many investors. For instance, to be eligible for central bank refinancing operations, securities must have a minimum rating. Similarly, the management objectives of many investors are based on ratings: for example, a mutual fund may have as one of its objectives to hold 80% of assets issued by issuers rated at least “BBB”. Credit risk monitoring indicators in corporate and investment banks are also based on ratings.

Credit Rating Agencies: judges & parties during the subprime crisis?

Rating agencies played a crucial role in securitization (“titrisation” in French), a financial technique that transforms rather illiquid assets, such as real-estate loans, into easily tradable securities. The agencies rate both the securitized credit packages and the bonds issued as counterparts according to the different risk levels.

The securitization technique appeared in the 70’ in the US, and allowed banks to grant more loans. During the 1990’ and 2000’, banks used securitization as a way to remove from their balance sheet the loans they granted. Indeed, banks would package loans in vehicles labelled as “Asset Backed Securities” (securities which the collateral is an asset). Banks would then sell these securities, or sell the risk associated with these securities. In the case of subprimes, the loans were packaged inside vehicles called “Mortgage Backed Securities”, as these securities had as counterpart the mortgage loans. There was a shift from the previous “originate-to-hold” bank model (where banks originated the loans and kept them in their balance sheet) to the new “originate-to-distribute” model (where banks originated the loans and then took them out of their balance sheet).

Michel Aglietta explains that in the case of securitized loans (such as MBS), the rating agencies rate and are at the same time stakeholders in the securitization. Indeed, the constitution of the product and the rating are completely intertwined. “Without the rating, the security has no existence”. The investment banks that structure and market the product and the agencies work together to determine the specificities of each loan packages or “pools” and obtain the desired rating.

It is now recognized that rating agencies often overrated the securitized packages compared to the intrinsic risk they were carrying. By granting high grades to many securitized packages (the highest being AAA), they have contributed to the formation of a speculative bubble. In addition, when the housing market collapsed, the rating agencies reacted too late and downgraded MBS abruptly, which inevitably worsened the crisis. For example, 93% of the MBS rated AAA marketed in 2006 had their grade scaled down to “junk bond” ratings (BB+/Ba1 and below) later on.

Rating agencies have been accused of conflict of interest, as they are paid by those they rate. The emails revealed by the US Senate Investigations Subcommittee in April 2010 during its work on the Goldman Sachs affair reveal a system in which the marketing teams of structured products of investment banks tended to choose the agency most inclined to give the most favorable rating. Furthermore, the Senate subcommittee found that rating decisions were often subject to concerns about losing market share to competitors.

Key concepts

Mortgage loan

A mortgage loan has the specificity of putting the purchase property (a house for instance) as the counterpart of a loan. In the case of a payment default, the property is seized.

Related posts on the SimTrade blog

▶ Jayati WALIA Quantitative Risk Management

▶ Jayati WALIA Credit risk

▶ Georges WAUBERT Credit analyst

▶ Jayati WALIA My experience as a credit analyst at Amundi Asset Management

Useful resources

La Finance pour Tous

Aglietta M. (2009) La crise : Pourquoi en est arrivé là ? Michalon Editions.

Ministère de l’Economie et des Finances Quel rôle ont joué les agences de notation dans la crise des subprimes ?

Marian Wang (2010) Banks Pressured Credit Agencies, Then Blamed Them Later on Blog.

About the author

Article written in May 2021 by Raphaël ROERO DE CORTANZE (ESSEC Business School, Master in Management, 2019-2022).