In this article, Bochen LIU (Queen’s Smith School of Business, BCom 2023–2027; ESSEC BBA Exchange Program, Fall 2025) explains the concept of the order book, how it functions in financial markets, and the insights it provides to traders.

What is an order book?

For anyone engaging in financial markets, understanding the order book is essential. The order book is a dynamic record of buy and sell orders for a given asset, reflecting the interaction between supply and demand in real time. Whether trading stocks, currencies, or digital assets, the order book allows market participants to visualize liquidity, identify potential price movements, and make informed decisions.

An order book lists all outstanding buy and sell limit orders for an asset, showing both the prices at which traders are willing to transact and the quantities they wish to trade. It provides a clear picture of market depth and the relative interest of buyers and sellers at different price levels. Unlike a simple price chart, the order book reveals where liquidity is concentrated and where potential support or resistance may occur, making it an indispensable tool for understanding short-term market dynamics.

How an order book functions

The order book is typically divided into two sections: the buy side (bid side) and the sell side (ask side). The buy side shows the highest prices buyers are willing to pay, while the sell side reflects the lowest prices sellers are willing to accept. Orders are listed by price and aggregated volume, and the book is continuously updated as trades are executed and new orders enter the market.

The difference between the best bid and best ask is known as the bid-ask spread, a key indicator of market liquidity. By monitoring changes in the spread and the distribution of orders, traders can gain insights into market sentiment and anticipate short-term price movements.

In practice, the organization of the order book allows traders to understand not just current prices but also the pressure from buyers and sellers at different levels. For example, a concentration of large buy orders may act as a support level, while clusters of sell orders can indicate resistance. The order book therefore acts as a living map of market intentions and is often used together with charts and other data sources.

Order book representation

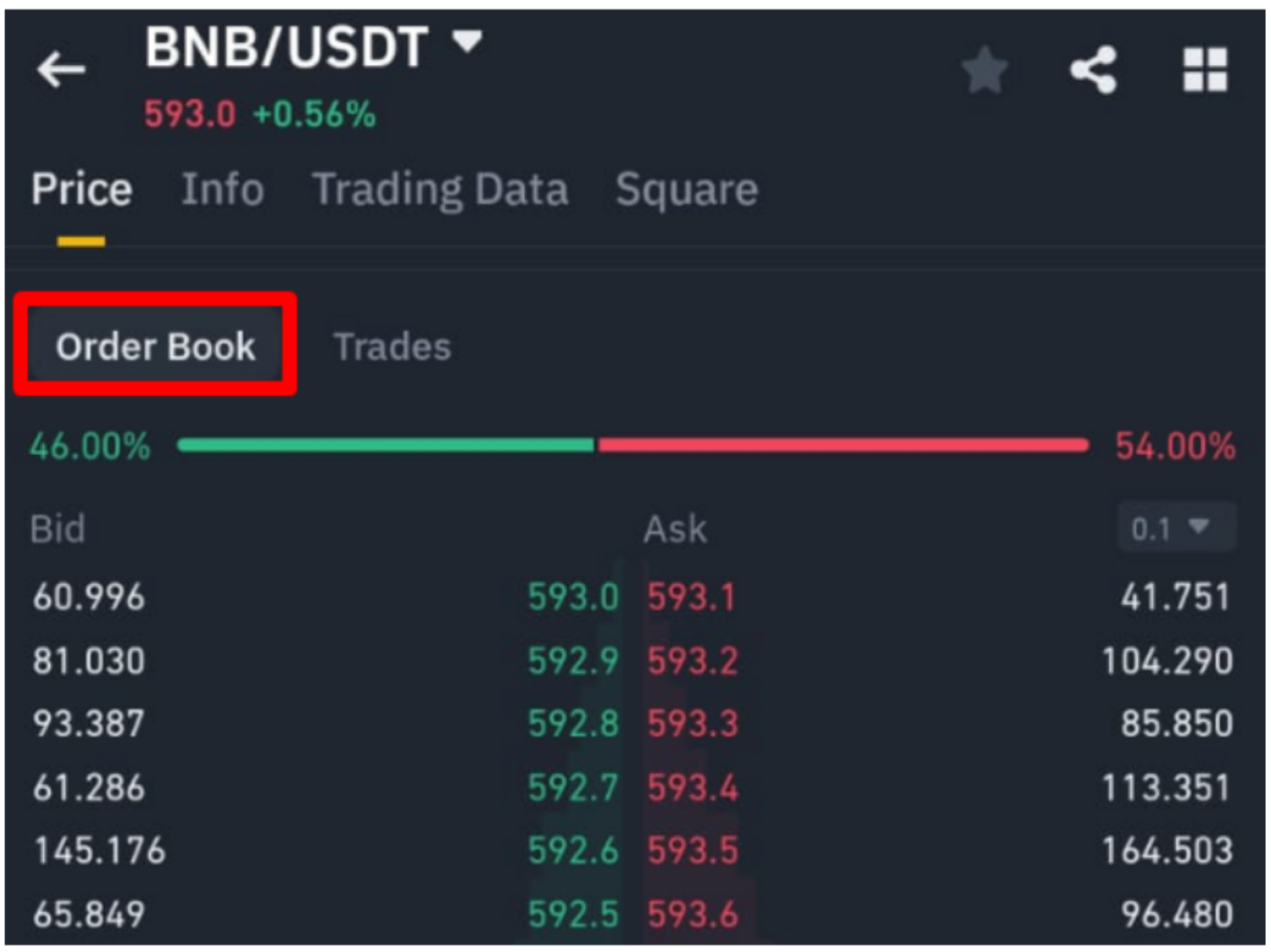

The structure of the order book is often visualized through trading platforms that display the distribution of buy and sell orders at different price levels. A typical representation includes two columns: bids on the left and asks on the right. Each row shows the price level and the cumulative quantity available at that level.

Figure 1. Example of an order book (buy and sell parts presented side by side).

Source: screenshot from a trading platform.

Figure 1 presents one of the most common visual formats of the order book, in which bid orders are shown on the left and ask orders on the right. This side-by-side structure allows traders to compare the quantities available at different price levels and to identify the best bid and best ask immediately. It also makes the bid-ask spread visible, which is a key indicator of market liquidity and transaction cost.

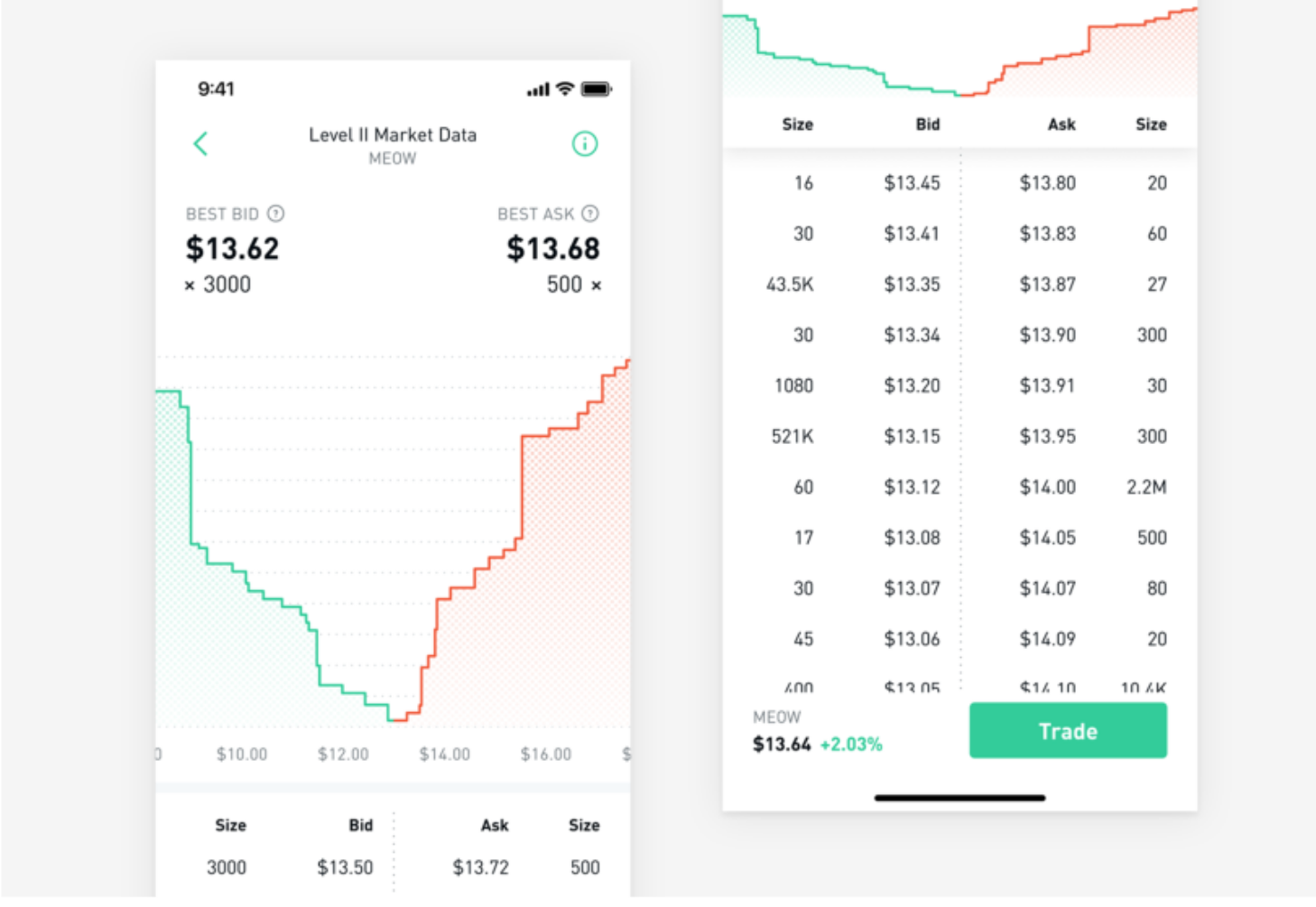

Modern electronic trading platforms such as NASDAQ TotalView or cryptocurrency exchanges provide graphical representations of the order book. These interfaces often include a “depth chart,” where the cumulative buy and sell volumes are plotted against price levels. Such visualizations allow traders to quickly observe supply and demand imbalances.

Figure 2. Example of an order book (depth chart representation).

Source: screenshot from a trading platform.

Figure 2 shows the order book in a format that combines tabular bid-ask information with a depth chart. The green area represents cumulative buy-side liquidity, while the red area represents cumulative sell-side liquidity. This representation helps traders visualize how orders are distributed across price levels and where supply-demand imbalances may emerge in the market.

Evolution of the order book

The order book constantly evolves as new orders arrive, existing orders are cancelled, and trades are executed. Two main types of orders influence this evolution: limit orders and market orders.

Limit orders add liquidity to the market by specifying both a price and quantity at which a trader is willing to buy or sell. When a trader places a buy limit order below the current market price or a sell limit order above it, the order enters the order book and waits to be matched.

Market orders, in contrast, remove liquidity. A market buy order immediately matches with the lowest available sell orders, while a market sell order matches with the highest available buy orders. As these trades execute, they reduce the quantities available in the order book and may shift the best bid and ask prices.

The interaction between incoming limit orders and market orders continuously reshapes the order book and drives short-term price movements.

Order priority rules

Electronic markets generally follow two key priority rules when matching orders: price priority and time priority.

Price priority means that orders offering better prices are executed first. For example, among buy orders, the highest bid has priority, while among sell orders the lowest ask has priority.

If multiple orders are placed at the same price level, time priority applies. The order that was submitted earlier will be executed before later orders. This rule encourages traders to submit orders quickly if they want to secure execution.

These priority mechanisms ensure fairness and transparency in electronic trading systems.

Price impact and transaction prices

The execution of orders can influence market prices, a phenomenon known as price impact. When large market orders consume multiple levels of liquidity in the order book, the transaction price may move significantly.

For example, if a large buy market order exceeds the quantity available at the best ask price, the trade will continue matching with higher ask prices. This process pushes the transaction price upward and illustrates how large orders can move markets.

Transaction prices and traded volumes therefore provide important information about market activity. High trading volumes often indicate strong participation and may reinforce price trends.

Liquidity characteristics of the order book

The order book provides several indicators that help measure market liquidity.

Bid-ask spread is the difference between the best bid and best ask price. A narrow spread typically indicates a liquid market with low transaction costs.

Market depth refers to the total quantity of buy and sell orders available at different price levels. A deep order book allows large trades to be executed without significantly affecting prices.

Market breadth describes how widely orders are distributed across price levels. A broad distribution indicates active participation from many traders.

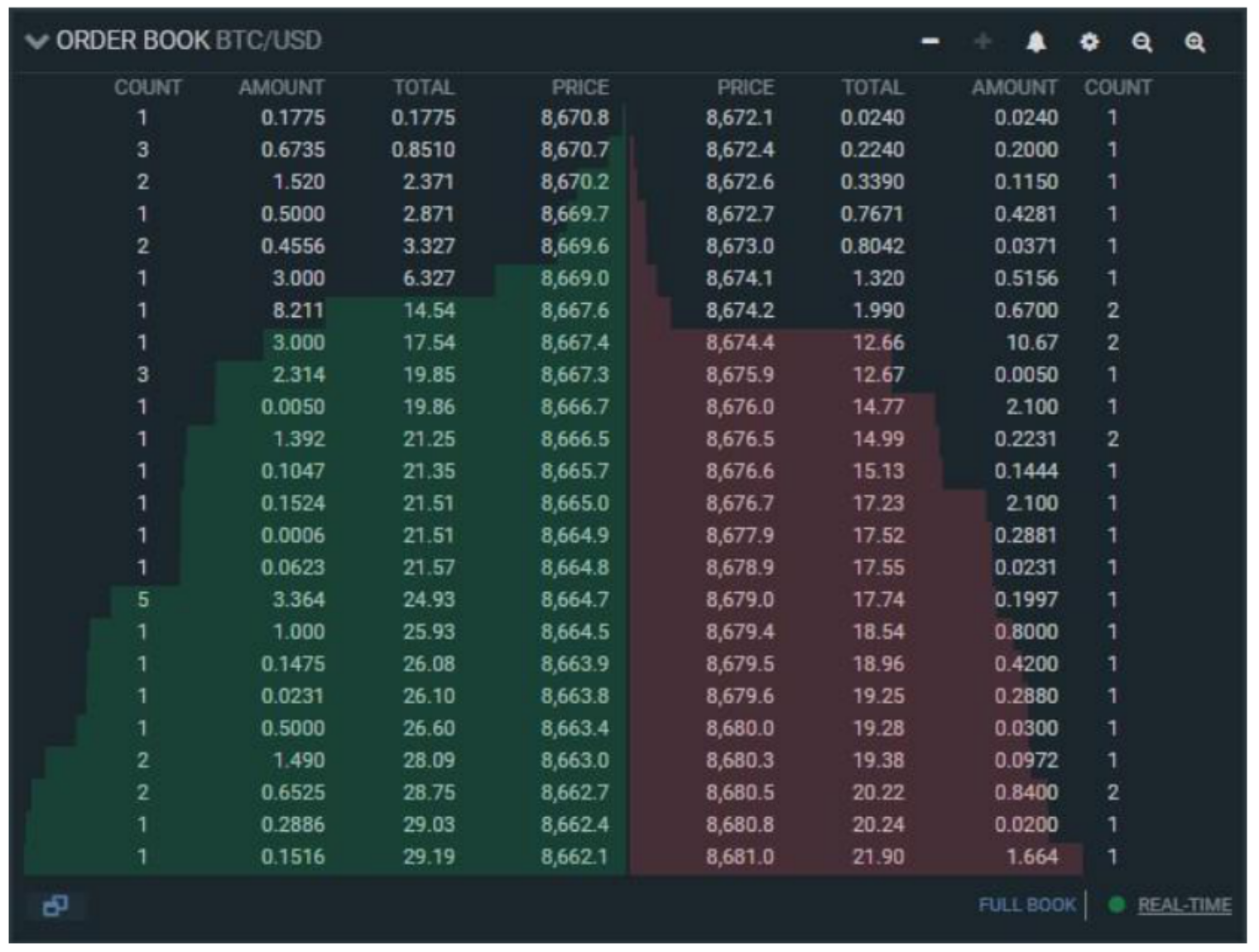

Figure 3. Example of an order book (used to assess liquidity).

Source: screenshot from a trading platform.

Figure 3 provides a mobile-style visualization of the order book, showing the best bid, the best ask, and the quantities available on both sides of the market. It is particularly useful for illustrating liquidity measures such as bid-ask spread, visible depth, and market breadth. By comparing the quoted quantities at different prices, traders can better evaluate the strength of buying and selling pressure.

Resilience measures how quickly the order book replenishes after large trades remove liquidity. A resilient market quickly attracts new orders and stabilizes prices.

These liquidity measures help traders evaluate the quality and stability of a market.

Why should I be interested in this post?

For ESSEC students interested in business and finance, understanding the order book is fundamental to analyzing financial markets and trading behavior. It provides practical insight into how prices are formed, how liquidity affects execution, and how real-time data informs strategic decisions.

Mastering order book analysis strengthens financial reasoning, improves understanding of market microstructure, and supports more informed investment or trading strategies. This knowledge is directly relevant for careers in finance, trading, investment analysis, and quantitative research.

Related posts on the SimTrade blog

▶ Federico DE ROSSI Understanding the Order Book: How It Impacts Trading

▶ Jayna MELWANI The impact of market orders on market liquidity

▶ Lokendra RATHORE Good-til-Cancelled (GTC) order and Immediate-or-Cancel (IOC) order

▶ Clara PINTO High-frequency trading and limit orders

Useful resources

SimTrade course — Trade orders

SimTrade course — Market making

SimTrade simulation — Market orders

SimTrade simulation — Limit orders

About the author

The article was written in April 2026 by Bochen LIU (Queen’s Smith School of Business, BCom 2023–2027; ESSEC BBA Exchange Program, Fall 2025).

▶ Discover all posts by Bochen LIU