Top financial innovations in the 20th century

In this article, Nithisha CHALLA (ESSEC Business School, Grande Ecole Program – Master in Management (MiM), 2021-2024) presents top financial innovations of the 20th century that have brought significant changes in people’s life.

Introduction

Financial innovations have significantly transformed how people make transactions and manage money like saving and investing. These innovations have increased accessibility, convenience, and security in financial activities, benefiting individuals and companies alike. From the introduction of paper money in ancient China to modern-day digital banking, each era has brought new ways to manage finances. The 20th century has seen rapid advancements due to technology, leading to groundbreaking changes in financial services.

Top Financial Innovations that Changed People’s Life in the 20th century

Our selection of financial innovations is based on their wide adoption by firms and individuals (usage in many countries worldwide).

- Credit Cards and Debit Cards: Introduced in the 1950s, credit and debit cards provided a convenient way for consumers to make purchases without cash, leading to a shift towards a cashless society.

- Automated Teller Machines (ATMs): ATMs revolutionized banking by allowing customers to perform transactions anytime, anywhere, without needing to visit a bank branch.

- Telephone Banking: The rise of the internet in the 1980s enabled banks to allow customers to perform basic banking transactions, such as checking account balances and transferring funds, via phone.

- Online Banking: The rise of the internet in the 1990s enabled banks to offer online services, making it easier for customers to manage accounts, pay bills, and transfer money.

We explain below how these financial innovations impacted people’s lives and companies. We also give some statistics to measure the impact.

Credit Cards and Debit Cards

The Diners Club card, introduced by Frank McNamara card in 1950, is considered the first credit. Later, Bank of America launched the BankAmericard (now Visa) in 1958. Later, Visa became one of the largest credit card issuers globally. MasterCard, originally Interbank Card Association, formed in 1966, is another major player in the credit card industry. The concept of a debit card was first introduced by the First National Bank of Seattle in 1966. The first debit card was issued by Barclays in the UK in 1966.

These Credit and Debit cards provided consumers a convenient and secure way to purchase without carrying cash. It allowed for the development of the credit industry, enabling consumers to borrow funds for purchases and pay them back over time. Which also helped customers make larger purchases thus improving purchasing power.

To speak on how much these innovations affected people, by the end of the 20th century, there were over 1 billion credit cards in use globally. And in 2019, Visa and MasterCard together processed over 171 billion transactions worldwide. In terms of debit card transactions, it recorded over 100 billion debit card transactions globally in 2020.

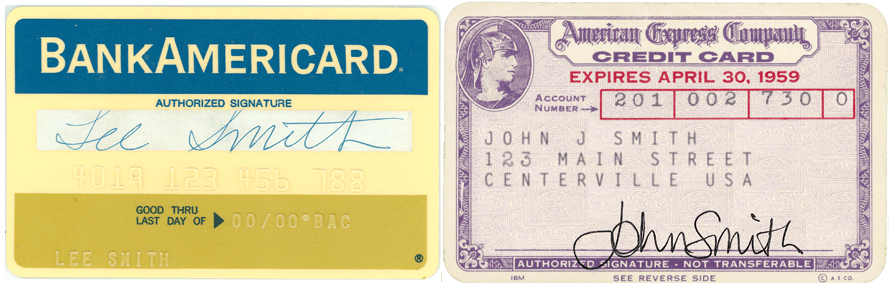

First ever credit card picture

Source: Time news letter

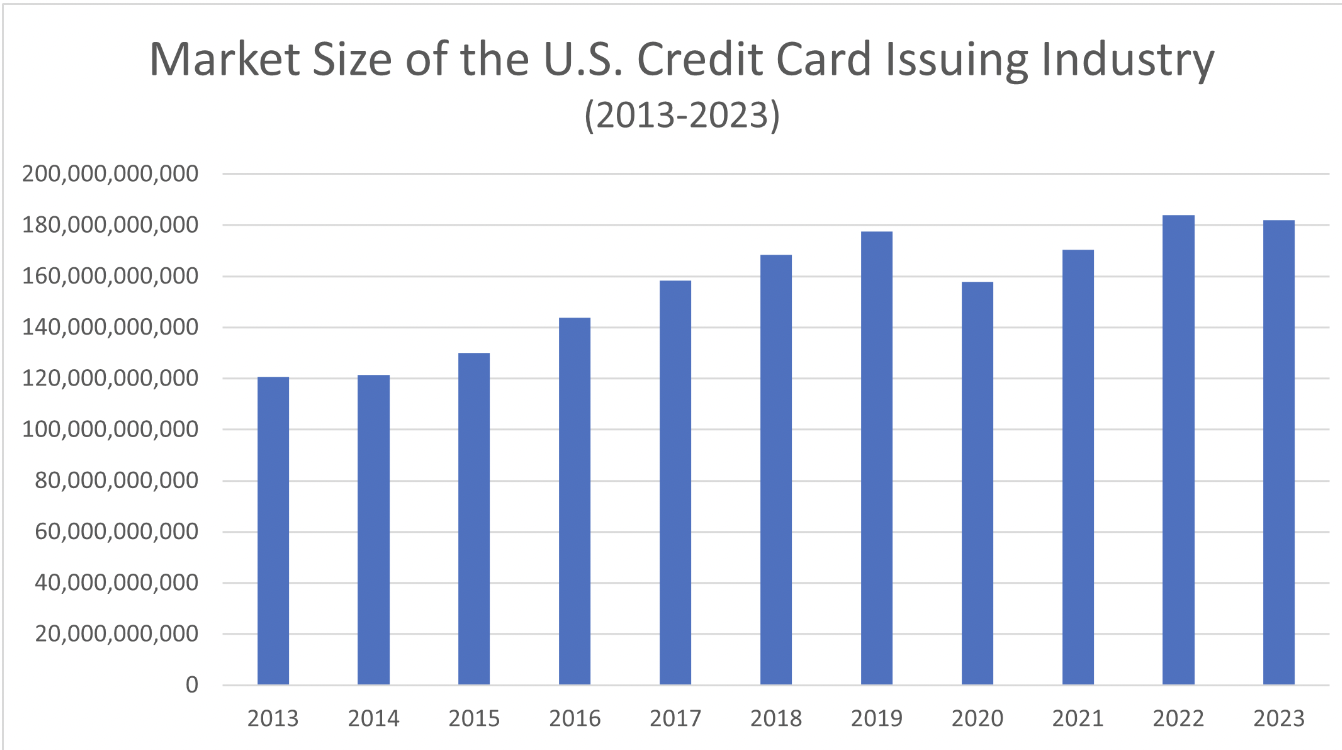

Figure 1 below presents the evolution of the size of the credit card industry in the United States from 2013 to 2023.

Figure 1. The market size of the US credit card industry

Source: Time news letter

Automated Teller Machines (ATMs)

John Shepherd-Barron is credited with inventing the first ATM, which was installed by Barclays Bank in London in 1967. Later, Diebold Nixdorf and NCR Corporation became the major manufacturers of ATMs in the 1980s.

These ATMs provided 24/7 access to banking services, allowing customers to withdraw cash, check balances, and perform other transactions without needing to visit a bank branch. Hence, it enhanced convenience and reduced the need for in-person banking services. Helping reduce queues at banks and improve transaction speed. Overall, this innovation has increased accessibility, convenience, and efficiency both for banks and consumers.

To speak on how much these innovations affected people, by 1990, there were around 100,000 ATMs worldwide. As of 2020, there are approximately 3.2 million ATMs globally. The global ATM market was valued at around $18.4 billion in 2019.

First ever ATM picture

Source: Time news letter

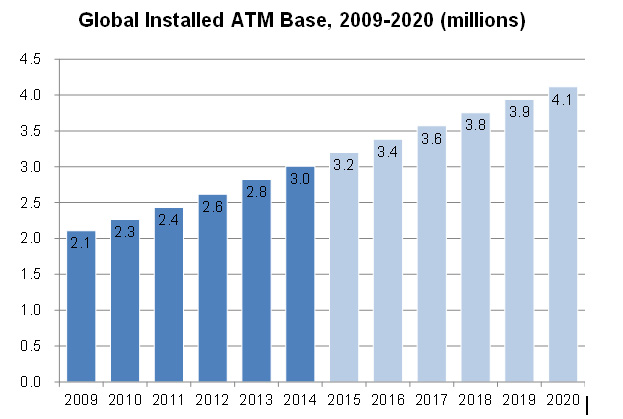

Figure 2 below presents the evolution of the globally installed ATM bases in the period of 2009 to 2020.

Figure 2. ATM global evolution

Source: Time news letter

Telephone Banking

Midland Bank (now part of HSBC) launched the first telephone banking service in the UK in 1989. HSBC pioneered telephone banking services and Citibank also offered telephone banking as part of its service portfolio being one of the early adopters of telephone banking. This is considered the innovation of the 1980-1990 decade.

This innovation has allowed customers to perform basic banking transactions, such as checking account balances and transferring funds, via phone. Provided a convenient alternative to visiting a bank branch, especially for those without internet access, and reduced risks associated with carrying cash or checks.

To speak on how much these innovations affected people, by the late 1990s, telephone banking was widely adopted, with millions of users globally. Despite the rise of online and mobile banking in the 21st century, telephone banking remains a valuable service for many customers, particularly the elderly and those in rural areas. In 2019, an estimated 5% of U.S. adults still used telephone banking. And by 2000, more than 50% of U.S. banks offered telephone banking services.

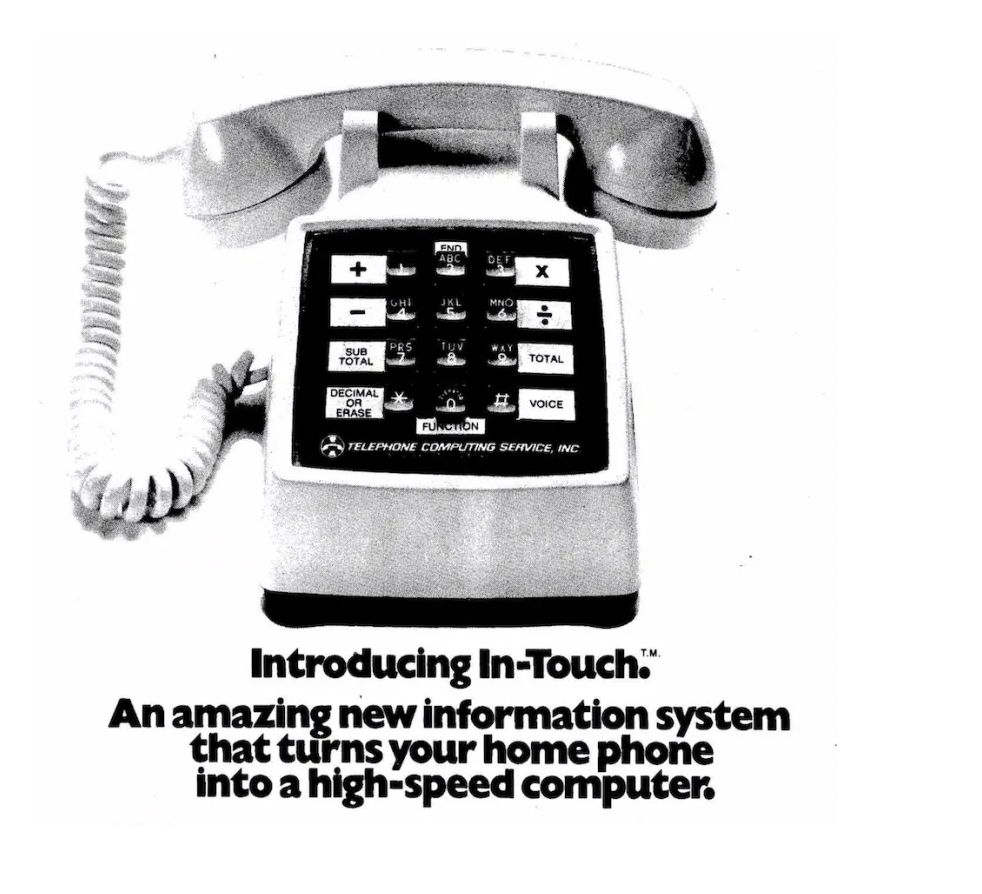

Figure 1 shows what the first-ever telephone banking machine looked like in 1973.

First ever touch-tone telephone banking machine in 1973.

Source: ZB Media

Online Banking

The concept of online baking was developed by banks like Stanford Federal Credit Union, which offered the first online banking services in 1994. Bank of America was one of the early adopters of online banking and Wells Fargo Launched its first Internet banking service in 1995.

This innovation has provided customers with the ability to manage their accounts, pay bills, transfer funds, and perform other banking activities from the comfort of their homes. It reduced the need for physical bank branches and made banking services more accessible.

To speak on how much these innovations affected people, by 2019, 76% of U.S. adults used online banking. The global online banking market was valued at $9.2 billion US dollars in 2019. And global online banking users are expected to reach 2.5 billion by 2024.

First ever Online banking machine in 1980.

Source: Fintech Magazine

Figure 1 shows what the first-ever Online banking machine looked like in 1980.

Conclusion

Financial innovations have profoundly transformed the way individuals and businesses interact with money. From the widespread adoption of credit cards to mobile payments these innovations have made financial services more accessible, efficient, and secure. As technology continues to advance, the financial landscape will undoubtedly see further changes, continuing to shape and improve people’s lives worldwide.

Why should I be interested in this post?

Management students, as future leaders and decision-makers, should understand financial innovations for several compelling reasons. These innovations not only influence the financial landscape but also have significant implications for strategic decision-making, operational efficiency, and competitive advantage.

Related posts on the SimTrade blog

▶ Nithisha CHALLA Top financial innovations in the 21st century

Useful resources

Wikipedia Financial Innovation

Fintech Magazine Online Banking 1973 – History of Computers

ZB Media Technology in Fintech and the story of Online Banking

Research gate The emergence of financial innovation and its governance – a historical literature review

Axis bank Credit card: A cashless surge

Cambridge University Press Banking and Finance in the Twentieth Century

About the author

The article was written in August 2024 by Nithisha CHALLA (ESSEC Business School, Grande Ecole Program – Master in Management (MiM), 2021-2024).