In this article, Cornelius HEINTZE (ESSEC Business School, Global Bachelor in Business Administration (GBBA) – Exchange Student, 2025) explains how the usage of different valuation methods can lead to different outcomes and how to use them.

Why this is important

In finance valuation is always present and it is not only a mechanical exercise. Analysts are working with discounted cash flow models, multiples or other procedures to value a company. Using these different methods will lead to different outcomes and it is crucial to understand why these differences occur and if this is in line with your expectations or differing from them. This helps to avoid misleading conclusions and relying only on a single method or having difficulties interpreting multiple methods.

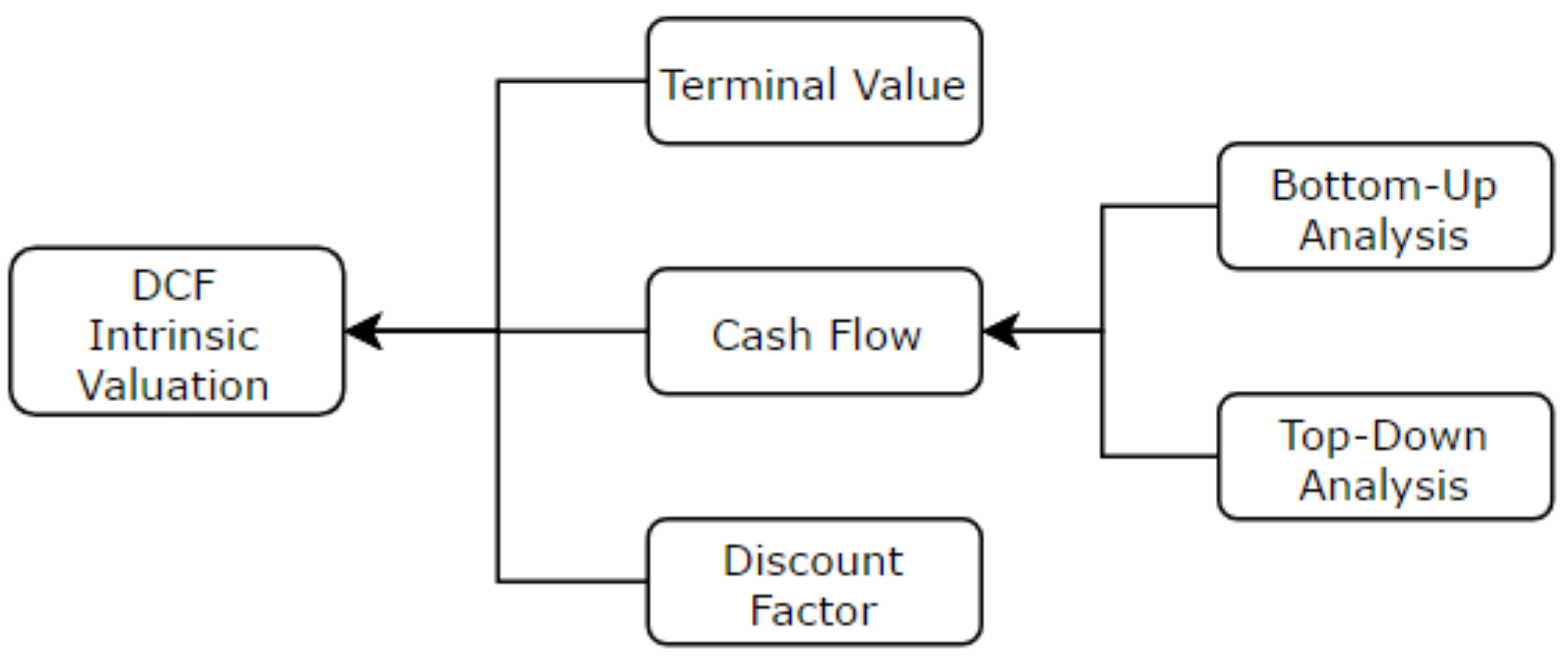

The DCF model: measuring intrinsic value

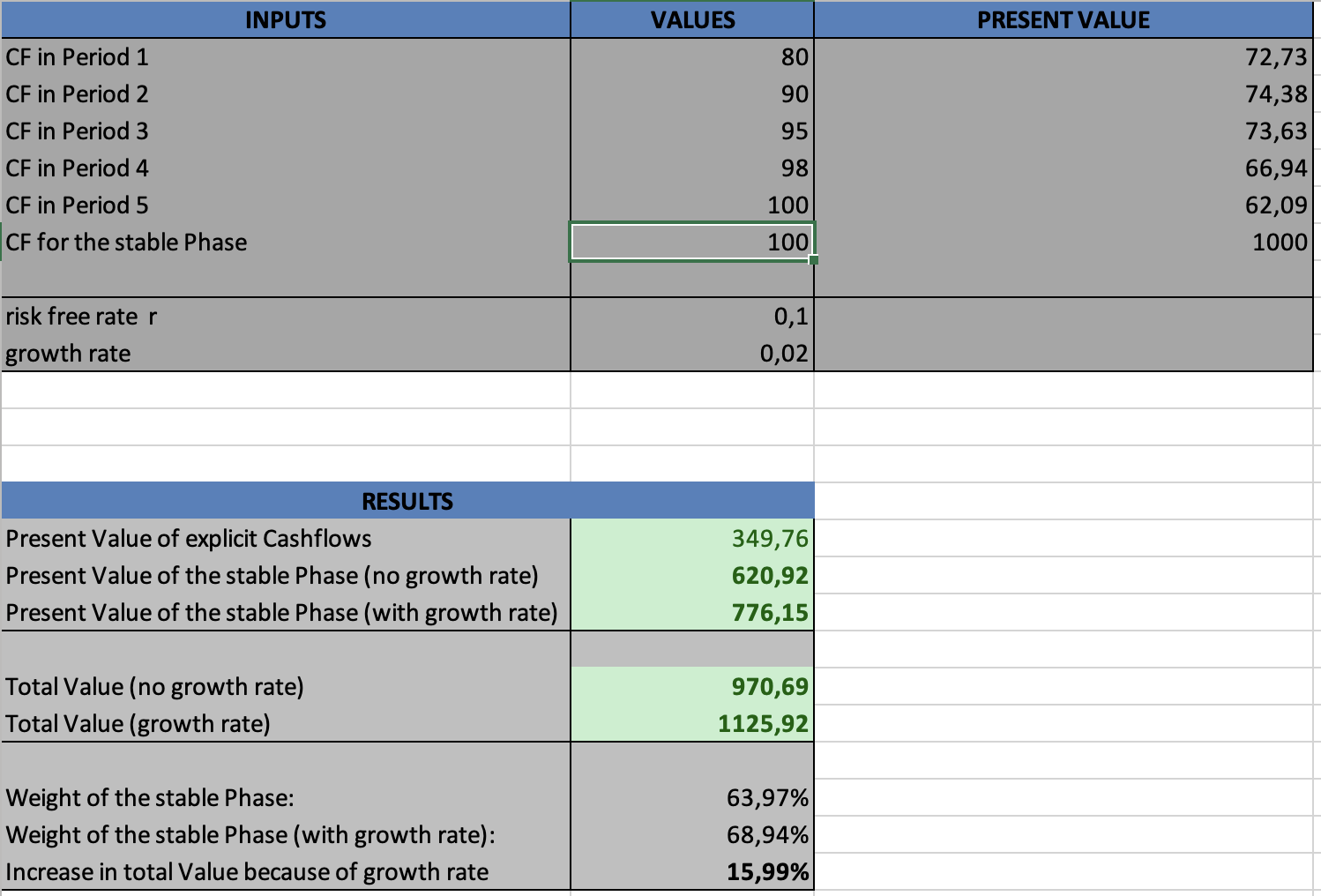

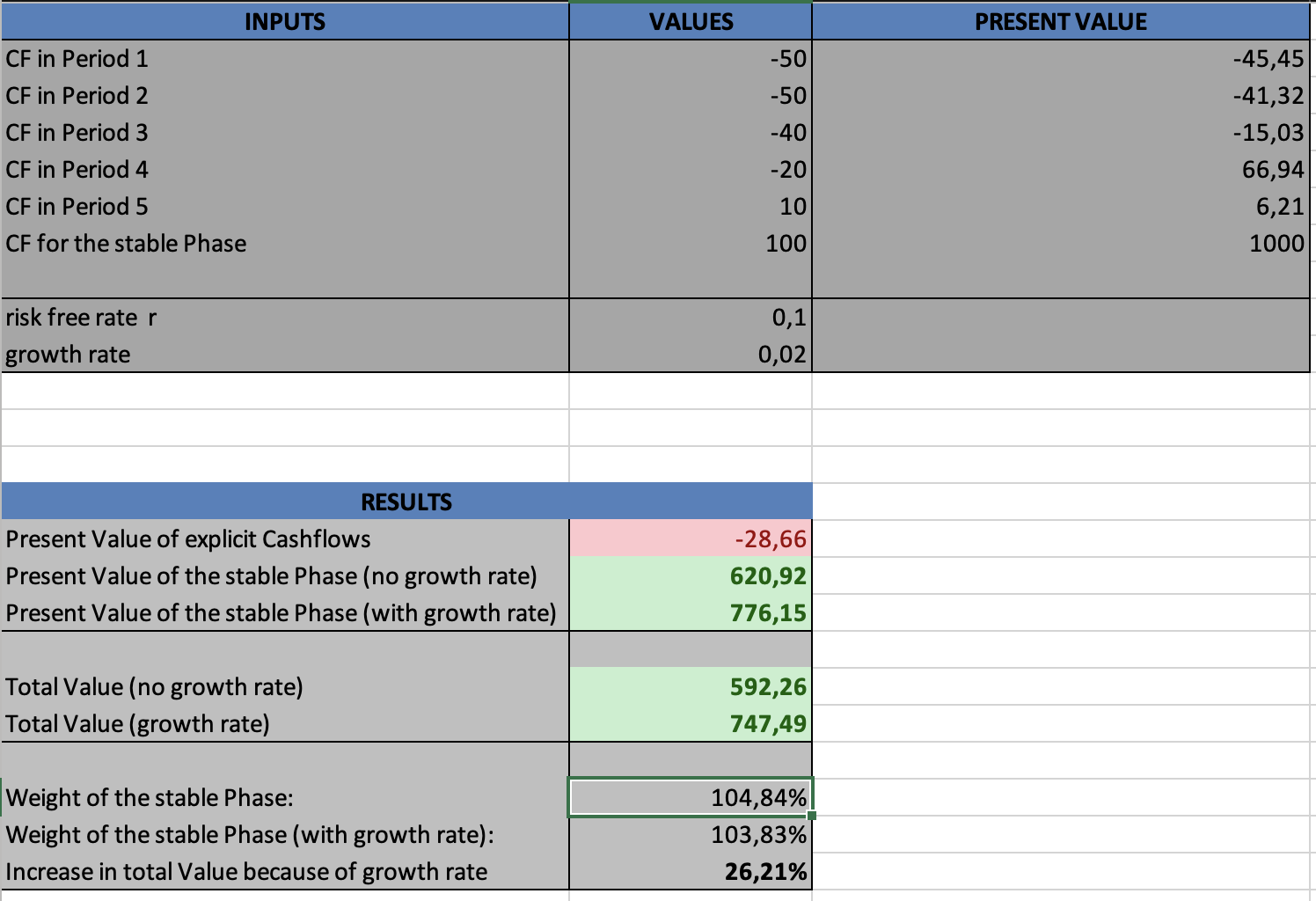

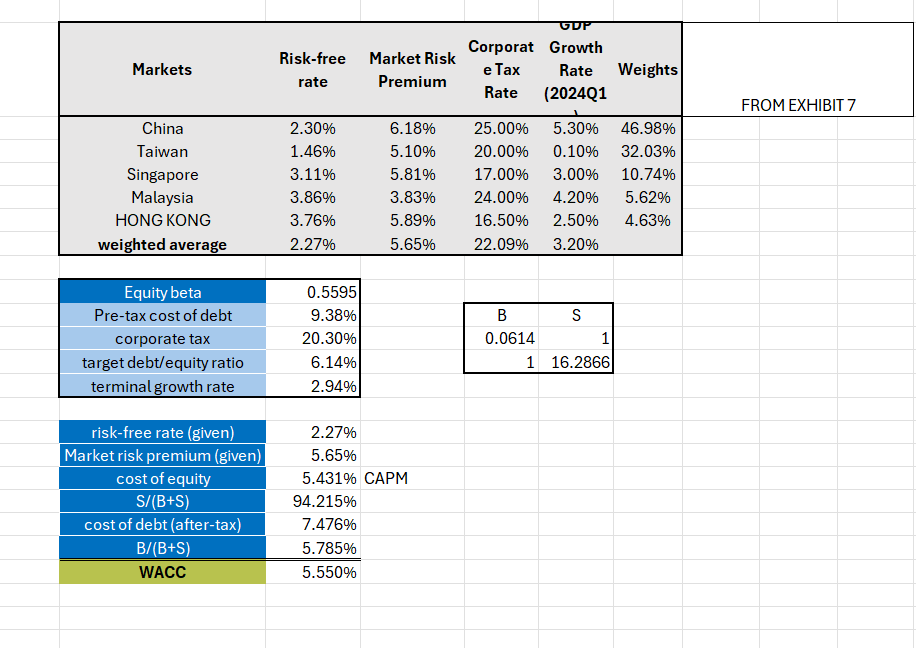

The discounted cash flow (DCF) model aims to measure the intrinsic value of a company. It does this by forecasting the expected future cash flows generated by the company and discounting them back to the present using an appropriate discount rate that reflects the risk specific for the company. The goal is to estimate the equity value of the company. The discount rate is often the WACC (weighted-average cost of capital), or the cost of equity based on the method you are using. The method can either be to estimate the enterprise value which would represent the value of the whole company including its assets and its liabilities. For this method you would use the WACC. To get to the equity value directly you have to subtract the part of the liabilites that contribute to the cash flows and create cash flows that are only generated by equity. You will also have to find out the cost of equity, which can be done using the CAPM. After doing this you will have the equity value of the company.

DCF logic (simplified):

- Explicit forecast period: Forecast cash flows CFt for years t = 1 … T and discount them at rate r.

- Terminal value: Estimate the value beyond year T using a stable long-term assumption. This is referred to as an annual perpetuity and can include a growth factor if it aligns with the assumptions about the company.

Formula (illustrative):

Value = Σt=1…T CFt / (1 + r)t + Terminal Value / (1 + r)T

This formula can differ based on which type of DCF model you are using. If you are using the WACC to discount your cashflows you will be left with the enterprise value of the company’s total assets and liabilities and not the equity value. To get to the equity value, you will have to subtract the liabilities.

Equity value using WACC = (Σt=1…T CFt / (1 + WACC)t + Terminal Value / (1 + r)T) – Liabilities

If you are using the cash flows that can be assigned to the equity of the company and the cost of equity to discount these cash flows you will automatically end up with the equity value.

Equity value = Σt=1…T CFtequity / (1 + requity)t + Terminal Value / (1 + r)T

Strengths of the DCF

You can already see that there are differences within one single model that need to be understood. In practice the method for the total company value is widely used. This is because of its fundamental strength, which is its simplicity and its convenience. It is very easy to follow and you can see how different assumptions will affect the firm value in different ways. It therefore forces the analyst to evaluate and model the key drivers of financial growth. Like looking at the growth rate, investments in working capital and the risk the company is currently facing. As a result, DCF valuations are often used for long-term strategic decisions, mergers and acquisitions, and fairness opinions.

Weaknesses of the DCF

Following this the major problems with the DCF-models are its assumptions. They are based on historical values and the CAPM, which both give no valuable outlook on the future. But as there is no better method currently to predict future cash flows, the method is holding strong in practice, although empirically it seems to be unsuitable. The resulting model is also very sensitive to the assumptions made. Especially looking at the growth rate or the discount rate which will accumulate over time.

Multiples valuation: estimating relative value

Now coming to the multiples-based valuation, this valuation method focuses on looking at the relative value of a company rather than the intrinsic value of a company. This means that the firm is compared to similar companies using different key values such as:

- Price-to-Earnings (P/E)

- Enterprise Value to EBITDA (EV/EBITDA)

- Enterprise Value to Sales (EV/Sales)

The process of choosing and working with multiples is simple. There are two main approaches: the similar public company-method, which is used to create and compare multiples based on data from a company that is publicly traded on a stock market. The second method is the recent acquisition-method, which will look at the transaction prices for a similar company. As the name of the first method indicates, the chosen companies must be similar to the valued company. You can achieve this by looking at the size of the company, the industry and the location or other features and specifying different values for these aspects (i.e. number of employees, pharmacy, Germany).

Implicit assumptions behind multiples

Although multiples are often perceived as simpler ways of valuing a company, they embed the same fundamental assumptions as a DCF model, albeit in a less transparent way.

A valuation multiple implicitly reflects:

- Expected growth

- Risk and discount rates

- Capital structure

- Profitability and reinvestment needs

For example, a high EV/EBITDA multiple usually signals that the market expects strong future growth or low risk. In other words, the market has already performed a form of discounted cash flow analysis — but the assumptions are hidden inside the multiple.

Strengths of multiples

Multiples are an easy way to get an overview of the value of a company and compare the estimated values to other companies on the market. They can also be used to quickly check the plausibility of a firm value estimated with the DCF model. The main strength is again its simplicity but this time in a much faster and easier way. They are used to compare the company to competitors and to give insights on how the company would perform against them and on the stock market. It’s also very helpful when valuing smaller companies because they might not have the amount of historical data organized and needed to value this with a DCF method.

Weaknesses of multiples

One of the biggest weaknesses is the requirement of finding a similar company that is traded on the stock market, or which information is publicly available. They therefore can also be manipulated easily because they are less transparent than other methods and can be adjusted very easily (what is “similar”?). They also cannot be seen as objective values as the market is estimating them with no individual interferences. Therefore, they are not consistent and have to be used with care. You should always make plausible assumptions, that can be explained by the multiple and the current situation of the company.

When to use them and the “football field”

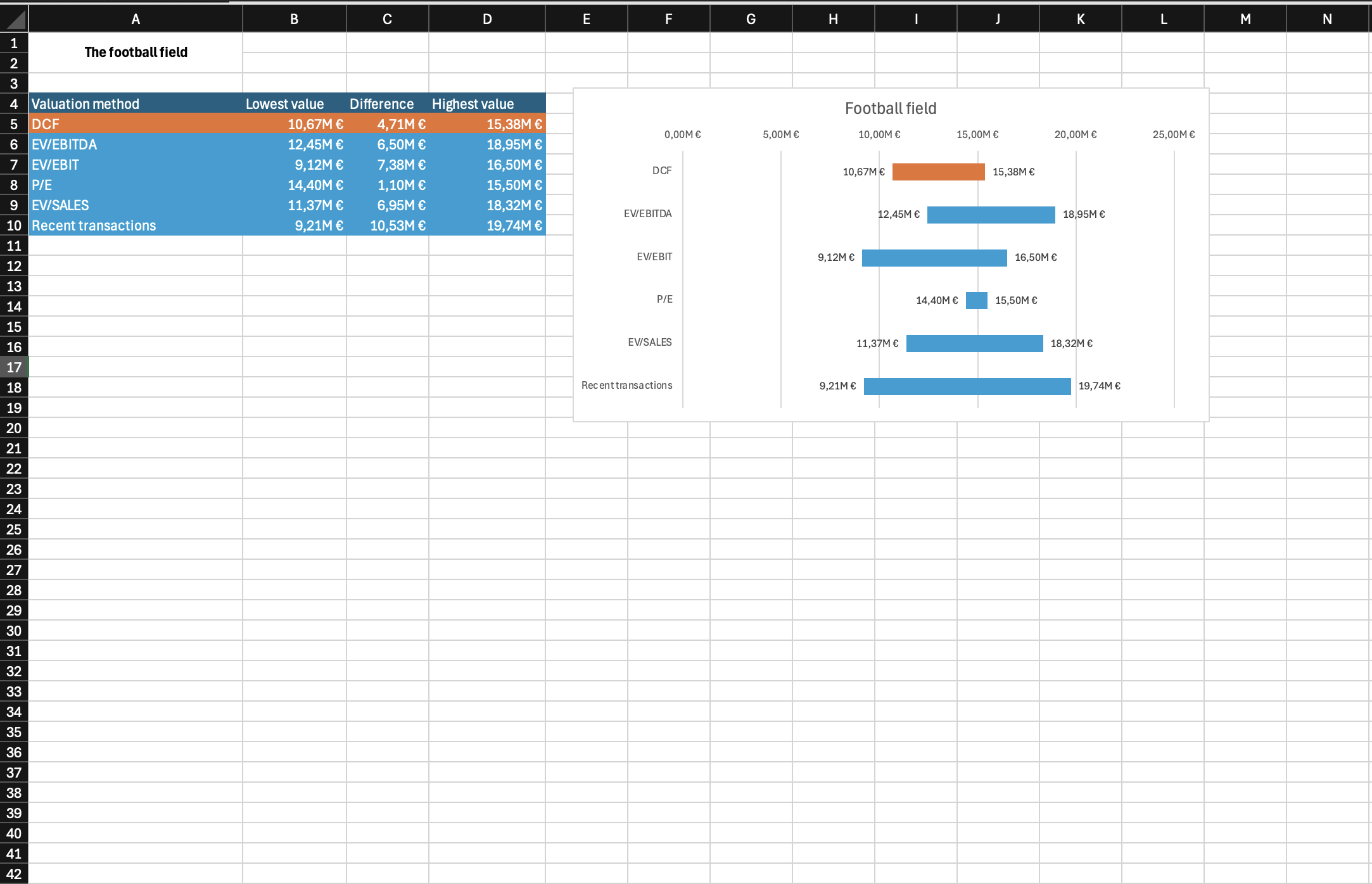

To really get behind the use of multiples and the DCF model all together we are looking how to combine them together in a meaningful way. Multiples are often used to create a “football field”. This technique describes a graph that is summarizing valuation ranges across methods rather than delivering a single point estimate. This is especially helpful when you are currently negotiating on an M&A deal to see if the offered prices are aligned with your assumptions and whether you want to accept or not.

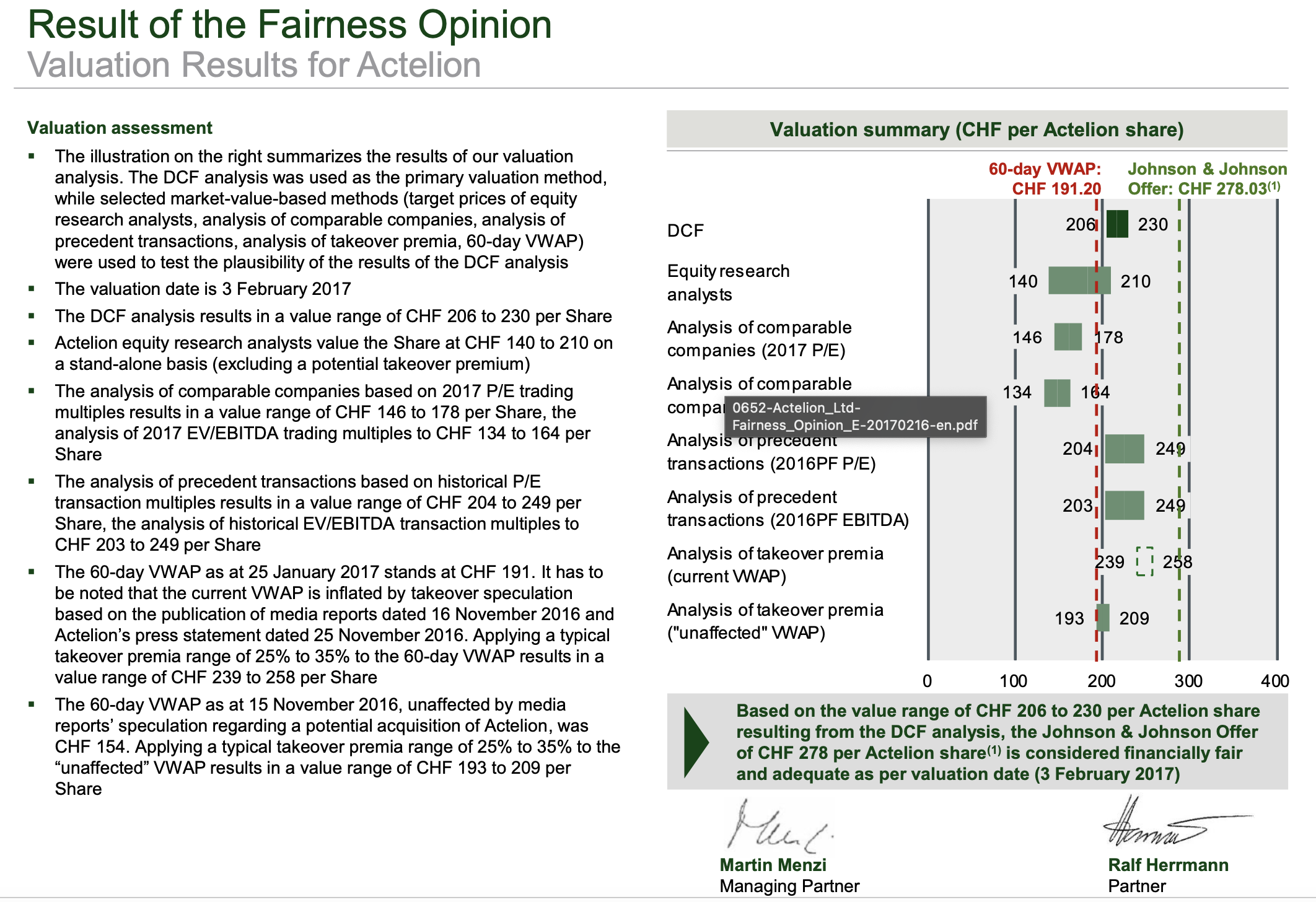

A great example for the combination of the DCF model and multiples is the acquisition from Actelion by Johnson & Johnson. To see if the offer was acceptable and fair, they hired valuation professionals from Alantra. Alantra gathered data and estimated multiple values to compare the offer. They used the graph of the “football field” to make it visually appealing and instinctive. You can see that the green line is far right beyond the red line and therefore it can be seen as a fair offer considering the other values that have been estimated by Alantra in their fairness opinion for Actelion. This is because the more the value is on the right side of the graph, the higher it is.

You can download the full fairness opinion here

You can download the Excel file provided below, which contains the “Football field” example.

You can see here that the estimated value from the DCF is a more on the lower end than the consensus of the market. This is not necessarily a problem as the market might have already considered synergies or future events that the DCF model did not capture or simply is not expecting, due to a lack of information (insiders etc.).

As you can see, rather than choosing between DCF and multiples, practitioners usually apply both approaches in a complementary way:

- DCF models are well suited for estimating intrinsic value and analyzing long-term fundamentals.

- Multiples are useful for understanding how the market currently prices similar firms.

- In IPOs and M&A transactions, both methods are typically combined to form a valuation range.

A robust valuation rarely relies on a single number. Instead, it emerges from comparing and reconciling different approaches.

Conclusion

DCF and multiples-based valuation often lead to different results because they answer different questions. DCF models aim to estimate intrinsic value based on explicit assumptions, while multiples reflect relative value and prevailing market expectations.

Recognizing the strengths and limitations of each method is essential for sound financial analysis. By combining both approaches and critically assessing their underlying assumptions, analysts can arrive at more balanced and informative valuation outcomes.

To sum up…

Both DCF and multiples are useful tools, but neither should be applied mechanically. A solid valuation comes from understanding what each method captures, where it can mislead, and how results change when assumptions or peer groups change. In practice, triangulating across methods provides the most reliable foundation for decision-making.

Why should I be interested in this post?

For a student interested in business and finance, this post provides a concrete bridge between theory and practice. Valuation models such as the two-stage DCF are not only central to courses in corporate finance, but also widely used in internships, case interviews, and real-world transactions. Understanding how sensitive firm values are to assumptions on growth and discount rates helps students critically assess valuation outputs rather than taking them at face value, and prepares them for practical applications in consulting, investment banking, or asset management.

Related posts on the SimTrade blog

▶ All posts about financial techniques

▶ Jorge KARAM DIB Multiples valuation method for stocks

▶ Andrea ALOSCARI Valuation methods

▶ Samuel BRAL Valuing the Delisting of Best World International Using DCF Modeling

▶ Cornelius HEINTZE The effect of a growth rate in DCF

Useful resources

Paul Pignataro (2022) Financial modeling and valuation: a practical guide to investment banking and private equity Wiley, second edition.

Aswath Damodaran (2015)Explanations on Multiples

About the author

The article was written in December 2025 by Cornelius HEINTZE (ESSEC Business School, Global Bachelor in Business Administration (GBBA) – Exchange Student, 2025).

▶ Read all articles by Cornelius HEINTZE .