My internship experience as a financial research analyst in Tianfeng Securities

In this article, Pai LI (ESSEC Business School, Global BBA, 2021-2023) shares her internship experience as an assistant financial research analyst in Tianfeng Securities which is a Securities Research Institute in China.

The Company

Tianfeng Securities is a global full-license integrated financial securities service provider. Tianfeng Securities Research Institute is a high-end industry research think tank in China. It brings together more than 200 team members to build bridges and links between funds and industry and enhance the ability of financial services to serve the substantial economy.

Tianfeng Research Institute adheres to the “industry-oriented” driving force, creates a unique financial ecological alliance, forming a complete ecological chain that runs through the life cycle of enterprises and industries.

Logo of Tianfeng Securities

![]()

Source: Tianfeng Securities.

My Internship

My missions

The department I practiced for was the Securities Research Institute, and the position was financial research assistant. My work mainly consisted of two parts, the daily research work about industry and the related work of writing in-depth research reports about companies.

Daily work includes using a financial database called Wind (like Bloomberg but focused on mainland China) to find industry data, prospectus, company annual reports and other materials, doing market shares calculations, doing valuation models, collecting information for industry research topics, writing new stock purchase proposals, updating internal industry databases, modifying and improve the Powerpoint presentation of roadshow reports, operating social media for publishing weekly reports, comments, and in-depth reports.

In addition to the above routines, I also participated in the writing of the first draft of the Institute’s in-depth reports. At the beginning I wrote some simple company tracking reviews. These short reports were completed by referring to the relevant announcements and materials of the company. Next, I gradually participated in the writing of the in-depth reports. In the process of continuous maturity and improvement of the reports, I learned a lot of research skills.

Writing in-depth reports requires the collection of a large amount of financial and business data, and an overall overall grasp of the structure and context of the company. Not only did I improve my ability to understand the company’s business by collecting information from all parties, but I also learned to build a valuation model to predict the company’s future performance.

Required skills and knowledge

In terms of technical skills, you need to have financial knowledge, frameworks and insights for industry analysis and company analysis, and report writing skills. These professional abilities of mine have been greatly improved during this internship.

In terms of behavior skills, industry researchers need to have logical thinking ability to predict the future direction of companies and industries. In addition, interpersonal communication skills are also very important, through which research results can be presented to the buy-side clients in the best possible state.

What I have learnt

My biggest gain in this internship is that I learned how to write a professional report. I summarize the essential qualities of an extraordinary in-depth report into seven points:

- The selection of the company is meaningful.

- The core point of view about the company is highlighted.

- The discussion about the business of the company is rigorous and logical.

- The business and financial data are authentic and credible.

- The business charts are clear and detailed.

- The text is concise and straightforward.

- The exhibit are exciting.

In addition, I also deepened my understanding of the industry of securities firm research. I realized that it is a highly homogenized industry, because the same teams research the same companies, and the companies provide the same type of information (announcements, financial and accounting data). This is an industry that pays great attention to timeliness. When a news comes out, investors expect to see relevant research results immediately, and will be swept away by other reports later. This is an industry with high barriers to entry. When looking for data, well-funded securities companies are equipped with sufficient database access qualifications, while small agencies can only search for free public information. Every year, many finance students try hard to get an internship in industry financial research, but few can get it. Therefore, in the face of such as intense competition, what we need to do is to maximize our core competitive advantages.

Three key financial concepts

Here are 3 useful valuation methods.

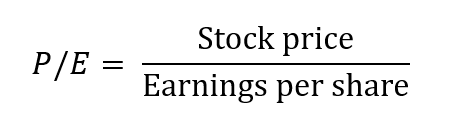

P/E Valuation Method

The Price-to-Earnings (P/E) valuation method is based on the price-earnings (P/E) ratio:

EPS comes in two main varieties. TTM is a Wall Street acronym for “trailing 12 months”. This number signals the company’s performance over the past 12 months. The second type of EPS is found in a company’s earnings release, which often provides EPS guidance. This is the company’s best-educated guess of what it expects to earn in the future. These different versions of EPS form the basis of trailing and forward P/E, respectively.

The price-earnings ratio can be used to predict the stock price by the following calculation formula:

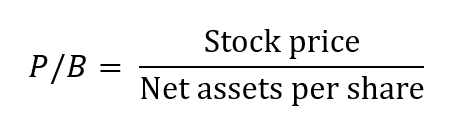

P/B valuation method

The P/B valuation method is based on the price-to-book (P/B) ratio:

Generally speaking, stocks with low price-to-book ratios generally have relatively high investment value (in their balance sheet).

The price-to-book ratio can be used to predict the stock price by the following calculation formula:

The P/B valuation method is suitable for companies with large and relatively stable net assets, such as steel, coal, construction and other traditional companies. However, it is not suitable for enterprises with light assets such as technology Internet and consulting services, which are small in scale and dominated by labor costs. The valuation should be based on the principle of “peer ratio and historical ratio”. Usually, the lower the price-to-book ratio, the safer the investment.

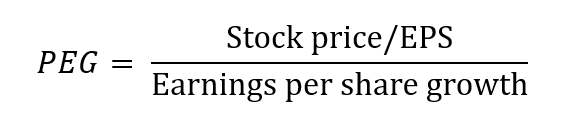

PEG valuation method

The PEG valuation method is based on the price-to-earnings growth (PEG) ratio:

In general, the smaller the PEG, the better and safer. But PEG>1 does not mean that the stock is overvalued. It must be measured according to the overall indicators of its peers. If the PEG is greater than 1, but its peers are higher than it, which also means that although the company’s PEG is already higher than 1, its value may also be is underrated.

Related posts on the SimTrade blog

▶ All posts about Professional experiences

▶ Anna BARBERO Career in finance

▶ Alexandre VERLET Classic brain teasers from real-life interviews

▶ Louis DETALLE A quick review of the Equity Research analyst’s job…

Useful resources

About the author

The article was written in May 2022 by Pai LI (ESSEC Business School, Global BBA, 2021-2023).