In this article, Theo SCHWERTLE (Maastricht University, School of Business and Economics, Bachelor in International Business, 2023) explains how behavioral biases can influence trading of market aprticiapnts.

Behavioral biases of investors

In complex decision environments, people use basic judgements and preferences to simplify the scenario rather than adhere to a strictly rational approach. This use of mental shortcuts is called heuristics, which are quick and instinctively appealing but may result in poor outcomes (Tversky and Kahneman, 1974). The traditional financial theory (based on expected utility theory) assumes that people are rational agents. In contrast to traditional financial theory, behavioral theories argue that people are generally risk-averse with a skewed view of probability (Kahneman and Tversky, 1979). Some common behavioral biases that have been identified in the literature on investment decisions include overconfidence, the disposition effect and herding behavior.

Prospect Theory

We start with the two main drivers of irrationality: value perception and probability perception.

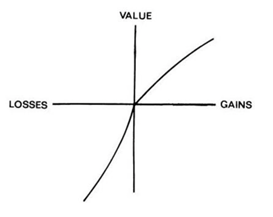

Value perception. The value function proposed by Kahneman and Tversky (1979) is characterized by the following features. First, it is determined based on departures from a reference point. Second, it typically has a downward, concave slope for gains and an upward, convex slope for losses. This suggests that individuals perceive losses as more painful gains as shown in Figure 1.

Figure 1. Perceived value function.

Source: Kahneman and Tversky (1979).

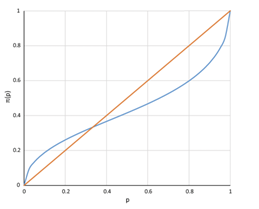

Probability perception. Individuals tend to assign a lower probability value to outcomes that are more likely to occur and, a higher probability value to outcomes that are less likely to occur as shown in Figure 2.

Figure 2. Perceived probability.

Source: Kahneman and Tversky (1979).

Overconfidence

Overconfidence manifests as an inclination to have an irrationally excessive level of trust in one’s own abilities and opinions and has been thoroughly investigated across many fields (Fischhoff et al., 1977).

Gervais and Odean (2001) explore how overconfidence develops as a result of a dynamic change in beliefs about one’s ability after observing successes and failures. Successful traders tend to be overconfident due to attributing too much credit to their own ability. They showed that overconfidence is highest among inexperienced traders, as proper self-assessment only develops over time. This leads to suboptimal behavior, such as increased trading volume and volatility, lower expected profits, and poor information utilization (Statman et al., 2006).

Ekholm and Pasternack (2007) investigate the link between overconfidence and investor size.

They show that larger investors are less overconfident than small investors. They also show that larger investors, on average, react more positively to good news and more negatively to bad news than smaller investors. Evidence suggests that smaller, more overconfident investors have worse performance following negative news (Ekholm and Pasternack, 2007).

Grinblatt and Keloharju (2009) argue that sensations seekers (people receiving more speeding tickets) and those who showed more overconfidence as measured by a psychological assessment traded more than the average, even after controlling for other factors that might explain trading activity like age, income and gender. Similarly, individual investors tend to buy stocks that have recently caught their attention, like stocks with high trading volume, extreme one-day returns, or those in the news, whereas institutional investors, especially those who follow a value strategy, do not (Barber and Odean, 2007). These results are confirmed by Barber et al. (2022) as Robinhood users, which are, as evidence suggests, less experienced traders, trade substantially more high-attention stocks.

Additionally, men are more prone to overconfidence than women, particularly in male-dominated industries like finance. Thus, men trade more than women and perform worse in terms of returns. Male investors not only engage in more frequent trading but, compared to female investors, also hold larger and less diversified portfolios (Barber & Odean, 2001; Lepone et al., 2022).

Why should I be interested in this post?

This post explores heuristics and behavioral biases in decision-making, particularly in the context of investment decisions. Overconfidence can lead to poor outcomes. Additionally, it touches on gender differences, with men being more prone to overconfidence and engaging in more frequent trading. By understanding these biases, readers can gain insights into human behavior, make more informed investment decisions, and explore the impact of gender on financial outcomes. Overall, this post offers valuable insights into decision-making processes and their implications.

Related posts on the SimTrade blog

▶ Jayati WALIA Trend Analysis and Trading Signals

▶ Shruti CHAND Technical Analysis

Useful resources

Barber, B.M. and Odean, T. (2007) All That Glitters: The Effect of Attention and News on the Buying Behavior of Individual and Institutional Investors Review of Financial Studies 21(2):785–818.

Barber, B.M. and Odean, T. (2001) Boys will be Boys: Gender, Overconfidence, and Common Stock Investment The Quarterly Journal of Economics 116(1):261–292.

Ekholm, A. and Pasternack, D. (2007) Overconfidence and Investor Size European Financial Management.

Fischhoff, B., Slovic, P. and Lichtenstein, S. (1977) Knowing with certainty: The appropriateness of extreme confidence. Journal of Experimental Psychology: Human Perception and Performance 3(4):552–564.

Gervais, S. and Odean, T. (2001) Learning to Be Overconfident Review of Financial Studies 14(1):1–27.

Grinblatt, M. and Keloharju, M. (2009) Sensation Seeking, Overconfidence, and Trading Activity The Journal of Finance 64(2):549–578.

Kahneman, D. and Tversky, A. (1979) Prospect Theory: An Analysis of Decision under Risk Econometrica 47(2): 263.

Lepone, G., Westerholm, J. and Wright, D. (2022) Speculative trading preferences of retail investor birth cohorts Accounting & Finance.

Statman, M., Thorley, S. and Vorkink, K. (2006) Investor Overconfidence and Trading Volume Review of Financial Studies 19(4):1531–1565.

Tversky, A. and Kahneman, D. (1974) Judgment under Uncertainty: Heuristics and Biases Science 185(4157):1124–1131.

About the author

The article was written in May 2023 by Theo SCHWERTLE (Maastricht University, School of Business and Economics, Bachelor in International Business, 2018-2023).

3 thoughts on “The Psychology of Trading”

Comments are closed.