In any asset management class, students are taught that diversification is a key to unlock mathematically optimal risk-adjusted returns. However, Warren Buffett, one of the world’s most successful investors, would beg to disagree: to him, “diversification is protection against ignorance. It makes little sense if you know what you are doing.”

In this article, Hadrien PUCHE (ESSEC Business School, Grande École Program, Master in Management, 2023-2027) discusses Buffett’s challenge to modern portfolio theory, and explains why, for a sophisticated investor, concentration may sometimes also be an option.

About Warren Buffett and this quote

Warren Buffett is the chairman and CEO of Berkshire Hathaway, a multinational holding company, that he transformed over the years into a conglomerate businesses (Geico, dairy queen…) and large equity stakes in listed companies (Coca-Cola, Apple…). He is widely considered the most successful value investor in history. He is known for his discipline, long-term perspective, and his ability to distinguish between market price and intrinsic value. This specific quote originates from his 1993 annual shareholder meeting, where he addressed the difference between a “know-nothing” investor and a “know-something” investor.

Warren Buffett

Source : CNBC

This also suggests that the reason Buffett said that isn’t to give a valuable lesson to investors, but to convince them that instead of looking for diversification and investing themselves, they should entrust their money to Berkshire Hathaway, because they have the informational edge to overperform a simply well-diversified portfolio.

Analysis of the quote

The core of Buffett’s idea is that risk is not a statistical measurement of price volatility, but rather a function of knowledge. If you have three companies you know perfectly (meaning you understand their business model, their management, and their competitive moat) then adding a fourth company “at random” just to diversify will actually increase your overall probability of loss.

Having more diversified portfolios lead to two critical issues:

- The dilution of quality: your best investment idea is, by definition, better than your tenth best idea. By adding more stocks, you are moving away from your highest-conviction choices toward relatively more mediocre ones, watering down the potential returns of your portfolio.

- Knowledge risk: spreading your attention across too many holdings dilutes your ability to monitor each one perfectly. You are more likely to miss a fundamental change in a business if you are tracking fifty companies instead of five.

Essentially, diversification only reduces risk when you add an asset you know nothing about to a portfolio of other assets you know nothing about. It is a great tool for the “ignorant” (in the financial sense) to protect themselves from a total wipeout, but it is a “downgrade” for anyone with a true informational edge.

Financial concepts linked to this quote

To better understand this tension between concentration and diversification, we can look at three key concepts that are very important to modern finance.

Modern Portfolio Theory (MPT) & Diversification

In every finance textbook, Modern Portfolio Theory (MPT) is presented as the “only free lunch” in investing. It suggests that by holding a large number of non-correlated assets, an investor can eliminate “idiosyncratic risk” (the risk specific to a company), leaving only the systematic risk of the market.

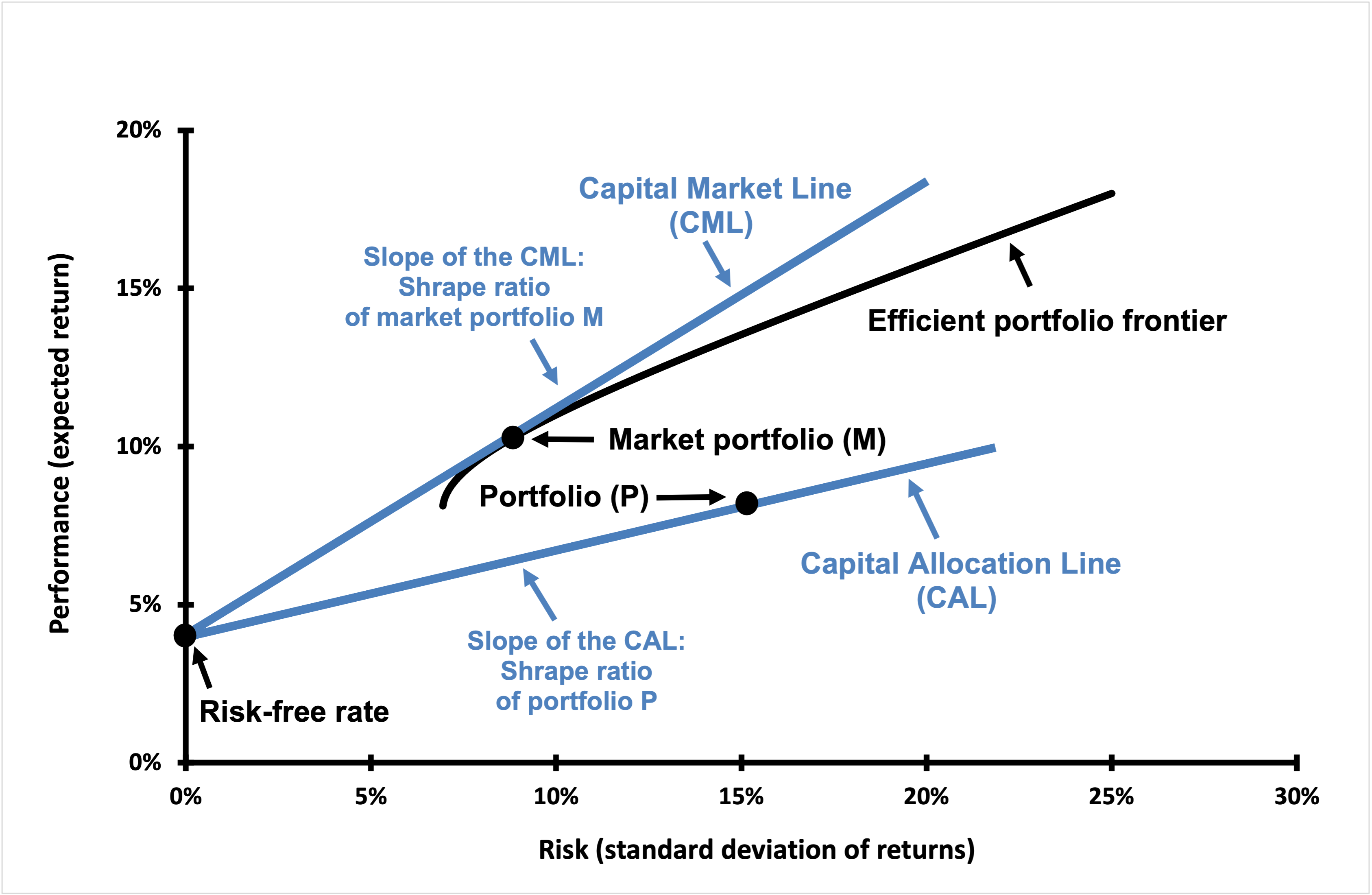

The Capital Market Line (CML) represents the most efficient combinations of the risk-free asset and the market portfolio. As shown in the graph below, every point on this line offers the highest possible (expected) return for a specific level of risk, effectively defining the “best” available trade-off. In the world of MPT, any portfolio falling to the right of this line is sub-optimal, while the area to the left remains mathematically unreachable.

However, MPT focuses almost entirely on the mathematical “co-variance” of stock prices rather than the underlying business quality. Buffett’s quote acts as a philosophical counter-weight to this academic standard: he suggests that MPT is a defensive tool, designed for those who cannot identify intrinsic value. If you cannot tell a good business from a bad one, MPT is your best protection; but if you can, it is nothing more than a constraint.

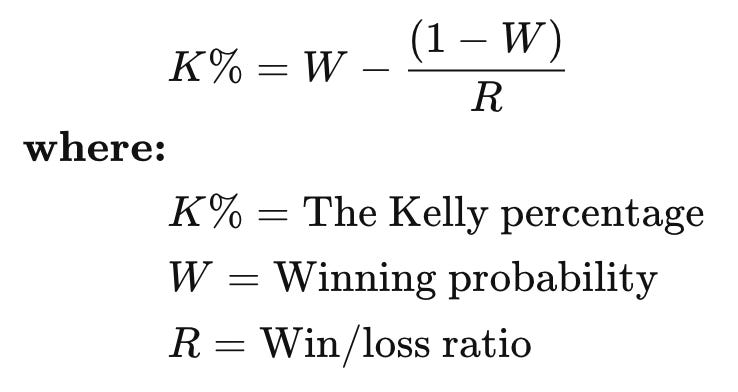

The Kelly Criterion

While MPT seeks to minimize variance, the Kelly Criterion seeks to maximize the growth of wealth. Originally developed by John Kelly at Bell Labs, this formula determines the optimal size of a series of bets based on the probability of success and the “edge” the bettor has.

Unlike the MPT, which would suggest a small allocation to any single stock to keep the portfolio “balanced,” the Kelly Criterion supports heavy concentration. It suggests that when the odds are heavily in your favor, the “bet” should be significantly larger, and can represent a significant portion of your capital. It is the mathematical foundation for the “betting big” philosophy that Buffett has applied throughout his career at Berkshire Hathaway.

Market Imperfection and Information Asymmetry

The Efficient Market Hypothesis (EMH) assumes that all information is already reflected in stock prices. However, Buffett’s success is built on the reality of market imperfections. For an investor to have a true edge, there must be a gap in how information is processed. If you spend hundreds of hours studying a specific niche, you may identify a ‘valuation gap’ that the average market participants missed. But you can’t do this work on all industries and all assets. Because of that, concentration allows you to maximize the financial value of that specific information.

Diversification, by contrast, “washes away” that hard-earned advantage, by blending your good insights with the general noise of the market average.

My view on this quote

While the logic of concentration is mathematically sound, its execution faces a major practical limit: intellectual honesty. To apply Buffett’s philosophy, you need to understand if you are yourself one of the professional managers who can overperform, or a simple retail saver who should go to diversification for protection against your own ignorance.

For an individual investor: humility as a strategy

For the vast majority of retail investors, diversification remains the “wisest default.” The “ignorance” Buffett mentions is not pejorative, but simply a realistic assessment of the time and resources one can dedicate to market analysis. Without a professional informational edge, concentration can often lead to a martingale trap, where an investor doubles down on loosing positions, based on an emotional conviction that the market is wrong and refusal to accept defeat. For this group, Modern Portfolio Theory (MPT) is not a constraint, but a necessary safeguard.

The institutional management problem

For an aspiring asset manager, the reality is a bit more complex, and highlights a structural paradox in the industry, where career incentives are more towards diversifying a portfolio than making a small number of concentrated bets.

- Career risk versus absolute risk: If a concentrated portfolio underperforms, the manager risks being “wrong alone” and losing their job. If a diversified portfolio fails, they are “wrong with the crowd,” and no one will really consider that the loss is their responsibility.

- The “closet indexing” trap: To minimize tracking error, many professionals choose the safety of the average. However, Buffett’s logic suggests that if you are not prepared to know your holdings better than the rest of the market, you are merely charging active management fees for a passive result, effectively selling the “market average” at a premium price.

Buffet’s call to invest with berkshire hathaway

Finally, we must consider context behind Buffett’s rhetoric. As we already stated, by framing diversification as a “protection against ignorance,” he is not just teaching finance, but also subtly positioning Berkshire Hathaway as the ideal destination for capital. He encourages investors to recognize their own limitations and, instead of buying a “know-nothing” index, to entrust their wealth to a firm that possesses the rare informational edge required to concentrate effectively. In essence, this quote is also a good lesson in brand positioning: it justified Berkshire Hattaway’s market concentration as the key to overperforming the market.

Why should you keep this quote in mind?

This principle forces you to ask a fundamental question: “Do I have a true edge, or am I just guessing?” If you are a student or a retail investor, recognizing your own ignorance is the first step toward safety. Diversification is your best friend when you are learning.

However, and this is where Buffett’s spirit is very important, if you want to achieve extraordinary results, you must first develop the analytical rigor to know your investments better than the rest of the market. Knowing the “average” only gets you the “average” return.

Related posts on the SimTrade blog

Business & Finance quotes

▶ Hadrien PUCHE Price is what you pay, value is what you get – Warren Buffett

▶ Hadrien PUCHE The stock market is designed to transfer money… – Warren Buffett

Useful resources

Academic research

Kelly J. L. Jr. (1956) A New Interpretation of Information Rate, Bell System Technical Journal 35(4) 917–926.

Markowitz, H. (1952) Portfolio Selection, The Journal of Finance 7(1): 77-91.

Sharpe W.F. (1991) The Arithmetic of Active Management, Financial Analysts Journal 47(1) 7-9.

Business resources

Buffett, W.E. Berkshire Hathaway Shareholder Letters

S&P Global. SPIVA Scorecards

About the Author

This article was written in April 2026 by Hadrien PUCHE (ESSEC Business School, Grande École Program, Master in Management, 2023-2027).

▶ Discover all articles by Hadrien PUCHE