In this article, Roberto RESTELLI (ESSEC Business School, Master in Finance (MiF), 2025–2026) explains the role of discounted cash flow (DCF) within the broader toolkit of company valuation—when to use it, how to build it, and where its limits lie.

Introduction to company valuation

Valuation is the process of determining the value of any asset, whether financial (for example, shares, bonds or options) or real (for example, factories, office buildings or land). It is fundamental in many economic and financial contexts and provides a crucial input for decision-making. In particular, the importance of proper company valuation emerges in the preparation of corporate strategic plans, during restructuring or liquidation phases, and in extraordinary transactions such as mergers and acquisitions (M&As). Company valuations are also useful in regulatory and tax contexts (for example, transfers of ownership stakes or determining value for tax purposes). Entrepreneurs and investors can evaluate the economic attractiveness of strategic options, including selling or acquiring corporate assets.

The need for a company valuation typically arises to answer three questions: Who needs a valuation? When is it necessary? Why is it useful?

Users and uses of company valuation

Different categories rely on valuation. In investment banks, Equity Capital Markets use it for IPO research and coverage (including fairness opinions), while M&A teams analyze transactions and prepare fairness opinions to inform deal decisions. In Private Equity and Venture Capital, valuation supports majority/minority acquisitions, startup assessments, and LBOs. Strategic investors use it for acquisitions or divestitures, stock‑option plans, and financial reporting. Accountants and appraisal experts (CPAs) prepare fairness opinions, tax valuations, technical appraisals in legal disputes, and arbitration advisory.

Beyond these, regulators and supervisory bodies (e.g., the SEC in the U.S., CONSOB in Italy) require precise valuations to ensure market transparency and investor protection. Corporate directors and managers need valuations to define growth strategies, allocate capital, and monitor performance. Courts and arbitrators request valuations in disputes involving contract breaches, expropriations, asset divisions, or shareholder conflicts. Owners of SMEs—backbone of the Italian economy—use valuations to set sale prices, manage generational transfers, or attract investors.

Examples of valuation

Valuations appear in equity research (e.g., a UBS report on Netflix indicating a short‑ to medium‑term target price based on public information), in M&A deal analyses (including subsidiary valuations and group structure changes), and in fairness opinions (e.g., Volkswagen’s acquisition of Scania). They are central in IPOs to set offer prices and expectations. Banks also rely on valuations in lending decisions to assess enterprise value and credit risk, clarifying the allocation of requested capital.

Core competencies in valuation

High‑quality valuation requires business and strategy foundations (industry analysis, competitive context, business‑model strength), theoretical and technical finance (NPV, pricing models, corporate cash‑flow modeling), and economic theory (uncertainty vs. value and limits of standard models). Valuation is not just technique: it balances modeling choices with empirical evidence and fit‑for‑purpose estimates.

A fundamental principle is that a firm’s value is driven by its ability to generate future cash flows, which must be estimated realistically and paired with an appropriate risk assessment. Higher uncertainty in cash‑flow estimates implies a higher discount rate and a lower present value. Discount‑rate choice depends on the model (e.g., CAPM for systematic risk via beta). Sustainability also matters: modern practice increasingly integrates environmental, social, and governance (ESG) factors—climate risk, regulation, and reputation—into valuation.

General approaches and specific methods

Income Approach. Present value of future benefits, risk‑adjusted and long‑term (e.g., discounted cash flows).

Market Approach. Value estimated by comparing to similar, already‑traded assets.

Cost (Asset‑Based) Approach. Value derived by remeasuring assets/liabilities to current condition.

Within these, DCF is among the most studied and used. It can be computed from the asset perspective via free cash flow to the firm (FCFF) or from the equity perspective via free cash flow to equity (FCFE). Under the asset‑based approach, other methods include net asset value and liquidation value. Additional families include economic profit (e.g., EVA, residual income) and market‑based analyses: trading multiples (e.g., P/E, EV/EBITDA), deal multiples, and premium analysis (control premia). Four further techniques often considered are current market value (market capitalisation), real options (valuing flexible investment opportunities), broker/analyst consensus, and LBO analysis (value supported by leveraged acquisition capacity).

Critical aspects and limits of valuation models

Each method has strengths and limits. In DCF, accuracy depends on projection quality; macro cycles can render forecasts unreliable. In market‑multiple analysis, industry/geography differences and poor comparables can distort results. Real options are powerful for uncertainty but require subjective parameters (e.g., volatility), introducing error bands.

Practical applications of company valuation

Firms use valuation to plan growth, allocate capital, and budget projects. In disputes and restructurings, it informs liquidation values and creditor negotiations. It also supports governance and incentives (e.g., option plans) that align managers with shareholders. In short, valuation enables both day‑to‑day management and extraordinary decisions.

Discounted Cash Flow (DCF)

What is a DCF?

The discounted cash flow (DCF) method values a company by forecasting and discounting future cash flows. Originating with John Burr Williams (The Theory of Investment Value), DCF seeks intrinsic value by projecting cash flows and applying the time value of money: one euro today is worth more than one euro tomorrow because it can be invested.

Advantages include accuracy (when inputs are sound) and flexibility (applicable across firms/projects). Risks include reliance on uncertain projections and difficulty estimating both discount rates and cash flows; hence outputs are estimates and should be complemented with other methods.

Uses of DCF

DCF is widely applied to value companies, analyse investments in public firms, and support financial planning. The five fundamental steps are:

- Estimate expected future cash flows.

- Determine the growth rate of those cash flows.

- Calculate the terminal value.

- Define the discount rate.

- Discount future cash flows and the terminal value to the present.

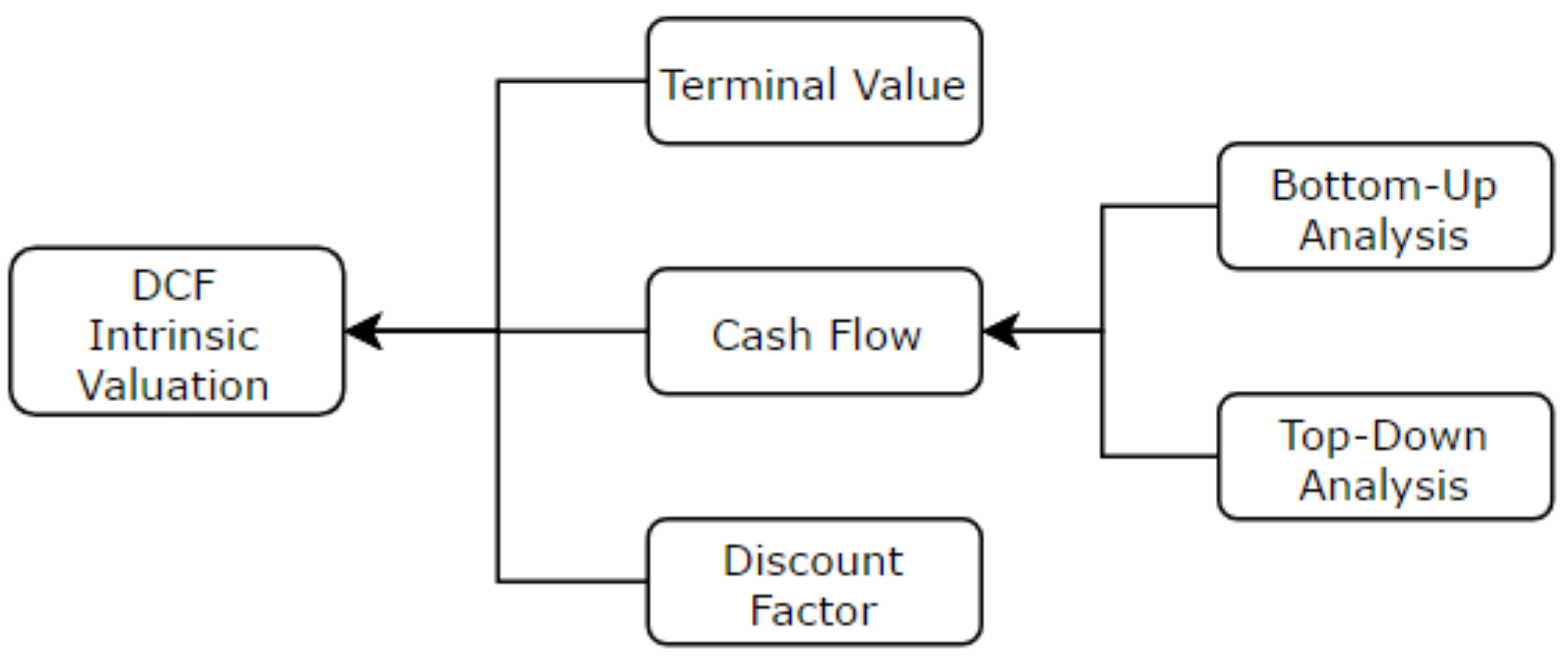

DCF components.

Source: author.

Discounted cash flow formula (with a perpetuity‑growth terminal value):

DCF = CF1 / (1 + r)1 + CF2 / (1 + r)2 + … + CFT / (1 + r)T + (CFT+1 / (r – g)) · 1 / (1 + r)T

Where CFt are cash flows in year t, r is the discount rate, and g is the long‑term growth rate.

Building a DCF

Start from operating cash flow (cash‑flow statement) and typically move to free cash flow (FCF) by subtracting capital expenditures. Example: if operating cash flow is €30m and capex is €5m, FCF = €25m. Project future FCF using growth assumptions (e.g., if 2020 FCF was €22.5m and 2021 FCF €25m, growth is ~11.1%). Use near‑term high‑growth and longer‑term fade assumptions to reflect maturation.

Determining the terminal value

The terminal value represents long‑term growth beyond the explicit forecast. A common formula is:

Terminal Value = CFT+1 / (r – g)

Ensure g is consistent with long‑run economic growth and the firm’s reinvestment needs.

Defining the discount rate

The discount rate reflects risk. Common choices include the risk‑free government yield, the opportunity cost of capital, and the WACC (weighted average cost of capital). In equity‑side models, CAPM is often used to estimate the cost of equity via beta (systematic risk).

Discounting the cash flows

Finally, discount projected cash flows and terminal value at the chosen rate to obtain present value. Sensitivity analysis (varying r, g, margins, capex) and scenario analysis (bull/base/bear) are essential to understand valuation drivers.

Example

You can download below an Excel file with an example of DCF. It deals with Maire Tecnimont, which is an Italian engineering and consulting company specializing in the fields of chemistry and petrochemicals, oil and gas, energy and civil engineering.

Why should I be interested in this post?

If you are an ESSEC student aiming for roles in investment banking, private equity, or equity research, mastering DCF is table‑stakes. This post distills how DCF fits among valuation approaches, the exact steps to build one, and the pitfalls you must stress‑test before using your number in IPOs, M&A, or buy‑side models.

Related posts on the SimTrade blog

▶ Jayati WALIA Capital Asset Pricing Model (CAPM)

▶ William LONGIN How to compute the present value of an asset?

▶ Maite CARNICERO MARTINEZ How to compute the net present value of an investment in Excel

▶ Andrea ALOSCARI Valuation methods

Useful resources

Damodaran online New York University (NYU).

European Central Bank (ECB) statistics

About the author

The article was written in November 2025 by Roberto RESTELLI (ESSEC Business School, Master in Finance (MiF), 2025–2026).