In this article, Mathias DUMONT (ESSEC Business School, Global Bachelor in Business Administration (GBBA), 2022-2026) explains how weather risk impacts the pricing of agricultural derivatives like futures and options, and how climate-based data can be integrated into stochastic pricing models. Combining academic insights and practical examples, including a mini-case from the SimTrade Blé de France simulation, the article illustrates adjustments to models such as the Black-Scholes-Merton model for temperature and rainfall variables in valuing agricultural contracts.

Introduction

Extreme weather has always been a critical factor in agriculture, but climate change is amplifying the frequency and severity of these events. From prolonged droughts to unseasonal floods, weather shocks can send crop yields and commodity prices on wild rides. This rising uncertainty has given birth to weather derivatives – financial instruments designed to hedge weather-related risks – and has made volatility forecasting a key challenge in pricing agricultural contracts. In fact, as businesses grapple with climate volatility, trading volume in weather derivatives has surged. CME Group saw a 260% increase last year (CME Group, 2023). The question for traders and risk managers is: how do we quantitatively factor weather risk into the pricing of futures and options on crops like wheat and corn?

Weather Risk and Agricultural Markets

Weather directly affects crop supply. A bumper harvest following ideal weather can flood the market and depress prices, whereas a drought or frost can decimate yields and trigger price spikes. These supply swings translate into volatility for agricultural commodity markets. For example, during the U.S. drought of 2012, corn prices skyrocketed, and the implied volatility of corn futures jumped by over 14 percentage points within a month, reaching ~49% in mid-July. Such surges reflect the market rapidly repricing risk as participants absorb new climate information (in this case, worsening crop prospects). Seasonal patterns are also evident: harvest seasons tend to coincide with higher price volatility because that’s when weather uncertainty is at its peak. Studies show that harvesting cycles create predictable seasonal volatility patterns in crop markets – when a critical growth period is underway, any shift in rainfall or temperature forecasts can send prices swinging.

Beyond affecting supply quantity, weather can influence crop quality (e.g., excessive rain can spoil grain quality) and even logistic costs (flooded transport routes, etc.), further feeding into prices. The interconnected global nature of agriculture means a drought in one region can reverberate worldwide. As noted in the SimTrade Blé de France case, weather conditions in France influence the quantity and quality of wheat the company harvests, while weather conditions around the world influence the international wheat price. In the Blé de France simulation (which models a French wheat producer’s stock), participants see how news of floods or droughts translate into stock price moves. For instance, the company might project a 7-million-ton wheat harvest, but analysts’ forecasts range from 6.5 to 7.2 Mt – with the realized level highly weather-dependent in the final weeks of the season. A poor weather turn not only shrinks the crop but boosts global wheat prices, creating a complex revenue impact on the firm. This mini-case underlines that weather risk entails both volume uncertainty and price uncertainty, a double-whammy for agricultural firms and their investors.

Case Study: Weather Shocks in Wheat Markets

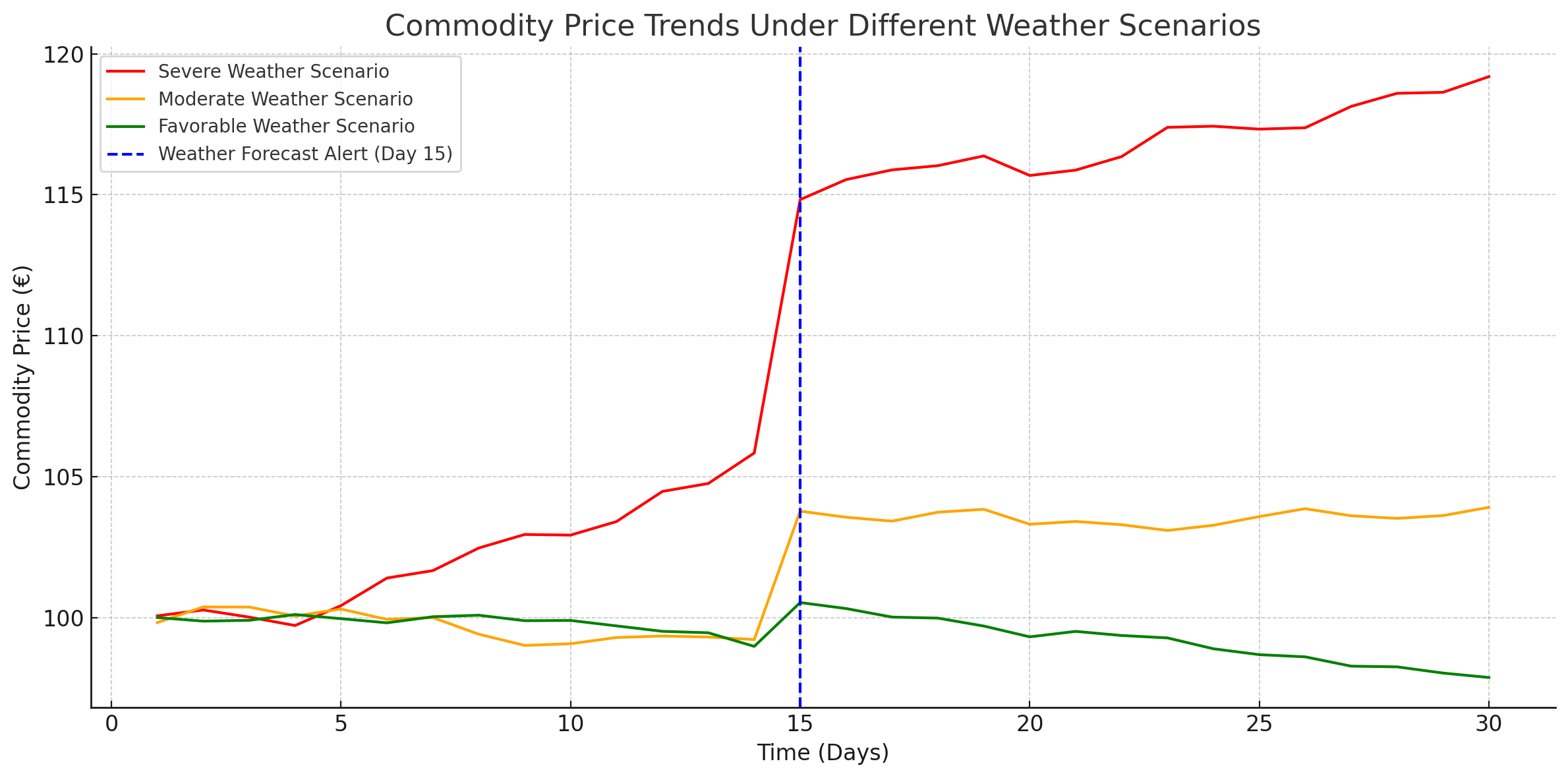

To illustrate the impact of weather risk on commodity pricing, consider three simulated scenarios for an upcoming wheat growing season: (1) **Favorable weather**, (2) **Moderate conditions**, and (3) **Severe weather** such as drought. Each scenario generates a distinct price trajectory in the wheat market. Under favorable weather, prices tend to remain stable or decline slightly, particularly at harvest, due to strong yields and potential oversupply. In moderate conditions, prices may rise modestly as the market adjusts to balanced supply and demand. In contrast, severe weather triggers early price rallies as concerns about yield shortfalls emerge, followed by sharp spikes once crop damage becomes evident. For producers and traders, anticipating these divergent price paths is essential for pricing contracts, managing risk exposure, and structuring hedging strategies effectively.

Figure 1. Simulated commodity price paths under three weather scenarios.

Source: Author’s simulation.

Figure 1. shows the simulation of commodity price paths under three weather scenarios: severe weather (red), moderate weather (orange), and favorable weather (green). A mid-season weather forecast alert (Day 15) triggers a shift in market expectations, causing price divergence. This simulation illustrates how weather shocks and forecasts impact commodity pricing through volatility and revised yield expectations.

From a risk management perspective, tools exist to handle these contingencies. Farmers or firms concerned about catastrophic weather can turn to weather derivatives for protection. Weather derivatives are financial contracts (often based on indexes like temperature or rainfall levels) that pay out based on specific weather outcomes, allowing businesses to offset losses caused by adverse conditions. They have been used by a wide range of players – from utilities hedging warm winters, to breweries hedging late frosts. These instruments can be customized over-the-counter or traded on exchanges. Notably, CME Group lists standardized weather futures and options tied to indices such as heating degree days (HDD) and cooling degree days (CDD) for various cities. The existence of such contracts means that even when commodity producers cannot fully insure their crop yield, they might hedge certain aspects of weather risk (like an unusually hot summer) via financial markets. In our context, a wheat farmer worried about drought could, say, buy a weather option that pays off if rainfall falls below a threshold, providing funds when their crop output (and thus futures position) suffers.

Climate-Based Volatility in Derivatives Pricing

How can weather uncertainty be incorporated into derivative pricing models? Classic option pricing, such as the Black-Scholes-Merton model, assumes a fixed volatility for the underlying asset’s returns. For agricultural commodities, that volatility is anything but constant – it ebbs and flows with the weather and seasonal progress. Practitioners thus often use stochastic volatility models or at least adjust the volatility input over time. For example, one might use higher volatility estimates during the crop’s growing season and lower volatility post-harvest when output is known. This practice parallels how equity traders anticipate higher volatility in stock prices ahead of major earnings or profit announcements, and lower volatility after the announcement of profits by the firm.

Like companies facing performance surprises, weather shocks inject information asymmetry into the market, which must be priced into the option premiums. This aligns with the observed Samuelson effect, where futures contracts on commodities tend to have higher volatility when they are near maturity (coinciding with harvest uncertainty).

Market prices of options themselves reflect these expectations. When a looming weather event is expected to cause turmoil, options premiums will rise. The metric capturing this is implied volatility – the volatility level implied by current option prices. Implied vol is essentially forward-looking and will jump if traders foresee choppy waters ahead. Empirical evidence shows that extreme weather forecasts translate into higher implied vols for crop options. In 2012, as drought fears intensified, corn option implied volatility spiked (alongside futures prices). Conversely, once a forecasted drought started being relieved by rains, implied volatility eased off, signaling that some uncertainty had been resolved. A recent study also found that integrating meteorological data (like rainfall and temperature anomalies) into volatility modeling significantly improves the ability to hedge risk in agricultural markets. In other words, the more information we feed into our models about the climate, the more accurately we can price and hedge these derivatives.

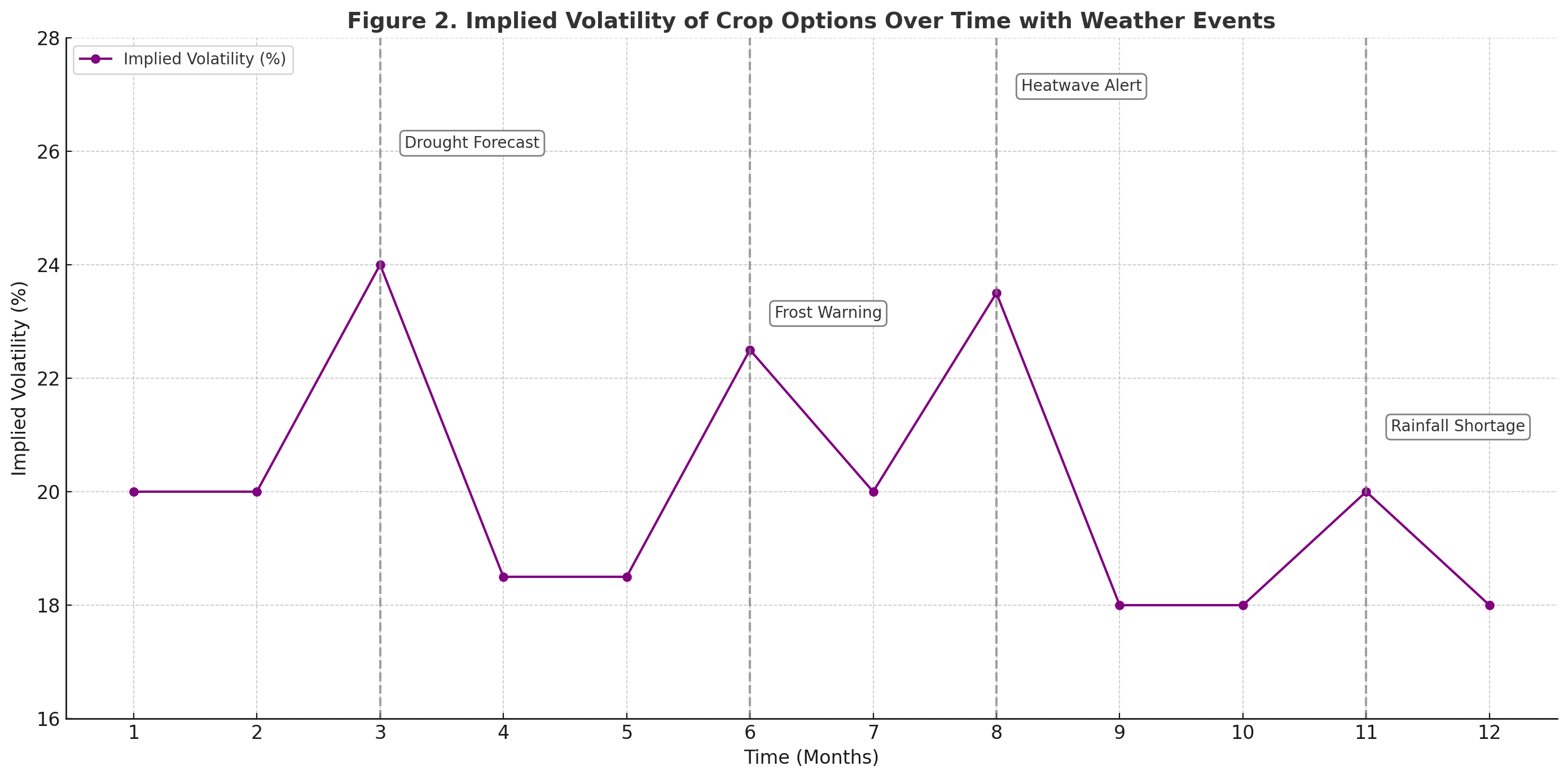

Figure 2. Implied Volatility of Crop Options Over Time with Weather Events

Source: Author’s simulation.

This simulation illustrates the evolution of implied volatility over a 12-month crop cycle. Forecasted climate events—drought (Month 3), frost (Month 6), heatwave (Month 8), and rainfall shortage (Month 11)—lead to moderate but distinct volatility spikes. As uncertainty resolves, volatility returns to baseline.

One practical approach to pricing under climate uncertainty is to use scenario-based or simulation-based models. Instead of assuming a single volatility number, an analyst can simulate thousands of possible weather outcomes (perhaps using historical climate data or meteorological forecast models) and the corresponding price paths for the commodity. Each simulated price path yields a payoff for the derivative (e.g. an option’s payoff at expiration), and by averaging those payoffs (and discounting appropriately), one can derive a weather-adjusted theoretical price. This Monte Carlo style approach effectively treats weather as an external random factor influencing the commodity’s drift and volatility. It’s particularly useful for complex derivatives or when the payoff depends explicitly on weather indices (such as a derivative that pays out if rainfall is below X mm).

When the derivative’s underlying is the commodity itself (e.g. a corn futures option), traditional risk-neutral pricing arguments still apply, but the challenge is forecasting volatility. Traders often adjust the volatility smile/skew on agricultural options to account for asymmetric weather risks – for instance, if a drought can cause a much bigger upside move than a rainy season can cause a downside move, call options might embed a higher implied volatility (reflecting that upside risk of price spikes). This is observed in practice as well; extreme weather events can distort the implied volatility “skew” of crop options, as out-of-the-money calls become more sought after as disaster insurance.

In contrast, if the derivative’s underlying is a pure weather index (say an option on cumulative rainfall), then pricing becomes more complex because the underlying (rainfall) is not a tradable asset. In such cases, the Black-Scholes-Merton formula is not directly applicable. Instead, pricing relies on actuarial or risk-neutral methodologies that incorporate a market price of risk for weather. For example, one method is to estimate the probability distribution of the weather index from historical data, then add a risk premium to account for investors’ risk aversion to weather variability, and discount expected payoffs accordingly. Another method uses “burn analysis” – taking historical weather outcomes and the associated financial losses/gains had the derivative been in place, to gauge a fair premium. Academic research has proposed models ranging from modified Black-Scholes-Merton-type formulas for rainfall (with adjustments for the non-tradability) to advanced statistical models (e.g. Ornstein-Uhlenbeck processes with seasonality for temperature indices. The key takeaway is that whether it’s directly in commodity options or in dedicated weather derivatives, climate factors force us to go beyond textbook models and embrace more dynamic, data-driven pricing techniques.

Why should I be interested in this post?

For an ESSEC student or a young finance professional, this topic sits at the intersection of finance and real-world impact. Understanding weather risk in markets is not just about farming – it’s about how big data and climate science are increasingly intertwined with financial strategy. Agricultural commodities remain a cornerstone of the global economy, and volatility in these markets can affect food prices, inflation, and even economic stability in various countries. By grasping how to value derivatives with climate-based volatility inputs, you are gaining insight into a growing niche of finance that deals with sustainability and risk management. Moreover, the skills involved – scenario analysis, simulation modeling, blending of economic and scientific data – are highly transferable to other domains (think energy markets or any sector where uncertainty reigns). In a world facing climate change, expertise in weather-related financial products could open career opportunities in commodity trading desks, insurance/reinsurance firms, or specialized hedge funds. Ultimately, this post encourages you to think creatively and interdisciplinarily: the best hedging or valuation solutions may come from combining financial theory with environmental intelligence.

Related posts on the SimTrade blog

▶ Camille KELLER Coffee Futures: The Economic and Environmental Drivers Behind Rising Prices

▶ Jayati WALIA Implied Volatility

▶ Akshit GUPTA Futures Contract

▶ Anant JAIN Understanding Price Elasticity of Demand

Useful resources

Chicago Mercantile Exchange (CME) Weather futures and options product information. (Exchange-traded weather derivative contracts on temperature and other indices)

U.S. Energy Information Administration Drought increases price of corn, reduces profits to ethanol producers (2012). (Article discussing the 2012 drought’s impact on corn prices and volatility)

Nature Communications (2024) Financial markets value skillful forecasts of seasonal climate. (Research showing that seasonal climate outlooks have measurable effects on implied volatility and market uncertainty)

Das, S. et al. (2025) Predicting and Mitigating Agricultural Price Volatility Using Climate Scenarios and Risk Models. (Academic study demonstrating the integration of climate data into volatility models and using Black-Scholes to value a government price support as a put option)

Pai, J. & Zheng, Z. (2013) Pricing Temperature Derivatives with a Filtered Historical Simulation Approach. (Discussion of why Black-Scholes is not directly applicable to weather derivatives and alternative pricing approaches)

About the author

The article was written in May 2025 by Mathias DUMONT (ESSEC Business School, Global Bachelor in Business Administration (GBBA), 2022-2026).