In this article, Nithisha CHALLA (ESSEC Business School, Grande Ecole Program – Master in Management (MiM), 2021-2024) delves into Dividends, providing a comprehensive analysis on type of dividends, explaining its theoretical foundations, discussing the policy strategies, its valuation and limitations.

Introduction

Dividends are a fundamental component of shareholder returns, representing a direct distribution of a company’s profits to its investors. They play a crucial role in corporate finance, investment decision-making, and equity valuation. Dividends not only signal financial health but also serve as a means of returning excess capital to shareholders. For finance students, understanding the theoretical foundations, types, determinants, and impact of dividends is essential for analyzing investment opportunities and corporate strategies.

Definition and Types of Dividends

A dividend is a payment made by a corporation to its shareholders, typically derived from net profits. Companies distribute dividends as a reward to shareholders for their investment, either in cash or additional shares.

There are different types of dividends:

- Cash Dividends – The most common form, where companies pay shareholders a fixed amount per share.

- Stock Dividends – Companies issue additional shares instead of cash, increasing the number of outstanding shares while retaining cash reserves.

- Property Dividends – Non-cash distributions, such as physical assets or securities of a subsidiary.

- Scrip Dividends – A promissory note issued by a company, committing to pay dividends at a later date.

- Liquidating Dividends – Distributed when a company is winding up operations, returning capital to investors beyond retained earnings.

Theoretical Foundations of Dividends

Dividends have been widely analyzed in financial theory, particularly in relation to firm value, investor behavior, and market efficiency.

Dividend Irrelevance Theory (Miller & Modigliani, 1961)

Miller and Modigliani argue that in a perfect capital market, dividend policy is irrelevant to a company’s valuation. The theory rests on several idealized assumptions. Miller and Modigliani asserted that in a perfect capital market (no taxes, transaction costs, or information asymmetry), a company’s dividend policy does not affect its market value or cost of capital. According to this theory, investors are indifferent between dividends and capital gains because they can generate “homemade dividends” by selling a portion of their shares if they desire cash.

Bird-in-the-Hand Theory

This theory suggests that investors prefer dividends over capital gains because they perceive dividends as more certain, reducing risk. It argues that firms with higher dividend payouts are more attractive to risk-averse investors.

Tax Preference Theory

Investors may prefer capital gains over dividends due to favorable tax treatment. In many jurisdictions, capital gains are taxed at a lower rate or deferred until realized, whereas dividends are often taxed immediately.

Signaling Theory (Bhattacharya, 1979)

Dividends serve as a signal of financial health. Since poorly performing firms cannot afford sustained dividend payments, an increase in dividends suggests management confidence in future earnings. Conversely, a dividend cut can signal financial distress.

Agency Theory and Free Cash Flow Hypothesis (Jensen, 1986)

Dividends can mitigate agency problems by reducing the free cash flow available to managers, thus limiting their ability to engage in inefficient spending or empire-building. Regular dividend payments force companies to be disciplined in capital allocation.

Determinants of Dividend Policy

Several factors influence a firm’s dividend decisions:

- Profitability – Firms with stable and growing profits are more likely to pay consistent dividends.

- Growth Opportunities – High-growth firms often reinvest earnings into expansion, leading to lower or no dividends.

- Liquidity Position – Even profitable firms may avoid dividends if they face cash flow constraints.

- Debt Levels – Highly leveraged firms prioritize debt repayments over dividend distributions.

- Taxation Policies – Tax treatment of dividends vs. capital gains affects investor preference and corporate policies.

- Market Expectations – Investors expect stable or gradually increasing dividends; sudden reductions can lead to stock price declines.

- Macroeconomic Conditions – Economic downturns, inflation, and interest rate changes impact corporate profitability and dividend policies.

Dividend Policy Strategies

In practice, companies adopt different dividend policies based on their financial strategy and market positioning:

- Stable Dividend Policy – Fixed payouts irrespective of earnings fluctuations (e.g., Coca-Cola).

- Constant Payout Ratio – A fixed percentage of earnings is paid as dividends.

- Residual Dividend Policy – Dividends are paid after funding all capital investment opportunities.

- Hybrid Dividend Policy – A mix of stable dividends and periodic special dividends.

Dividends and Valuation

Dividends are critical in valuation models, as they represent cash flows to shareholders.

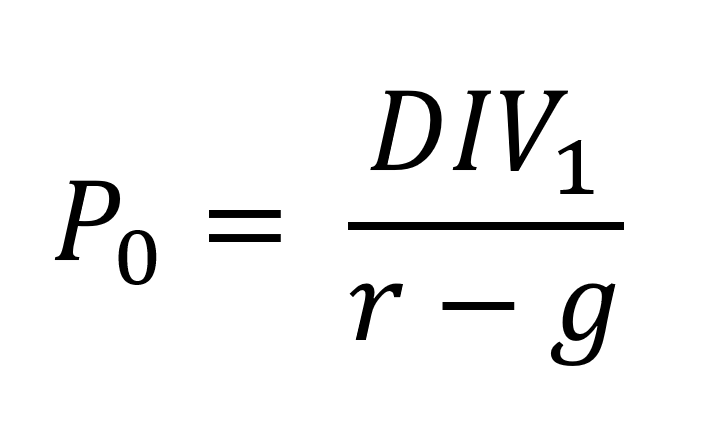

Dividend Discount Model (DDM)

The Gordon Growth Model is a fundamental valuation tool:

Formula of Dividend Discount Model (DDM)

where:

- P0 = Current stock price

- DIV1 = Expected next-year dividend

- r = Required rate of return

- g = Dividend growth rate

This model applies to firms with stable dividend growth but is less effective for high-growth or non-dividend-paying companies.

Discounted Cash Flow (DCF) Model

DCF considers total cash flows, incorporating dividends as part of Free Cash Flow to Equity (FCFE). It provides a broader valuation approach beyond just dividends.

Comparative Valuation

Dividend yield (DP\frac{D}{P}PD) is commonly used to compare income-generating stocks. A higher yield may indicate undervaluation but could also signal financial distress.

Empirical Evidence and Case Studies

- Apple: Initially avoided dividends but introduced payouts in 2012 after accumulating substantial cash reserves, balancing growth and shareholder returns.

- General Electric (GE): A significant dividend cut in 2018 led to a major stock price decline, showing the impact of investor expectations.

Limitations of Dividend Analysis

- Does Not Reflect Total Returns – Dividends exclude capital gains, potentially underestimating true investor returns.

- Influence of External Factors – Regulatory policies, tax changes, and economic conditions impact dividend sustainability.

- Not Suitable for Growth Stocks – Many high-growth firms reinvest profits, making dividend-based valuation ineffective.

- Potential for Financial Misinterpretation – High dividends may indicate strong profitability or a lack of profitable reinvestment opportunities.

Conclusion

Dividends remain a crucial aspect of financial analysis, providing insights into corporate strategy, investor expectations, and firm valuation. While theories like M&M’s irrelevance hypothesis argue that dividends do not affect firm value, real-world evidence suggests that dividends play a significant role in investor preferences and market perception. Understanding dividend policies and valuation models equips finance students with the necessary analytical skills to evaluate investment opportunities and corporate strategies effectively.

Why should I be interested in this post?

For master’s students in finance, understanding dividends is essential for making informed investment decisions, evaluating corporate financial strategies, and mastering valuation techniques. Dividends are a key component of Total Shareholder Return (TSR) and play a crucial role in equity pricing models like the Dividend Discount Model (DDM) and Discounted Cash Flow (DCF) analysis. By studying dividends, students gain insights into capital allocation, corporate governance, and investor behavior—fundamental areas in asset management, investment banking, and financial advisory.

Related posts on the SimTrade blog

Modelling

▶ Isaac ALLIALI Understanding the Gordon-Shapiro Dividend Discount Model: A Key Tool in Valuation

▶ Lou PERRONE Free Cash Flow: A Critical Metric in Finance

▶ Isaac ALLIALI Decoding Business Performance: The Top Line, The Line, and The Bottom Line

Data for dividends

▶ Nithisha CHALLA Compustat

▶ Nithisha CHALLA CRSP (Center for Research in Security Prices)

▶ Nithisha CHALLA Bloomberg

Useful resources

Academic articles

Bhattacharya, S. (1979) Imperfect Information, Dividend Policy, and “The Bird in the Hand” Fallacy. The Bell Journal of Economics, 10(1), 259–270.

Jensen, M. C. (1986) Agency Costs of Free Cash Flow, Corporate Finance, and Takeovers. American Economic Review, 76(2), 323–329.

Miller, M. H., & Modigliani, F. (1961) Dividend Policy, Growth, and the Valuation of Shares. The Journal of Business, 34(4), 411–433.

Business

Dividend University Dividend Irrelevance Theory

Harvard Business School Publications The Effect of Dividends on Consumption

Other resources

Religare Broking What are Different Types of Dividends?

Munich Business School Dividend explained simply

CNBC What are dividends and how do they work?

About the author

The article was written in May 2025 by Nithisha CHALLA (ESSEC Business School, Grande Ecole Program – Master in Management (MiM), 2021-2024).